Market Overview

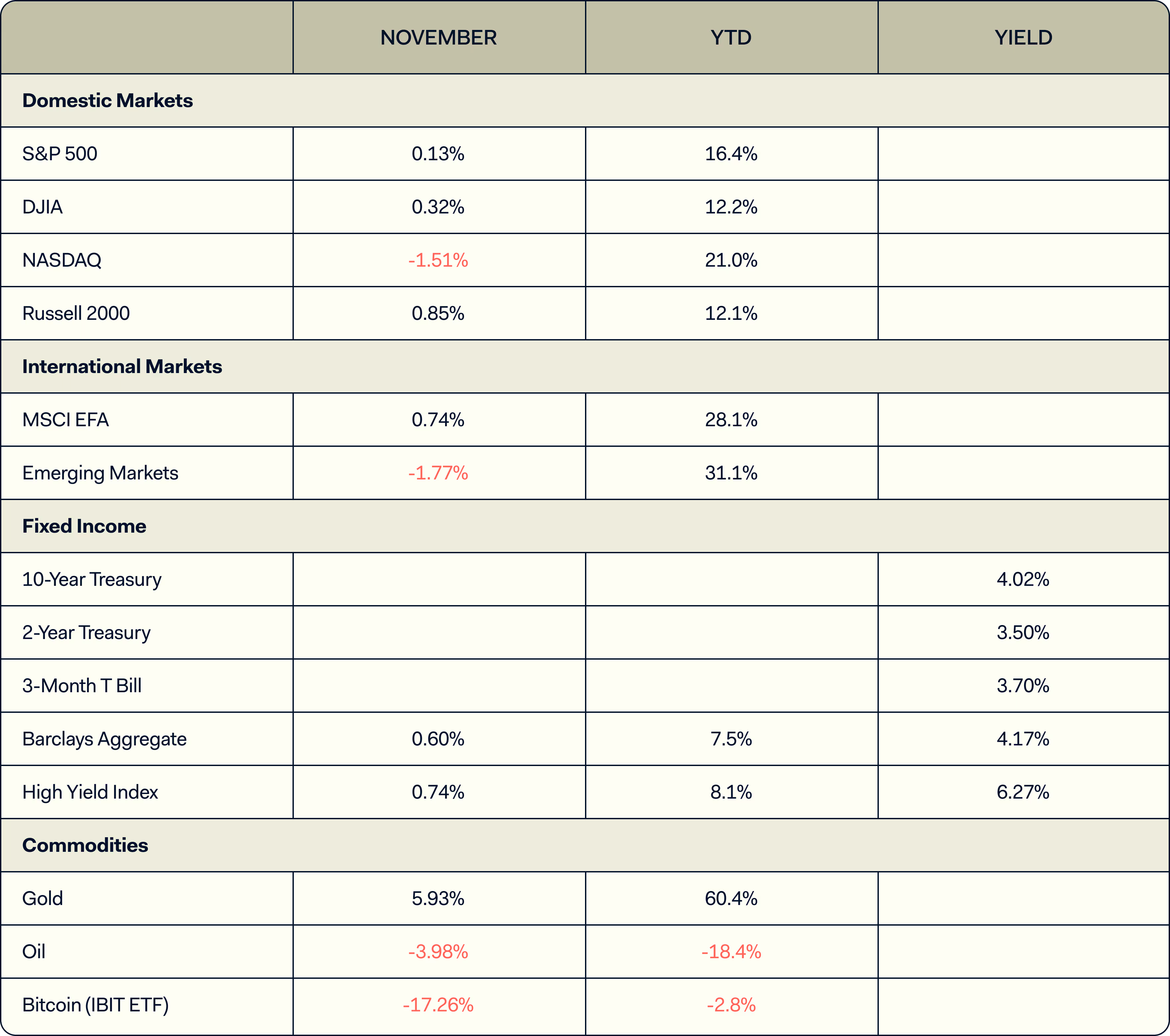

The S&P 500 ended November at 6,849.09, posting a fractional 0.01% gain for the month. While essentially flat, the path to that result was anything but uneventful. Concerns over AI infrastructure financing, crowded positioning, overly optimistic sentiment, and a sharp reassessment of the odds of a December rate cut triggered intense selling pressure mid-month. By November 20th, the S&P had fallen 4.4%, marking its monthly closing low.

Over the following four and a half sessions, equities staged a robust 4.75% rebound, bringing the index back to unchanged. November became the seventh consecutive monthly gain, albeit the smallest of the year. The NASDAQ finished -1.5% for the month, reflecting a rotation out of large-cap technology stocks.

Farther Market Perspective

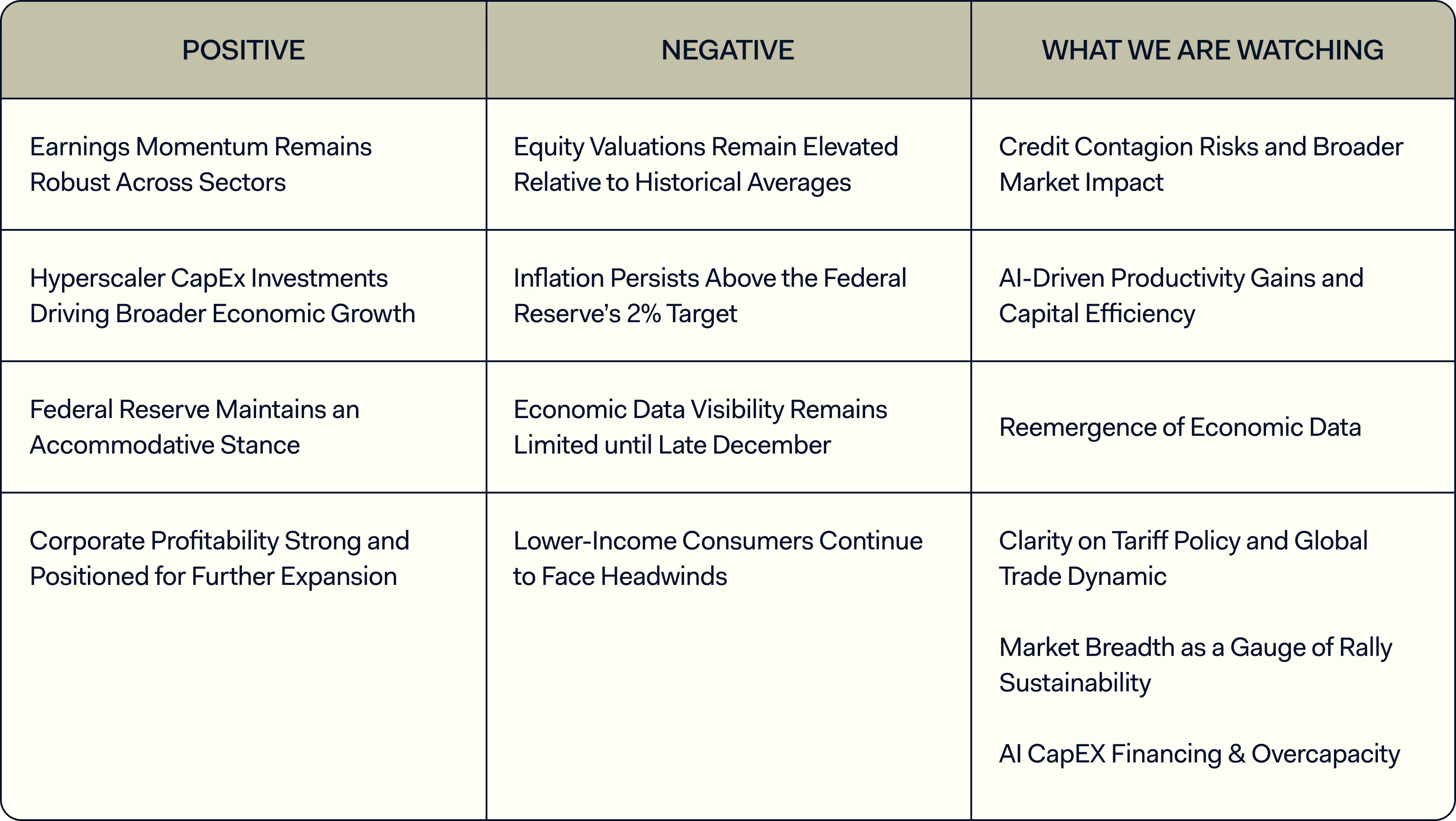

The following is a summary of positives, negatives, and what we are watching in the market.

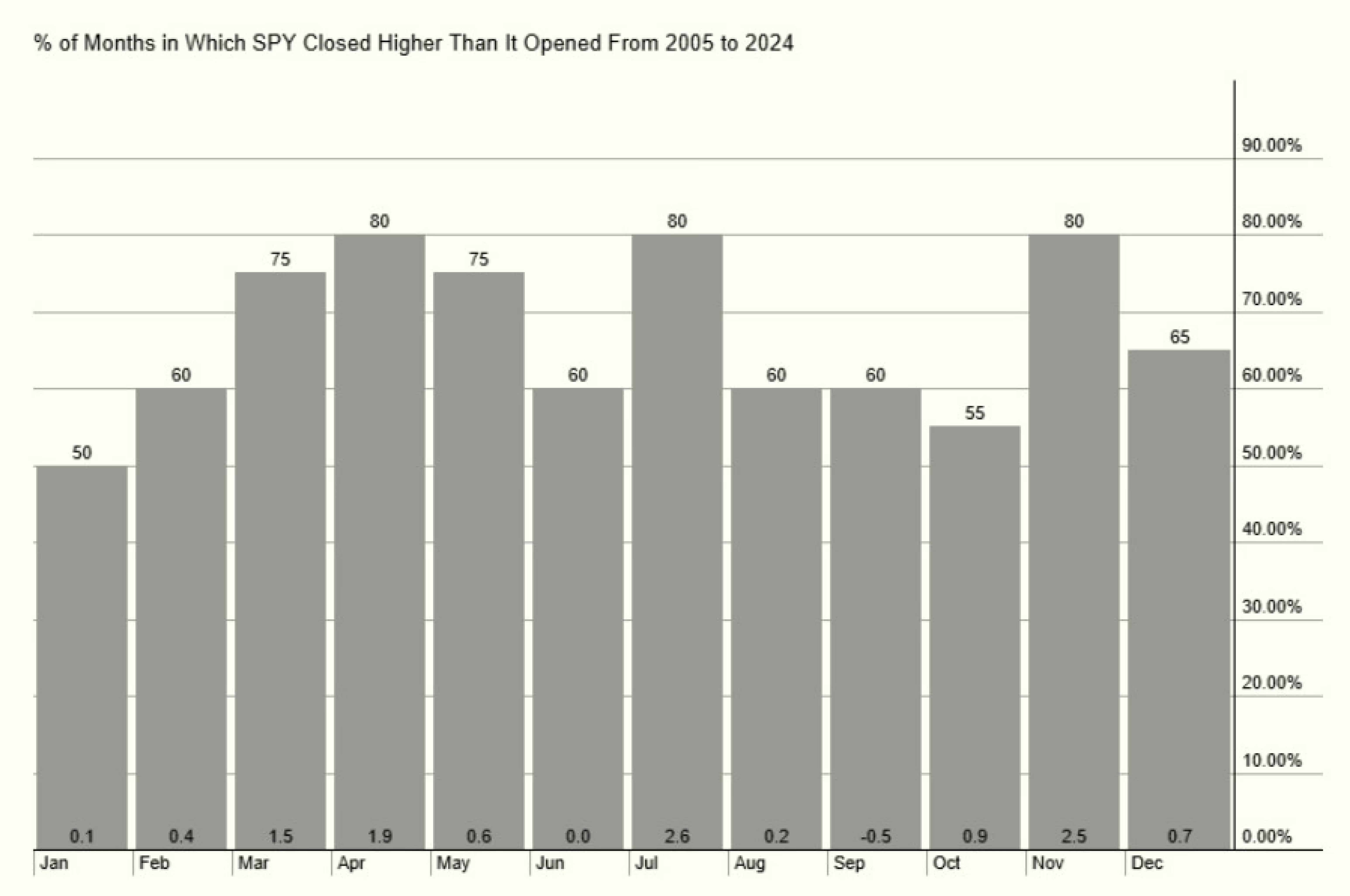

The December Dilemma: Will Seasonal Strength Win the Battle Against Macro Headwinds?

Historically, December has been a favorable month for equities, posting positive returns 65% of the time.1 However, several unresolved macro and thematic overhangs could limit near-term visibility:

- Slowing job growth

- Rising concerns about economic contraction

- Uncertain returns on AI investment

- Massive future AI capital expenditures (CapEx) financing needs

These issues are unlikely to be resolved before year-end—and will likely continue to influence markets into 2026.

Sector Highlight: Healthcare Delivers a Standout Gain

Following significant underperformance, the Healthcare sector delivered standout performance in November, demonstrating the market rotation underway as investors became increasingly concerned about tech valuations. XLV (Healthcare Sector ETF) returned +9.3% for the month of November. Select large-cap pharmaceutical companies continued to outpace the broader market for the year as a whole. Some of those standouts include:

- JNJ +42% YTD

- LLY +37% YTD

- ABBV +27% YTD

These gains far exceeded the S&P 500’s +16% YTD gain thus far.

The performance of the Healthcare sector illustrates the benefits of owning a well-diversified portfolio.

Bitcoin’s Warning: A Correction Signals Crypto Turmoil

Bitcoin again functioned as a high-beta market signal. After peaking at $123,355 on October 9, it corrected 31.4% to $84,648 before rebounding modestly to the low $90,000s alongside equities. As of December 3rd, Bitcoin is averaging daily moves of 4%.

The Sudden Spike: November’s Brief Moment of Volatility

The VIX, which tracks the expected volatility of the S&P 500, began November at 17.44, surged to 26.42 (+51.5%), then retreated to finish at 16.35, below its starting point. This surge underscores the month’s significant—but ultimately short-lived—risk-off episode.

Limited Visibility Heading into the December Fed Meeting

The final Federal Reserve meeting is approaching on December 10. Since the last Fed meeting, the probability of a December rate cut has fluctuated dramatically, as illustrated by the following events and their corresponding probability of a rate cut occurring:3

- 100% probability before the October Fed Meeting

- Declined to 60% after Powell’s press conference

- Further moved down to 30% at the mid-November equity lows

- Moved up to 70% by month-end due to dovish Fed commentary

- Virtually back to 100% following the weak ADP Payroll Report (-32,000)4 on December 3rd

Complicating Fed interest rate policy decisions is a lack of critical economic data following the government shutdown that ended on November 12:

- The October payrolls report and October CPI will not be published.

- The December jobs report (Dec 16) andthe inflation report (Dec 18) follow the December 9–10 FOMC meeting.

As a result, the Federal Reserve will be “flying blind” without key economic inputs to guide its decision-making during one of the year’s most pivotal meetings.

The Trillion-Dollar Question: Can OpenAI Finance the AI Arms Race?

A central market concern remains how the AI infrastructure buildout will be financed.

OpenAI, now generating roughly $20B in annual revenue, has outlined an extraordinary $1.4 trillion decade-long capital expenditure plan to secure 26 GW of compute capacity—a figure 3x its current $500B valuation and 70x its revenue run rate.5

To support this, the company is exploring:

- Government partnerships

- Retail/e-commerce tools

- Short-form video initiatives

- Selling computing capacity via Stargate

Whether these efforts ultimately close the financing gap is unclear.

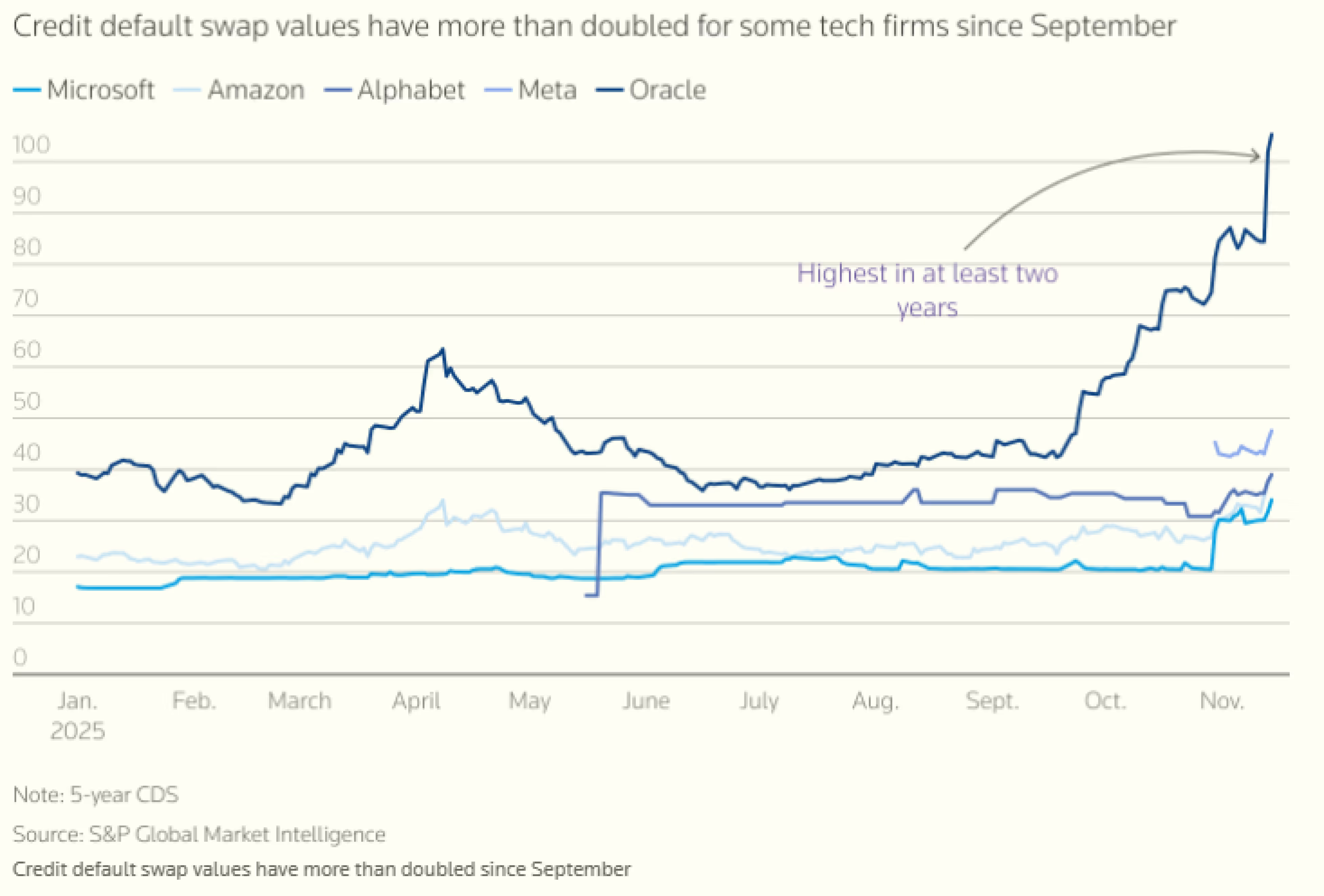

Credit Default Swaps and Tech Debt Issuance

An unusual development has been the widening of Credit Default Spreads (CDS) on major tech companies—traditionally among the safest credits due to high margins and strong balance sheets. This change reflects increased investor concerns about debt-financed AI investment.6

Notable tech debt issuances:

- META issued $30B in debt (Oct 2025)

- ORCL issued $18B (Sept 2025), with the stock now 42% below its 52-week high

The Mag-7 trade is also losing momentum. Relative to the S&P’s +16% YTD, several names now lag:

- Laggards: MSFT (+15%), AAPL (+13%), META (+9%), AMZN (+7%), TSLA (+6%)

- Leaders: GOOG (+65%), NVDA (+34%)

NVDA Earnings: Stellar Results Met with a Sharp Reversal

As always, NVDA earnings sit alongside birthdays and anniversaries on the “do not forget” list for financial professionals. NVDA semiconductor chips represent the bellwether for AI infrastructure spending.7

On November 19, NVDA delivered another strong beat:

- Revenue: $57B vs. $55B expected

- EPS: $1.30 vs. $1.25 expected

- Guidance:

- Revenue: $65B vs. $61.8B expected

- Gross margin: 75% vs. 74.5% expected

Despite positive earnings and guidance, the stock’s reaction was striking:

- Opened +5% to ~$196

- Reversed sharply

- Closed –3.2% on the day

The reversal in price action raises the question: Are we nearing peak AI optimism?

NVDA valuation remains reasonable at 25× 2026 EPS, not far from the S&P’s 22×. But the market is beginning to debate when NVDA’s earnings will peak—a storyline unlikely to be resolved until well into 2026.

Cracks in the Private Credit Armor

To follow up on our previous month’s commentary on private credit, we saw continued signs of strain in November.

Blue Owl, a $150 billion private credit provider, terminated the merger of its non-traded BOC II vehicle into the publicly traded Blue Owl Capital Corp, citing market conditions. Investor losses could have approached 20% based on prevailing marks, while investors would have been restricted from selling shares until deal closure. The parent company’s stock fell 13% during the month.

Loan Pricing Discrepancies

Medallia (software company) loan marks varied widely:8

- Apollo: 77 cents

- Blackstone: 82 cents

- KKR: 91 cents

Such discrepancies highlight the opacity and subjectivity inherent in private credit valuation. We are monitoring this area closely as we continue to meet with private credit managers.

Goodbye, QT

December 1 marked the official end of Quantitative Tightening (QT). The Fed will no longer shrink its balance sheet and will now reinvest all principal from maturing Treasury and MBS holdings. This will stabilize the balance sheet and halt liquidity withdrawals. The Fed’s actions represent a meaningful shift in the macro liquidity backdrop.

As we enter December, the Farther Investment Team is actively preparing our 2026 Outlook, which will be available in January.

Until then, we wish you and your families a happy, healthy, and restful holiday season.

Farther Market Summary

All Performance Data is sourced from Bloomberg

All Performance Data included Dividends

___

References

(All performance and Price Data is sourced from Bloomberg)

- Trade That Swing, November 30, 2025

- Stockchart.com, November 30, 2025

- https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- ADP Employment Report December 3, 2025

- CNBC, November 6, 2025

- Reuters, November 18, 2025

- Bloomberg/NVDA, November 19, 2025

- PrivateDebtNews.org November 15, 2025