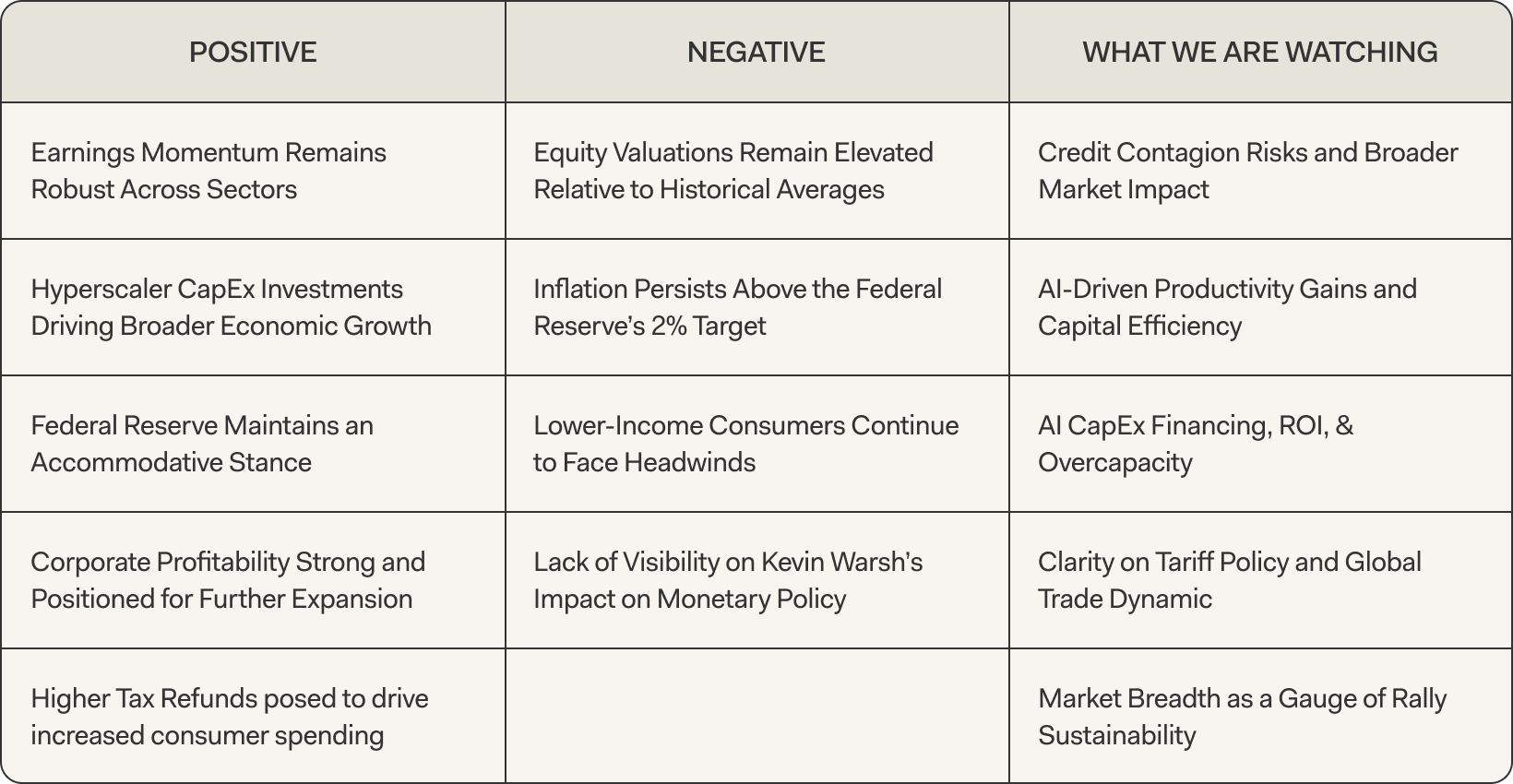

The wait is finally over….

In one of the longest and most Apprentice-like public interview sessions, President Trump announced Kevin Warsh as the successor to Jerome Powell at the end of January. Kevin Warsh brings vast experience in both the public arena as a former Fed Board member as well as in the private sector, most recently at prominent hedge fund Duquesne Capital. He also brings a distinct philosophy to the Federal Reserve in his belief that the Federal Reserve Balance Sheet is too large. He opposed QE2 in 2010 and resigned in protest. While it may be challenging to significantly reduce the Federal Reserve Balance Sheet immediately due to the composition of the Federal Reserve Board, it is safe to say that the likelihood of future Quantitative Easing has decreased significantly.

Another significant contrast between Warsh and Powell is that Kevin Warsh believes that the increased deregulatory environment and productivity gains from AI are deflationary, setting the stage for future rate cuts. Powell has led the Federal Reserve in the belief that tariffs are inflationary.

Warsh has also believed that regulatory requirements on banks have been constraining, particularly on medium and local banks. Warsh has been an opponent to paying interest on reserves held by banks. His endgame is to shrink the Federal Reserve Balance sheet, which would be supported by increased banking activity.

January market activity

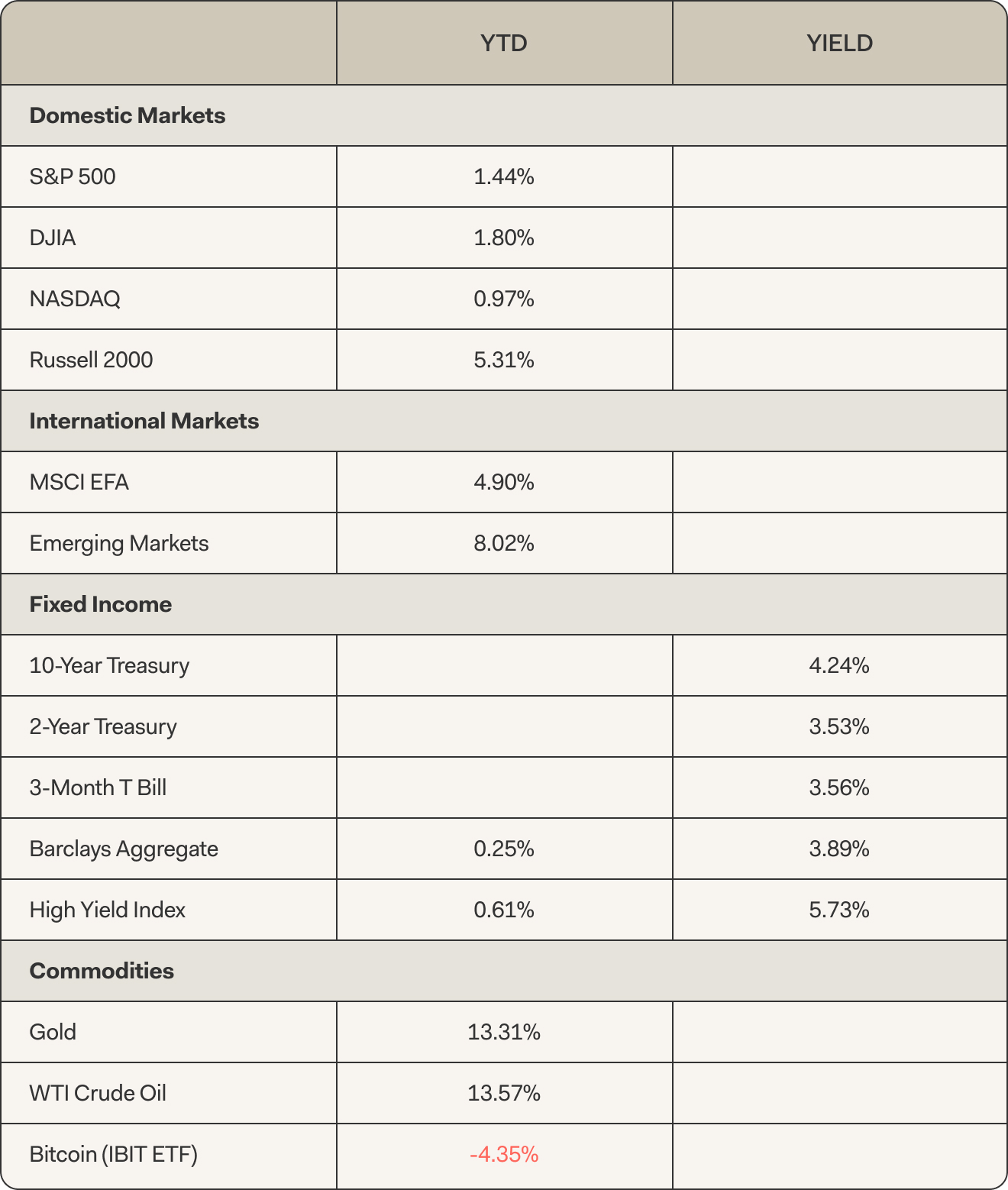

Despite headlines triggering multiple episodes of turbulence, markets delivered positive results for both equities and fixed income as the year began. The S&P 500 saw its largest single-day decline since October 2026 on January 20th when President Trump threatened new tariffs over Greenland. Within a matter of days, major benchmarks established fresh record highs, bolstered by robust corporate profit reports that have provided support for investment portfolios.

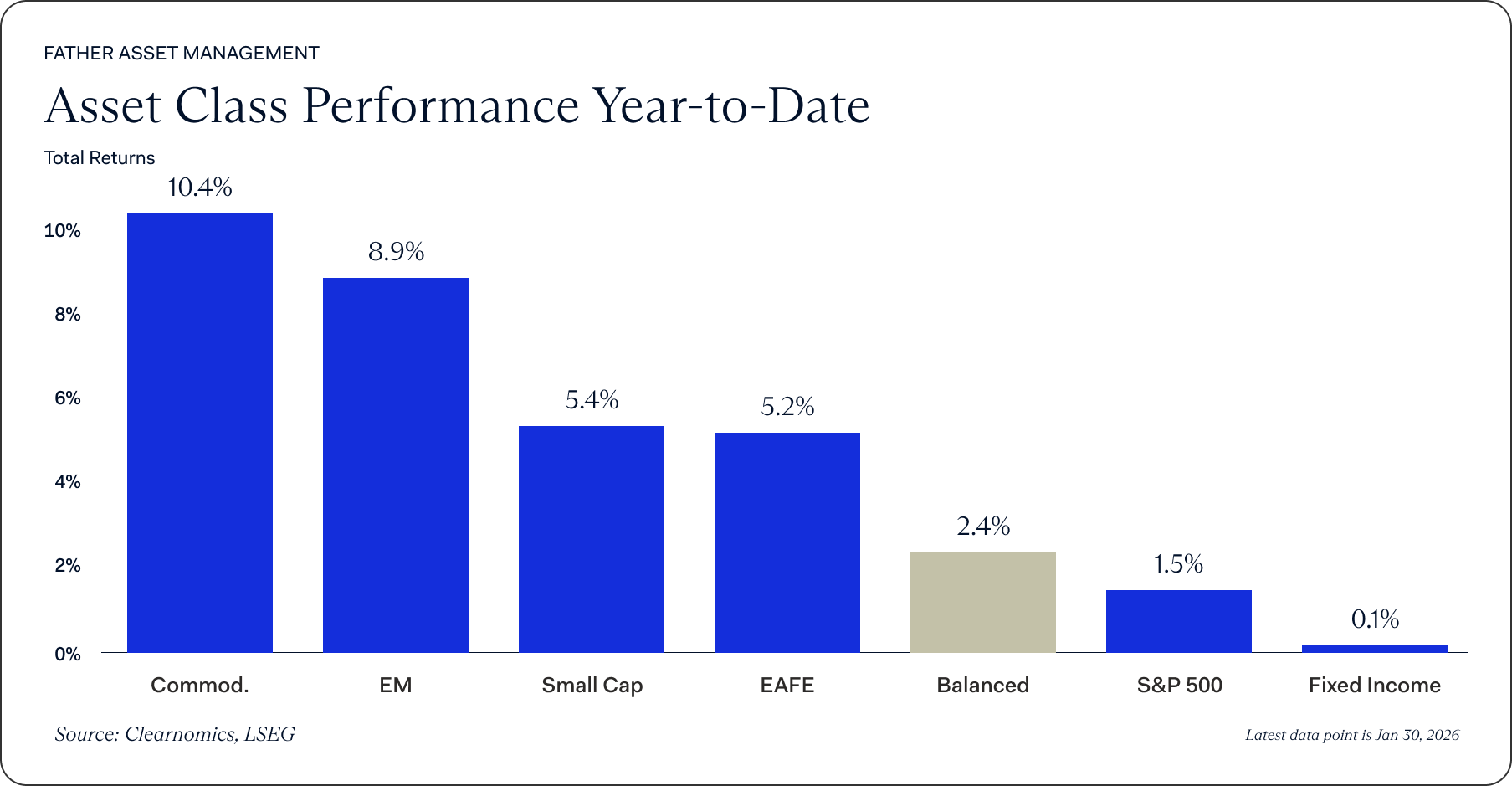

- We may be witnessing the long-awaited market broadening. While the S&P 500 advanced 1.4%, the Nasdaq Composite increased 0.9%, and the Dow Jones Industrial Average rose 1.7%, these were easily surpassed by the equal-weighted S&P (RSP) with January performances of 3.4%.

- Volatility returns. The CBOE VIX volatility index concluded the month at historical averages of 17.44 following a spike above 20 amid geopolitical concerns.

- Significant Small Cap outperformance. Small-cap stocks rallied with the Russell 2000 posting gains of 5.5% in part due to low interest rates and a favorable regulatory environment.

- International outperformed the US as International developed markets surged 5.2% in U.S. dollar terms according to the MSCI EAFE Index, while emerging markets advanced 8.8% based on the MSCI EM Index.

- Dollar decline persists. The U.S. dollar index declined further to approximately 97.0, touching its lowest point in nearly four years, before recovering modestly following the Fed Chair announcement.

- Fed held rates steady. The Federal Reserve maintained its policy target rate at 3.50 to 3.75% during its January meeting, after implementing three consecutive quarter-point reductions in the latter half of 2025.

- Inflation unchanged. Consumer Price Index inflation held steady at 2.7% year-over-year in December, remaining above the Fed's 2% objective. The Producer Price Index rose to 3.0%.1

- Wildcard weekends

- Wildcard Weekend is synonymous with football fans as the opening weekend of the NFL playoffs. However, this year it took on a different context, as a string of unexpected geopolitical events took place.

- A U.S. military operation in Venezuela during the early part of the month led to the apprehension of Nicolás Maduro. Although the mission focused on narco-terrorism concerns, discussions rapidly shifted toward petroleum implications. Venezuela possesses the world's largest confirmed oil reserves yet produces under 1% of worldwide crude output because of deteriorating infrastructure

- Geopolitical worries intensified following U.S. remarks about acquiring Greenland citing its strategic value for defense and natural resources. This triggered diplomatic tensions with NATO allies which led to retaliatory tariffs, contributing to the S&P 500's steepest decline since October of the prior year. Nevertheless, conditions rapidly improved after President Trump convened with the NATO Secretary General and outlined a "framework of a future deal," prompting markets to recover.

- January offers an important lesson for those investing with a long-time horizon: news headlines can trigger unpredictable market reactions, but underlying fundamentals and strategic financial planning ultimately drive success. Although geopolitical developments and policy questions will likely generate additional market swings in 2026, the most effective approach to manage these obstacles continues to be maintaining a well-diversified portfolio that reflects your long-term financial objectives.

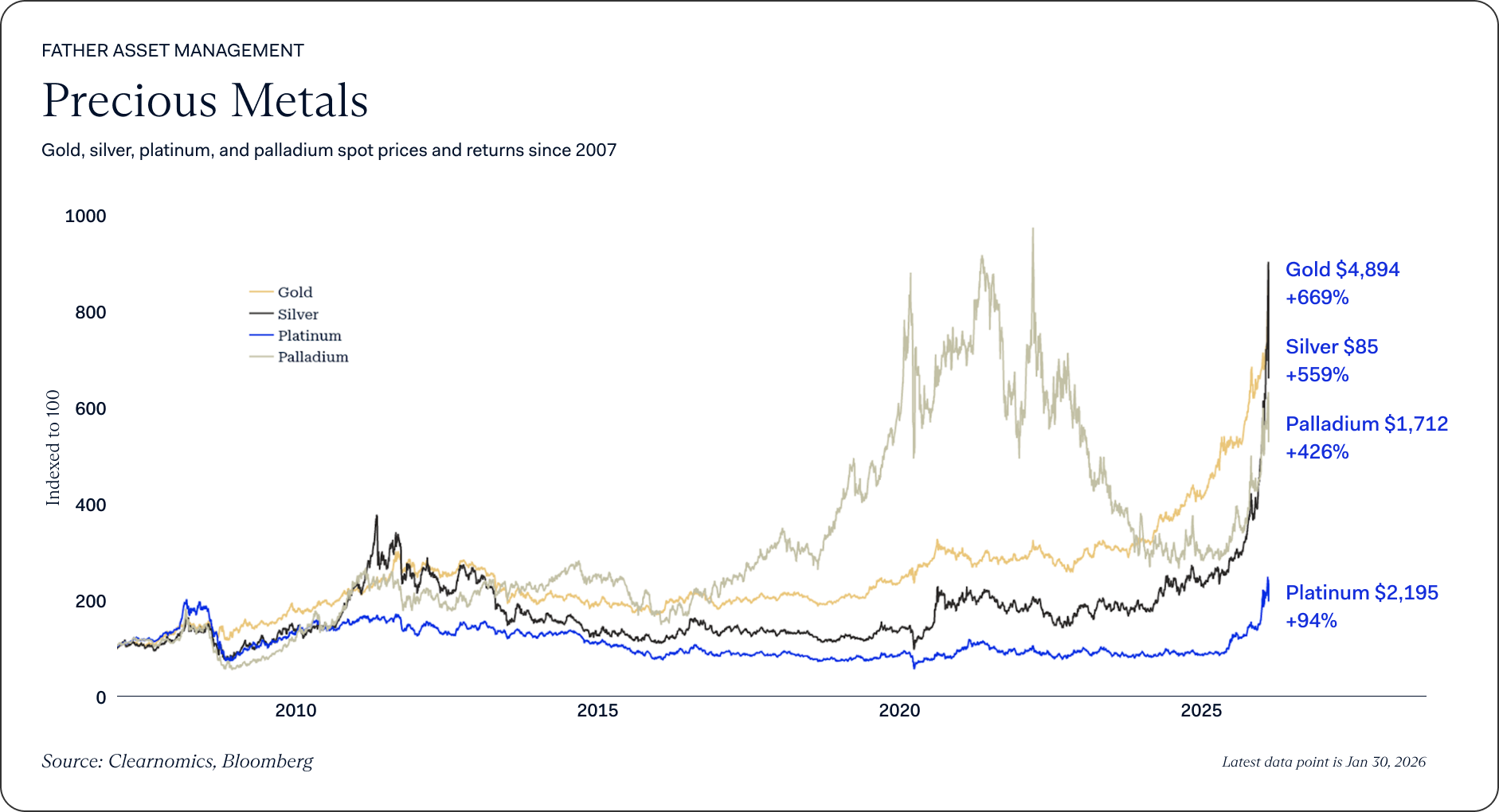

- Federal Reserve uncertainties influenced gold, silver, and currency markets

- Precious metals sustained their upward trajectory until experiencing a substantial reversal on January's final trading day. Gold approached nearly $5,600 on an intraday basis before sharply correcting 10% on January 30th to $4894. Silver's spot price surpassed $120 per ounce before dropping 26% on January 30th to $85.20. These price movements have resulted from multiple influences, including geopolitical uncertainty, central bank buying activity, and questions surrounding Federal Reserve autonomy.The forces propelling gold and silver upward have been characterized as the "debasement trade," representing the notion that fiscal and monetary approaches that effectively diminish dollar strength, generate budget shortfalls, and produce inflation may bolster precious metals. Uncertainty regarding the Fed, including speculation that a new Fed chair might pursue lower interest rates, has driven these metals to elevated levels.This sharp reversal highlights both the susceptibility of precious metals to boom-and-bust patterns and illustrates how rapidly markets can pivot based on policy outlook. Although precious metals can provide value to investors, their turbulence throughout January illustrates why they should complement, rather than substitute for, foundational positions in equities and fixed income.

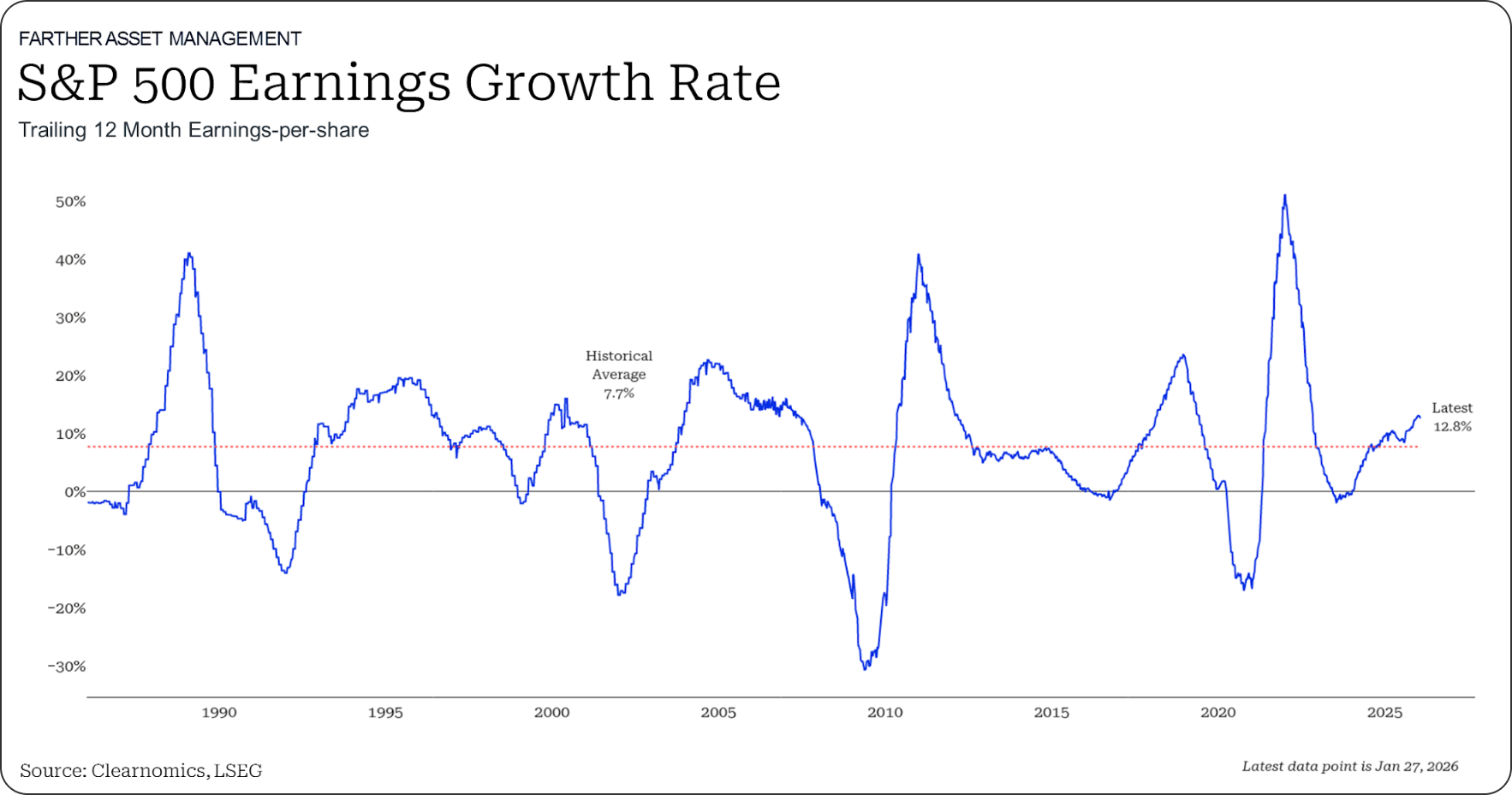

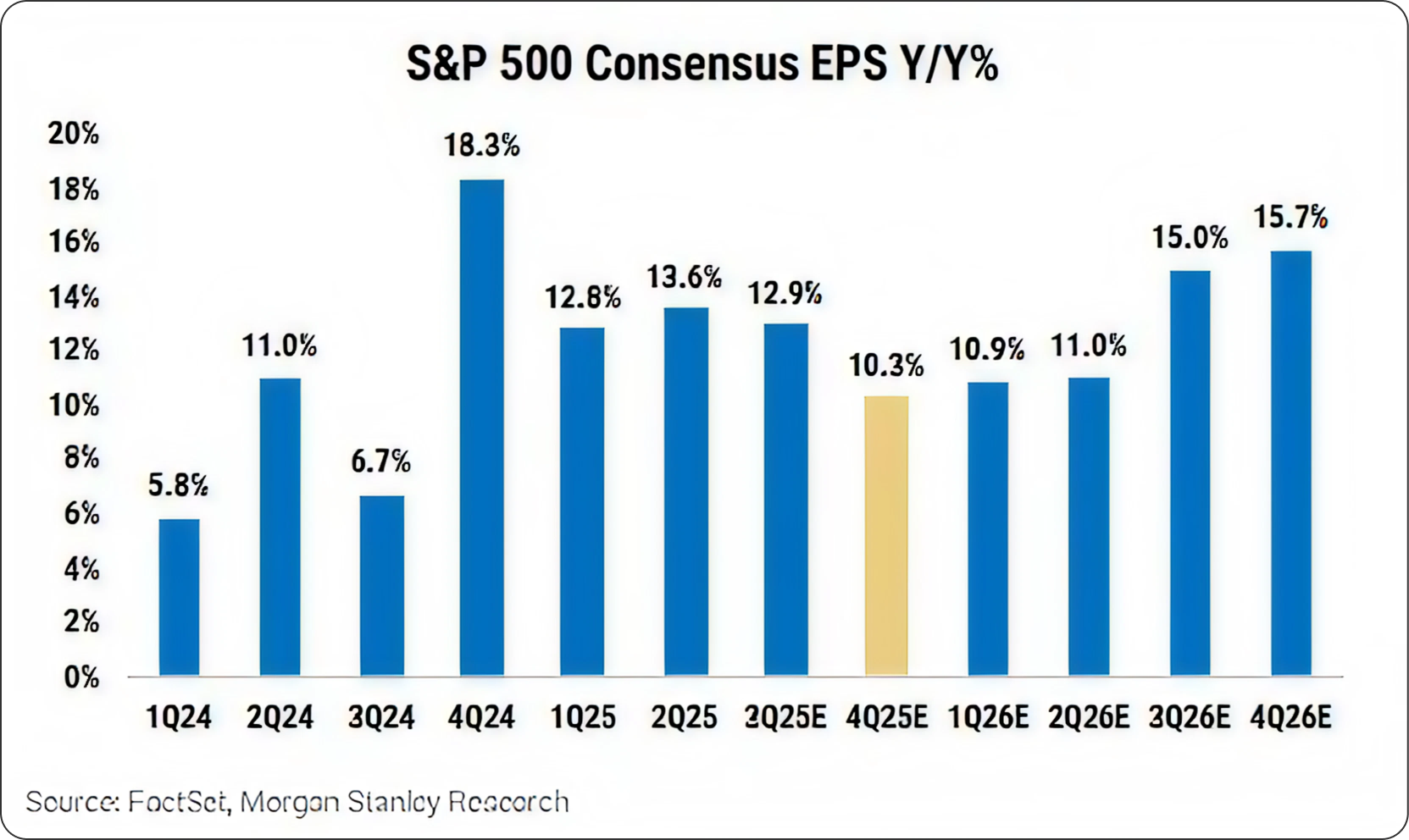

Q4 2025 earnings seasonThrough the end of January, roughly 44% of S&P 500 companies had reported fourth-quarter results. Overall, the earnings season has been strong:- Revenue surprise: +1.3% (vs. 1.3% historical average)

- EPS surprise: +9.2% (vs. 4.4% historical average)

- Consensus EPS growth: +12% for 2025, +14% for 2026

- Consensus sales growth: +6% (Q425), +4% (2025), +7% (2026)

- Realized TTM EBIT margins: 18.2%

- Expected EBIT margins: 18.4% (2025), expanding to 19.6% (2026)2

- Understandably, investors are concentrating on AI and technology sector earnings, given that these equities have driven market performance during recent years. Thus far, markets have responded inconsistently to these companies' earnings releases, even when they surpass estimates, reflecting elevated expectations and uncertainties about continued investment levels. Meanwhile, numerous other sectors have enjoyed benefits from the broader economic expansion and have increased their earnings at accelerated rates.

- For those investing with extended time frames, the fundamental takeaway from earnings season remains encouraging. Corporate profitability continues demonstrating strength across multiple sectors, justifying equity valuations. This foundational resilience explains why major benchmarks remained in positive territory for the month, notwithstanding significant volatility.

- January barometerFor those who subscribe to the Stock Trader’s Almanac, the “January barometer” is the tendency of January performance to forecast the remainder of the year (as goes January, so goes the year). Since 1928, when January is positive, the remainder of the year has been positive 79% of the time with an average gain of 9%. This compares with S&P positive returns of 71% for all years and an average gain of 6.8%. When the S&P is negative in January, the S&P is positive from February to December 59% of the time, with an average gain of 3.1%. The bottom line? January brought market fluctuations stemming from geopolitical events, Federal Reserve leadership changes, and other factors. Nevertheless, markets demonstrated resilience, and solid corporate earnings helped major benchmarks establish new record highs, even as precious metals experienced sharp reversals. For those with long-term investment horizons, this reinforces the significance of sustaining appropriate asset allocation aligned with financial objectives.

- All Performance Data is sourced from BloombergAll Performance Data includes DividendsReferences1. US Bureau of Labor Statistics, January 13, 20262. Morgan Stanley,Feb 2, 2026

Wildcard weekends

Wildcard Weekend is synonymous with football fans as the opening weekend of the NFL playoffs. However, this year it took on a different context, as a string of unexpected geopolitical events took place.

A U.S. military operation in Venezuela during the early part of the month led to the apprehension of Nicolás Maduro. Although the mission focused on narco-terrorism concerns, discussions rapidly shifted toward petroleum implications. Venezuela possesses the world's largest confirmed oil reserves yet produces under 1% of worldwide crude output because of deteriorating infrastructure

Geopolitical worries intensified following U.S. remarks about acquiring Greenland citing its strategic value for defense and natural resources. This triggered diplomatic tensions with NATO allies which led to retaliatory tariffs, contributing to the S&P 500's steepest decline since October of the prior year. Nevertheless, conditions rapidly improved after President Trump convened with the NATO Secretary General and outlined a "framework of a future deal," prompting markets to recover.

January offers an important lesson for those investing with a long-time horizon: news headlines can trigger unpredictable market reactions, but underlying fundamentals and strategic financial planning ultimately drive success. Although geopolitical developments and policy questions will likely generate additional market swings in 2026, the most effective approach to manage these obstacles continues to be maintaining a well-diversified portfolio that reflects your long-term financial objectives.

Federal Reserve uncertainties influenced gold, silver, and currency markets

Precious metals sustained their upward trajectory until experiencing a substantial reversal on January's final trading day. Gold approached nearly $5,600 on an intraday basis before sharply correcting 10% on January 30th to $4894. Silver's spot price surpassed $120 per ounce before dropping 26% on January 30th to $85.20. These price movements have resulted from multiple influences, including geopolitical uncertainty, central bank buying activity, and questions surrounding Federal Reserve autonomy.

The forces propelling gold and silver upward have been characterized as the "debasement trade," representing the notion that fiscal and monetary approaches that effectively diminish dollar strength, generate budget shortfalls, and produce inflation may bolster precious metals. Uncertainty regarding the Fed, including speculation that a new Fed chair might pursue lower interest rates, has driven these metals to elevated levels.

This sharp reversal highlights both the susceptibility of precious metals to boom-and-bust patterns and illustrates how rapidly markets can pivot based on policy outlook. Although precious metals can provide value to investors, their turbulence throughout January illustrates why they should complement, rather than substitute for, foundational positions in equities and fixed income.

Q4 2025 earnings season

Through the end of January, roughly 44% of S&P 500 companies had reported fourth-quarter results. Overall, the earnings season has been strong:

- Revenue surprise: +1.3% (vs. 1.3% historical average)

- EPS surprise: +9.2% (vs. 4.4% historical average)

- Consensus EPS growth: +12% for 2025, +14% for 2026

- Consensus sales growth: +6% (Q425), +4% (2025), +7% (2026)

- Realized TTM EBIT margins: 18.2%

- Expected EBIT margins: 18.4% (2025), expanding to 19.6% (2026)2

If this momentum continues into 2026, equity valuations are likely to remain elevated. Ultimately, earnings drive markets—and strong profit growth continues to provide a supportive backdrop for equities.

Understandably, investors are concentrating on AI and technology sector earnings, given that these equities have driven market performance during recent years. Thus far, markets have responded inconsistently to these companies' earnings releases, even when they surpass estimates, reflecting elevated expectations and uncertainties about continued investment levels. Meanwhile, numerous other sectors have enjoyed benefits from the broader economic expansion and have increased their earnings at accelerated rates.

For those investing with extended time frames, the fundamental takeaway from earnings season remains encouraging. Corporate profitability continues demonstrating strength across multiple sectors, justifying equity valuations. This foundational resilience explains why major benchmarks remained in positive territory for the month, notwithstanding significant volatility.

January barometer

For those who subscribe to the Stock Trader’s Almanac, the “January barometer” is the tendency of January performance to forecast the remainder of the year (as goes January, so goes the year). Since 1928, when January is positive, the remainder of the year has been positive 79% of the time with an average gain of 9%. This compares with S&P positive returns of 71% for all years and an average gain of 6.8%. When the S&P is negative in January, the S&P is positive from February to December 59% of the time, with an average gain of 3.1%.

The bottom line? January brought market fluctuations stemming from geopolitical events, Federal Reserve leadership changes, and other factors. Nevertheless, markets demonstrated resilience, and solid corporate earnings helped major benchmarks establish new record highs, even as precious metals experienced sharp reversals. For those with long-term investment horizons, this reinforces the significance of sustaining appropriate asset allocation aligned with financial objectives.

All Performance Data is sourced from Bloomberg

All Performance Data includes Dividends

References

1. US Bureau of Labor Statistics, January 13, 2026

2. Morgan Stanley,Feb 2, 2026