RATE HIKES

Global investors are facing a challenging market environment, with expectations of higher inflation, tighter monetary policy and now, the impacts of the Russia-Ukraine war. As widely anticipated, the Federal Reserve raised the Fed Funds rate by 0.25% to 0.25%-0.50% during the March Federal Open Market Committee (FOMC) meeting, its first interest rate hike since December 2018. We think interest rates — especially for long-term yields — are likely to rise further this year, driven by expectations of above potential GDP growth, tighter monetary policy, and inflation that is much above the Fed’s target of 2%.

We prefer a multi-asset framework as investors navigate the upcoming hiking cycle. In equities, selectivity within sectors plays an even more important role, and we prefer picking pockets of the market with strong pricing power and resilient margins in a rising rate environment. On this front, sectors and subsectors in tech, healthcare, and communication are worth noting.

Changes in rate hike expectations

STOCKS

Historical analysis shows that value exposures have tended to outperform in a rising yield environment as it coincides with rising inflation. Despite the value sectors’ recent outperformance versus the growth sectors of the market, value still appears attractive, as its 12 month forward looking Price to Earnings ratio (PE) remains low. We prefer seeking ‘value’ within the value basket, particularly in the financials and energy sectors, which typically exhibit greater sensitivity to higher interest rates.

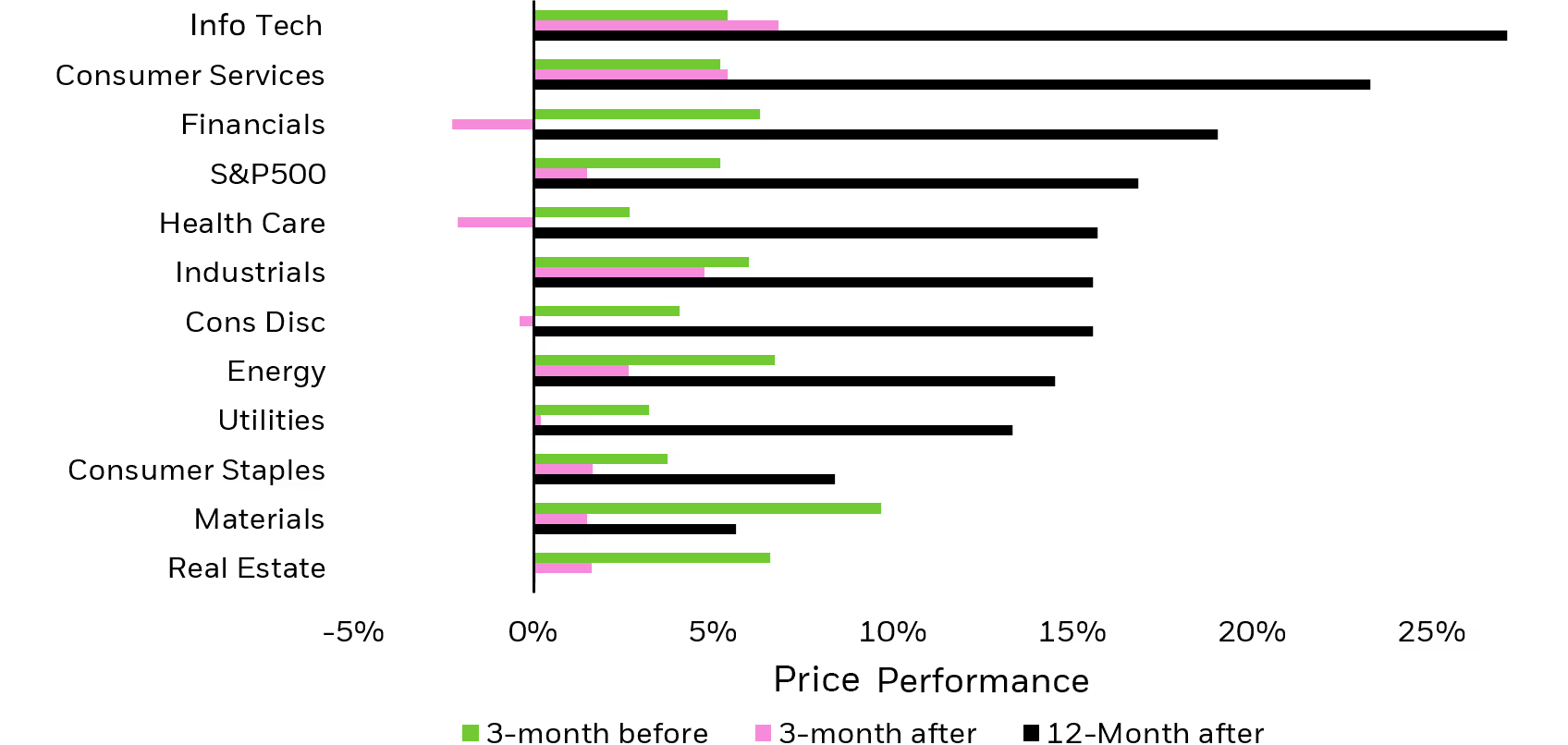

Average sector performance before and after the beginning of new rate hike cycles

The rise in interest rates since the start of the year has weighed on risk sentiment and triggered selloffs in growth sectors of the market. However, we believe that technology exposures could potentially outperform the broader market after initial rate moves. Despite higher interest rates, we think real rates are likely to remain in negative territory, supporting global equities. With higher rates and a higher inflation backdrop, we prefer industries that can take advantage of the rising costs and pass prices to consumers, such as quality companies — companies with stable cashflows and higher profit margins — and industries such as semiconductors.

BONDS

In a rising rate environment, traditional bonds can lose value, but investors should not write off fixed income exposure altogether. We believe allocations to inflation-linked bonds can potentially outperform fixed-rate bonds as inflation remains elevated, while allocations to floating rate bonds could also outperform in rising rate environments. Of course, bonds can provide diversification in times of geopolitical turmoil. Finally, for those looking for income, exposure to shorter duration credit bonds can also be an alternative as shorter duration bonds are less sensitive to interest rate changes.

COMMODITIES

Exposure to broad commodities can provide diversification in a multi-asset portfolio and can potentially hedge against interest rate risk. Now, given the war in Ukraine, we have seen commodities rally as Russian isolation chokes supplies of energy, agriculture, and metals. This could add to higher inflation, which we think could persist at above-trend levels into late 2022, providing a strong backdrop for commodities.

From the Farther Wealth Advisory Team, with insights from our partners at BlackRock.