Market Overview

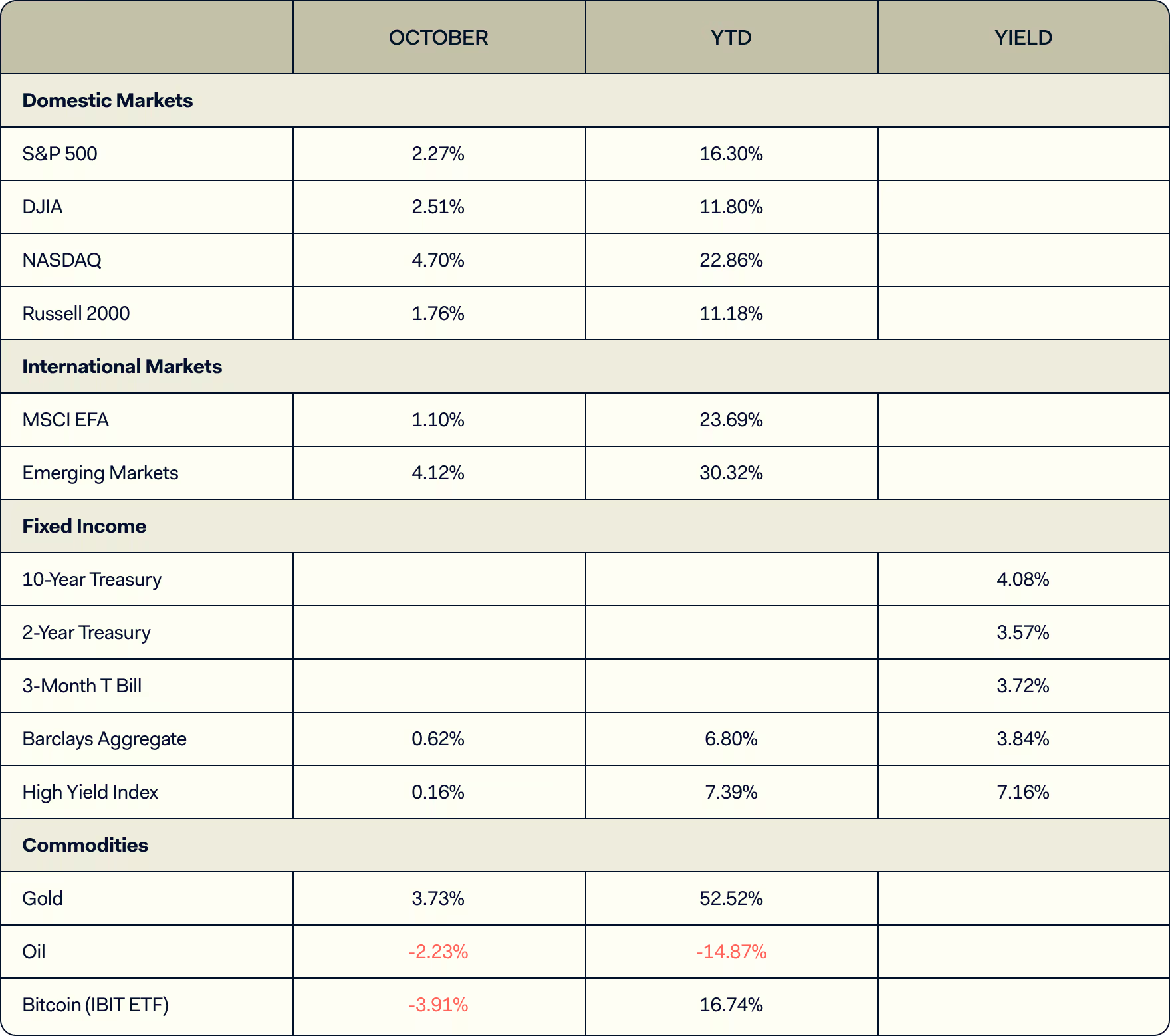

The S&P 500 posted its sixth consecutive monthly gain in October, while the Nasdaq extended its winning streak to seven months—its longest since 2018. Strong corporate earnings, increased conviction in the AI narrative, and the resolution of U.S.–China trade tensions drove equity markets higher.

The month began on a volatile note: on October 10th, the S&P 500 declined 2.7% and the Nasdaq fell 3.6% following renewed trade war rhetoric and tariff threats. However, markets rebounded later in the month as the U.S. agreed to reduce tariffs on Chinese imports by 10% in exchange for China suspending rare earth export controls, resuming soybean purchases, and implementing measures to curb fentanyl precursor exports.

Farther Market Perspective

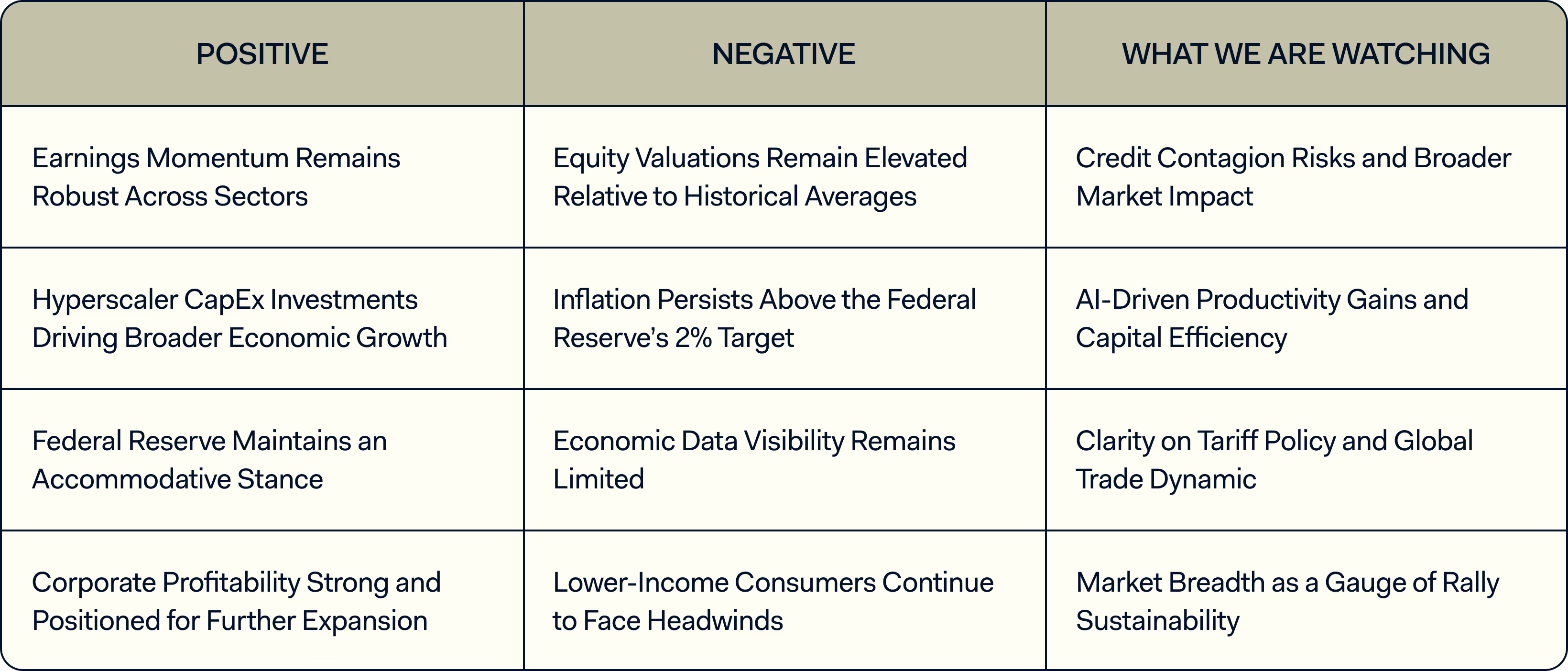

The following is a summary of positives, negatives and what we are watching in the market.

________________

Credit Market Concerns: First Brands & Tricolor

Investor sentiment early in October was also shaken by the September bankruptcies of First Brands, an auto parts supplier, and Tricolor, a subprime auto finance dealer network. JP Morgan CEO Jamie Dimon warned of potential systemic credit risks, noting that “when you find one cockroach, there are probably more,” following JPM’s $170 million write-off tied to Tricolor.1

These events have reignited debate around the health of private credit markets, concerns over lending standards, and the potential for widening credit spreads.

As part of our ongoing due diligence, we met with multiple private credit managers to assess potential exposure. Encouragingly, none of our managers reported direct involvement, citing strong internal underwriting processes that avoided both names.

- First Brands appears to have engaged in fraudulent practices involving double-pledged collateral and off-balance-sheet loans.

- Tricolor suffered from similar “double-pledging” of receivables, compounded by rising delinquencies among its low-income and undocumented borrower base.

While these bankruptcies appear isolated for now, we are monitoring for additional stress in the credit system. The private credit industry remains relatively young and has yet to experience a major downcycle. We continue to emphasize fraud detection, underwriting rigor, and transparency as key selection criteria when partnering with private credit managers.

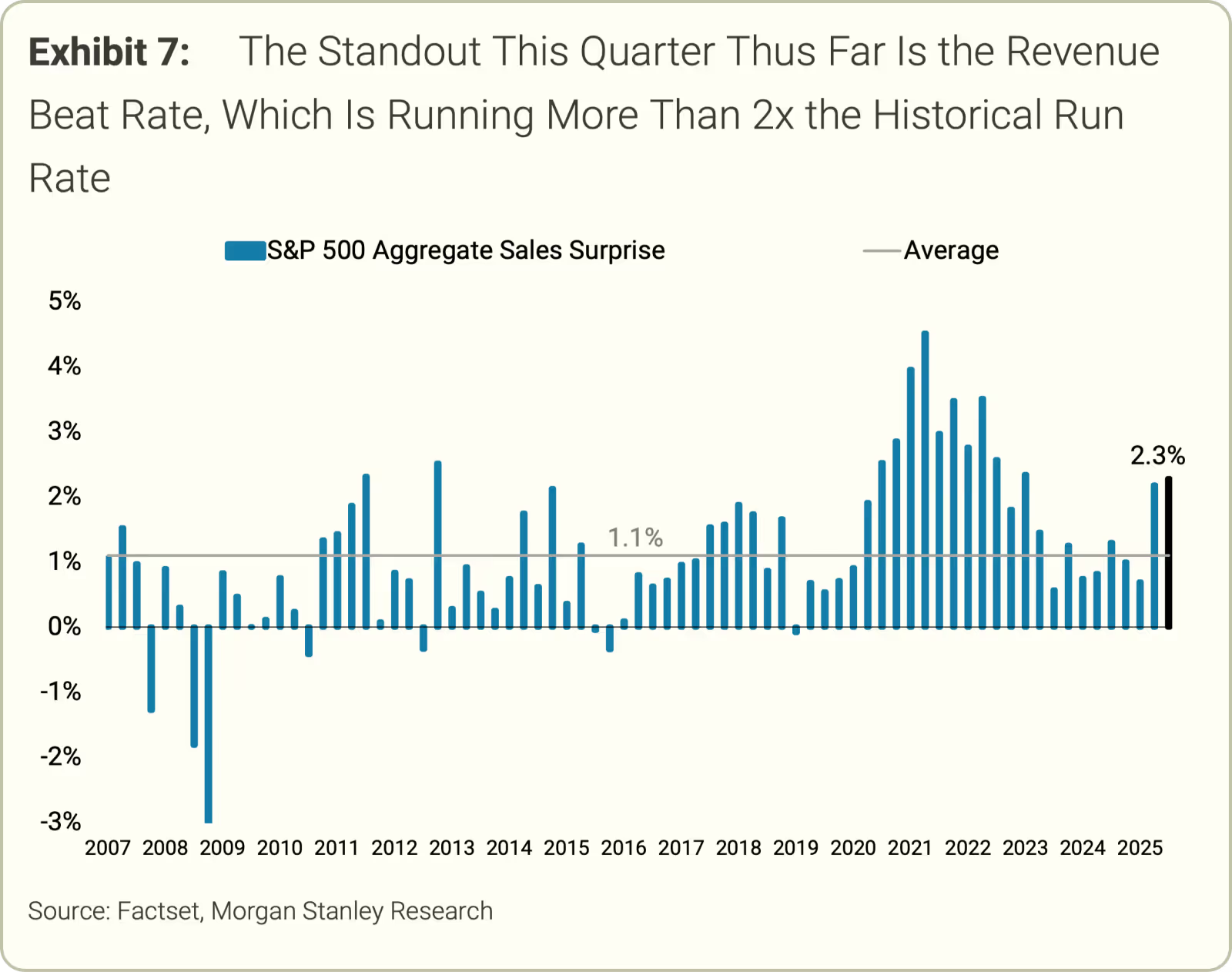

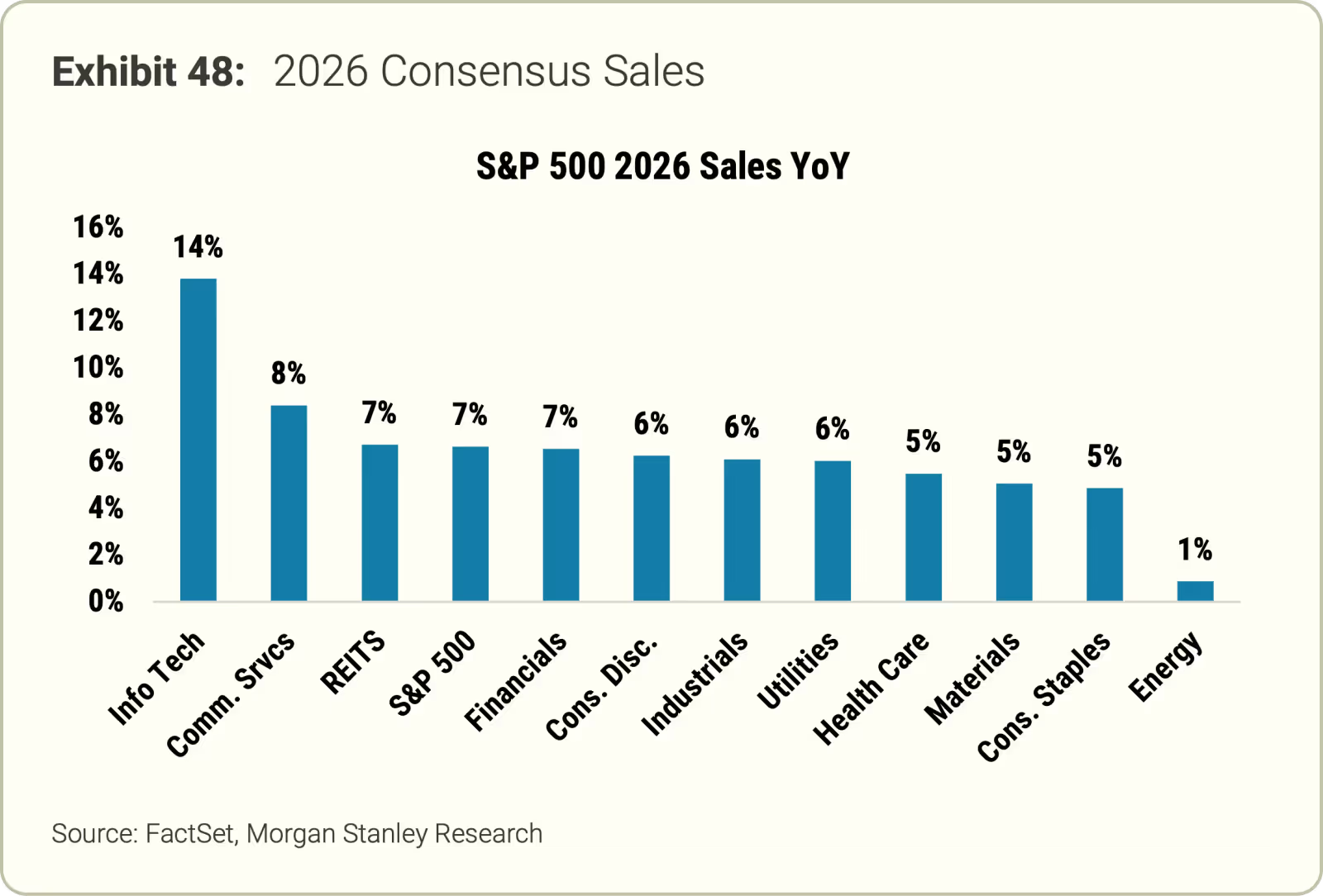

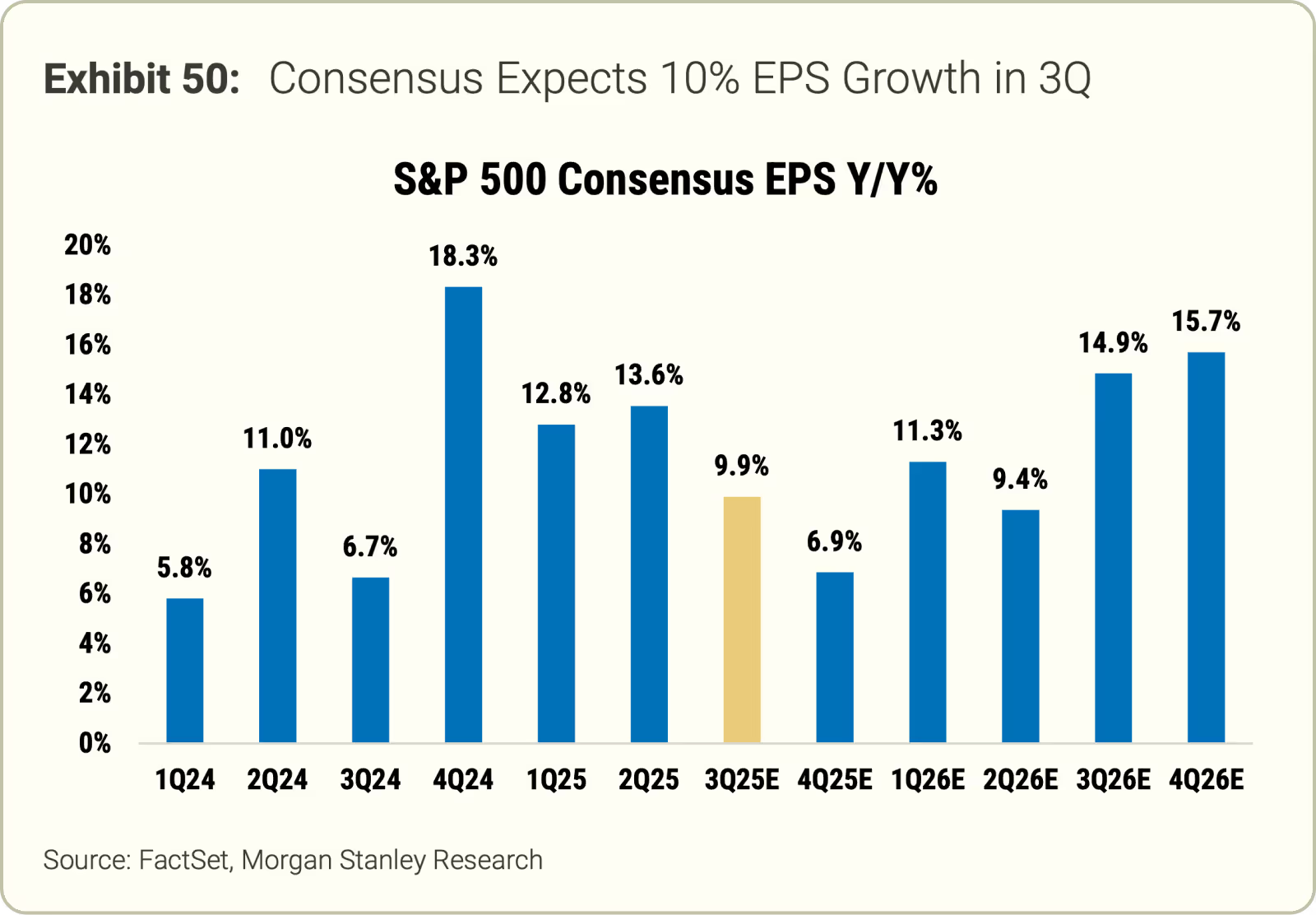

Q3 2025 Earnings Season

Through the end of October, roughly 68% of S&P 500 companies had reported third-quarter results. Overall, the earnings season has been robust:

- Revenue surprise: +2.2% (vs. 1.3% historical average)

- EPS surprise: +4.5% (vs. 4.4% historical average)

- Consensus EPS growth: +10% for 2025, +14% for 2026

- Consensus sales growth: +6% (Q3’25), +4% (2025), +7% (2026)

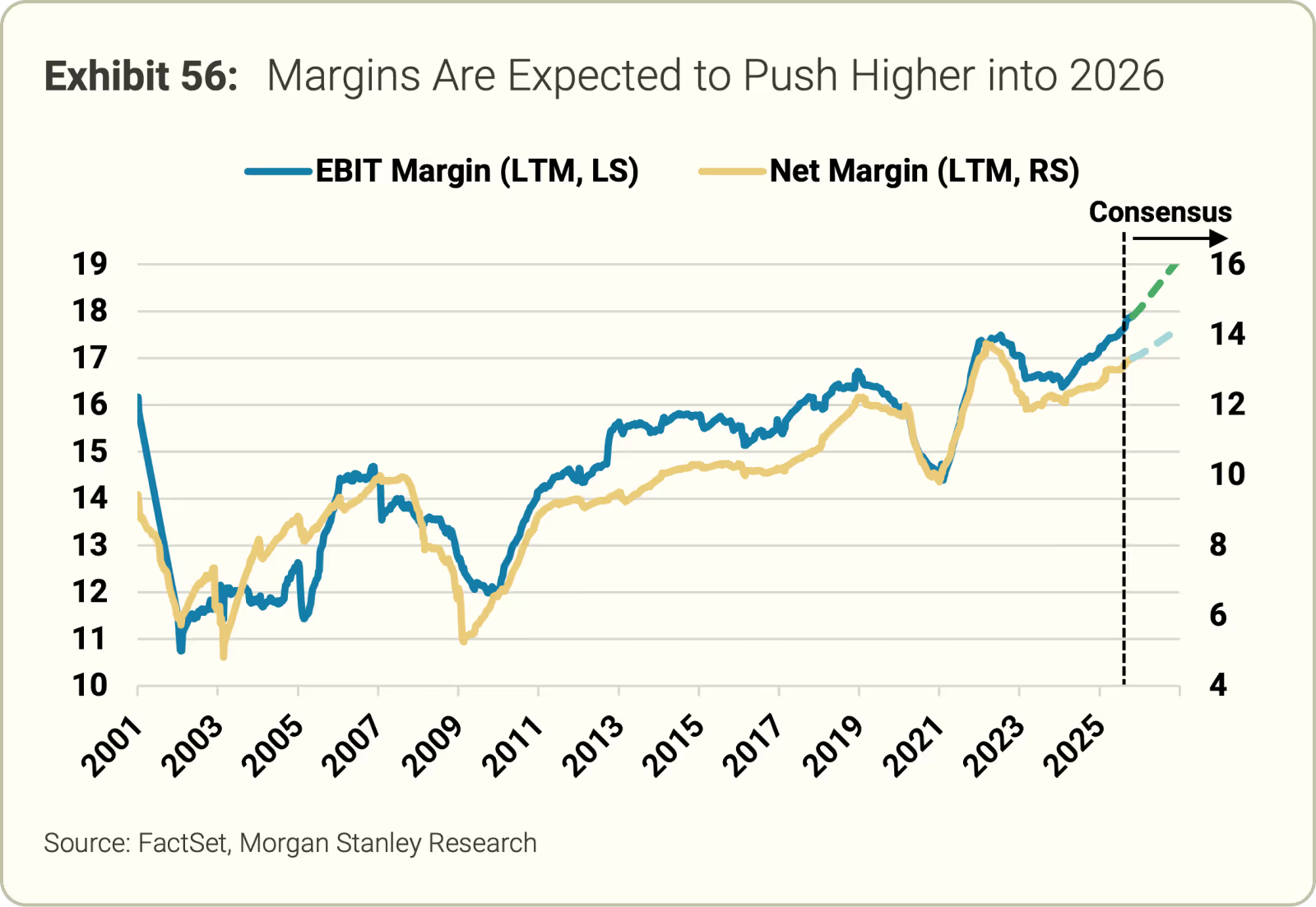

- Realized TTM EBIT margins: 17.9%

- Expected EBIT margins: 18.1% (2025), expanding to 19.1% (2026)2

If this momentum continues into 2026, equity valuations are likely to remain elevated. Ultimately, earnings drive markets—and strong profit growth continues to provide a supportive backdrop for equities.

CapEx & AI Infrastructure

One major theme emerging this quarter is the acceleration in hyperscaler capital expenditures tied to AI infrastructure and data center buildouts. Meta, Microsoft, and Google all highlighted sharp increases in capex, which collectively rose +23% sequentially and +85% year-over-year to nearly $80 billion.

Key highlights:

- Meta (META): Raised 2025 CapEx to $70–72B (from $66–72B); guided for a notably larger 2026 budget—potentially exceeding $100B (+50% y/y).

- Microsoft (MSFT): 2026 CapEx expected to rise +60% (FY June), implying ~$140B in spend.

- Alphabet (GOOG): 2025 CapEx guidance increased +74% to $91–93B, with further growth in 2026.

- Amazon (AMZN): CapEx of ~$90B YTD, tracking toward $125B for 2025 and an estimated $152B in 2026 (+22% y/y).3

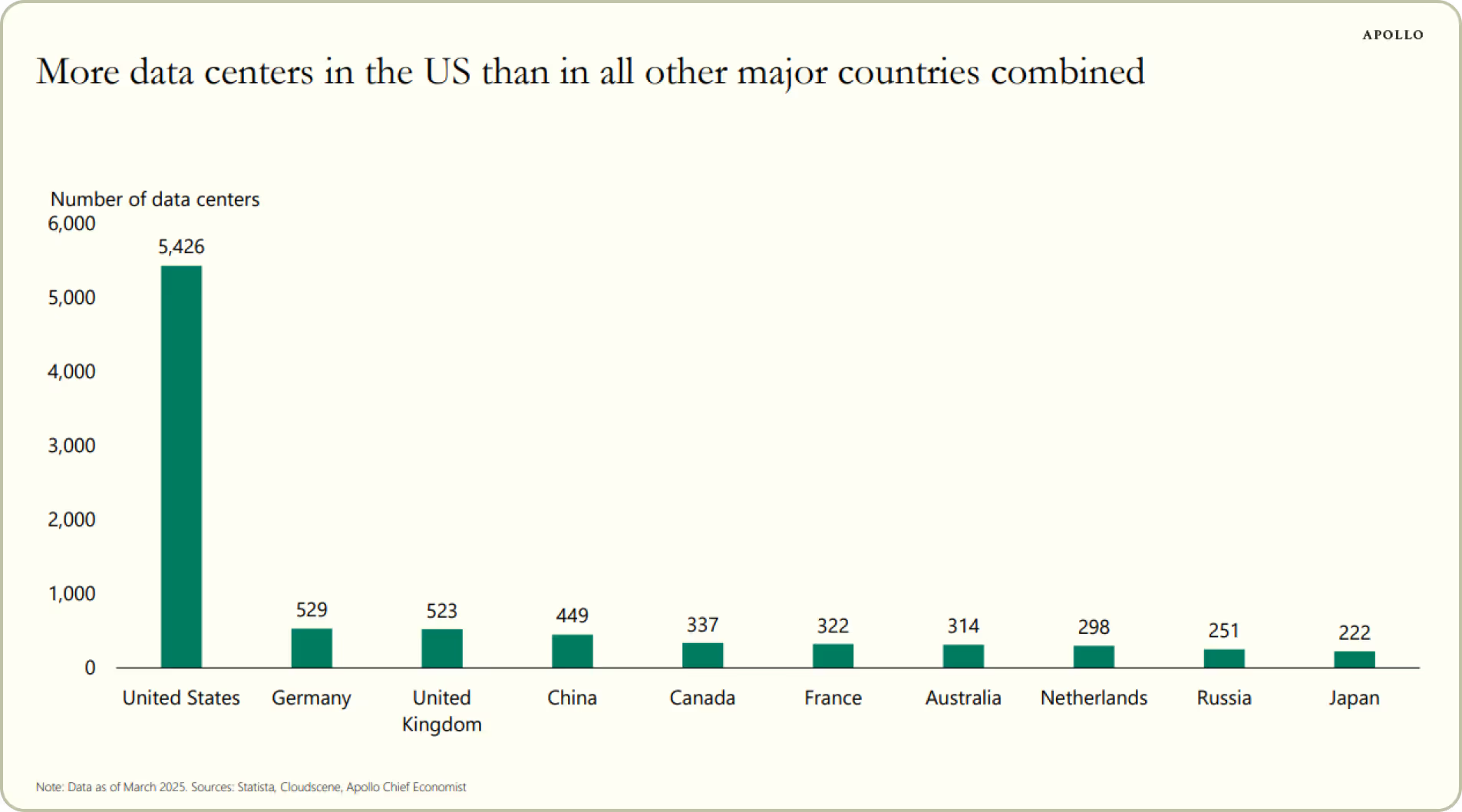

This ongoing hyperscaler investment supports near-term GDP growth and reinforces the U.S. as the global leader in AI infrastructure, with 10x more data centers than the next largest country (Germany).4

However, financing this expansion bears watching. OpenAI has committed to roughly $1.4 trillion in infrastructure spending, requiring ~30 gigawatts of data center capacity. Its recent deal with AMD—purchasing 6 gigawatts of GPUs beginning in 2H 2026, with warrants for up to 160 million AMD shares (~10% potential stake)—evokes memories of 1990s telecom “vendor financing” practices. The arrangement, which sent AMD stock surging over 50%, underscores the frothy and highly financialized nature of AI-linked investments.

The U.S. Consumer & “K-Shaped” Economy

The U.S. consumer landscape remains bifurcated: high-income households—supported by rising stock and home values—continue to spend freely, while lower-income consumers are increasingly strained. This “K-shaped” dynamic may dampen broad-based consumption but has yet to materially slow overall GDP growth.

Government Shutdown

As of November 5th, the federal government remains shut down—ongoing since October 1st—marking what will soon become the longest closure on record. The primary sticking point remains funding for Affordable Care Act (ACA) premium tax credits enacted during the pandemic, which are set to expire at year-end. Without renewal, premiums could rise an estimated 114% for many enrollees.5

Democrats have insisted on extending these subsidies as part of any continuing resolution. We expect a resolution before Thanksgiving, as Congress historically avoids remaining in session during the holidays. Note: The Senate reached an agreement to reopen the government on November 10, after this article was written.

The shutdown has disrupted key economic data releases:

- The last employment report was issued September 5th (for August).

- The most recent CPI report, released October 24th after a nine-day delay, showed both headline and core inflation rising 3% y/y.6

The CPI data will determine the 2026 Social Security cost-of-living adjustment, but overall, the Federal Reserve is operating with limited real-time data, complicating policy calibration.

Federal Reserve Update

At its October 29th meeting, the Fed cut the Federal Funds Rate by 25 basis points—its second consecutive reduction—and announced the end of quantitative tightening effective December 1st.

Chair Powell emphasized that another rate cut at the December meeting is not guaranteed, prompting a rally in Treasury yields. Futures markets now imply a 50% probability of a December cut, down from 100% prior to the meeting.7

Looking Toward Year-End

The final week of October brought clarity to several overhangs—the Fed’s trajectory, U.S.–China trade relations, and mega-cap tech earnings. As we move into the final months of the year, seasonal tailwinds and performance-chasing dynamics often favor risk assets. Historically, the S&P 500 has risen 77% of the time in November and December, and that probability climbs to 95% when the market is already up more than 15% entering November.

Reflecting on 2025, the early-year volatility proved to be one of the most attractive buying opportunities of the past three years. As we look ahead, we remain focused on identifying what the “surprise of 2026” may bring.

We thank you for your continued trust and partnership.

Farther Market Summary

___

References

- JP Morgan Earnings Call, October 10, 2025.

- Mike Wilson, Morgan Stanley Research, November 3, 2025

- Samik Chatterjee, JP Morgan Equity Research, October 29, 2025

- Dr. Torsten Slok, The Daily Spark (Apollo), October 26, 2025.

- KFF, Seeking Alpha, October 30, 2024

- US Bureau of Labor Statistics, October 24, 2025

- Federal Reserve Bank Meeting, October 29, 2025

- Barron’s Investor Circle, November 3, 2025