401(a) vs 401(k): Key Differences Explained

Confused by the alphabet soup of retirement plans? You're not alone. When it comes to securing your future, understanding the difference between a 401(a) and a 401(k) plan is crucial - and it might be simpler than you think.

A 401(a) is often offered by government agencies or nonprofits, while a 401(k) is popular in the private sector. Each has unique rules on contributions, taxes, and withdrawals that can impact your future.

This blog will explain how these plans work and compare them side by side, highlighting their similarities and differences, so that you can feel confident about where you're putting your money.

Key Takeaways

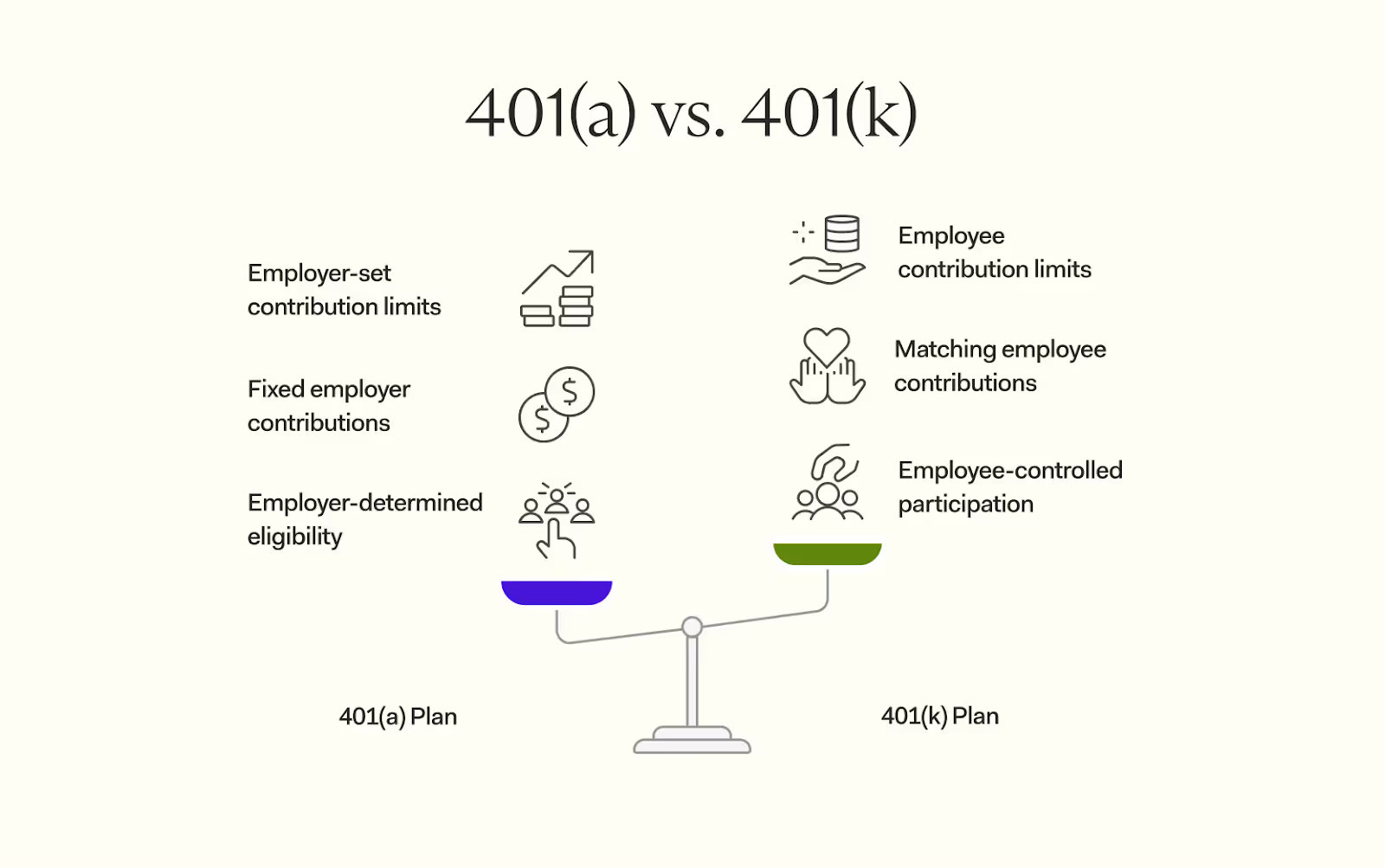

- A 401(a) is common in government or nonprofit jobs, while a 401(k) is popular in private companies. Eligibility and rules differ based on the employer.

- Both plans have tax-deferred growth and pre-tax contributions. Some 401(k)s also allow Roth options for after-tax contributions with tax-free withdrawals later.

- Investment options vary—401(k)s usually offer more flexibility like stocks and mutual funds, while 401(a)s often limit choices set by employers.

- Early withdrawals before age 59½ face a 10% penalty plus taxes unless exceptions apply. Both require Required Minimum Distributions (RMDs) starting at age 73.

What Is a 401(a)?

This type of employer-sponsored retirement plan is common in educational institutions, government agencies, and nonprofit organizations. Employers create it to help employees save for retirement.

Employers set the rules for contributions. They may require employees to contribute or make voluntary contributions themselves. An employee's contribution is typically made with pre-tax dollars, reducing taxable income now.

The plan offers tax-deferred growth on savings until withdrawal during retirement.

What Is a 401(k)?

Employees can contribute pre-tax or after-tax dollars from their paycheck into this retirement savings plan offered by employers. Contributions grow tax-deferred, meaning you don't pay taxes on earnings until you withdraw money.

Employers may offer matching contributions to boost your savings. The annual contribution limit for employees under 50 is $24,500 in 2026. Those aged 50 or older can make an extra catch-up contribution of $8,000, with a higher catch-up contribution limit applicable for certain age groups in 2026 due to the SECURE 2.0 legislation.

Funds are often invested in mutual funds, stocks, or bonds to help build long-term growth toward retirement goals.

Brief History of 401(a) and 401(k) Plans

The journey of 401(a) and 401(k) plans began in the late 20th century, transforming how Americans save for retirement. The 401(k) plan was introduced in 1978 as part of the Revenue Act, providing a new way for employees to save for retirement with tax-deferred contributions. This innovation allowed employees to set aside a portion of their paycheck into a retirement account, growing their savings without immediate tax implications.

In the 1980s, the 401(a) plan emerged, tailored specifically for government and non-profit organizations. This plan aimed to offer similar tax-deferred benefits but was designed to meet the unique needs of public sector employees.

Significant legislative changes have shaped these plans over the years. The Economic Growth and Tax Relief Reconciliation Act (EGTRRA) of 2001 increased contribution limits, allowing employees to save more for their retirement. More recently, the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 introduced new rules, such as raising the age for Required Minimum Distributions (RMDs) and expanding access to retirement plans.

Today, both 401(a) and 401(k) plans are cornerstone retirement savings vehicles in the United States. They offer employees in various sectors a structured, tax-advantaged way to build their retirement nest egg, adapting over time to meet evolving financial landscapes and retirement needs.

Key Differences Between 401(a) and 401(k)

These retirement plans differ in eligibility, contributions, limits, and investment options—learn how these distinctions affect your retirement savings.

Eligibility and Employee Participation

401(a) plans are usually offered by government employers, schools, or nonprofits. Employers decide who can join the plan and set strict rules for participation. Employees often must meet specific criteria, like working a certain number of hours or being full time.

401(k) plans are more common in the private sector. Any eligible employees—often those over 21—can participate if their employer offers it. Employees have more control in deciding how much to contribute from their paycheck. The eligibility rules depend on whether it's a 401(a) or 401(k)—one is chosen by employers, the other by you. Understanding 401(k) plans similarities can help clarify these eligibility criteria.

Employer Contributions

Employers decide how much to contribute to 401(a) plans. Contributions often depend on the employer's policy and may be required or optional. Some employers match a percentage of employee contributions, while others set fixed amounts.

401(k) plans usually offer matching contributions based on what employees put in. For example, an employer might match up to 5% of an employee's salary. These contributions are pre-tax dollars and grow tax-deferred until withdrawal. The amount of the saver's credit an employee can claim is directly dependent on the employee's adjusted gross income.

Contribution Limits

401(a) plans have a fixed contribution limit set by the employer, unlike 401(k) plans which have different contribution rules. For 2026, total contributions (employer and employee) cannot exceed $72,000 or 100% of the employee's annual compensation—whichever is lower.

Employers decide whether employees contribute pre-tax or after-tax dollars.

401(k) plans allow employees to contribute up to $24,500 in 2026. Those aged 50 or older can make catch-up contributions of an additional $8,000. Combined employer and employee contributions must stay within a $72,000 cap for the year.

Investment Options

Contribution limits affect how you allocate funds—but investment options shape where that money grows. 401(k) plans often provide a wide range of choices, like mutual funds, stocks, and bonds.

Many private sector employees favor these flexible options to build their retirement accounts.

401(a) plans tend to have fewer investment options. The employer typically decides the available options based on the plan documents. These could include safer investments like government securities or fixed-income assets.

Your choices depend heavily on your specific employer-sponsored plan's structure.

Tax Advantages

Both 401(a) and 401(k) plans offer tax advantages. Contributions to these accounts are often made with pre-tax dollars, lowering taxable income for the year. Taxes on earnings grow on a tax-deferred basis—meaning you don't pay taxes until withdrawal.

Roth options in some 401(k) plans allow after-tax contributions. This means no taxes on qualified withdrawals during retirement. Both types of plans help reduce income taxes now or later, depending on how you choose to contribute.

Withdrawal Rules for 401(a) and 401(k)

Both 401(a) and 401(k) plans have specific rules for withdrawing funds. These rules affect taxes, penalties, and how much you can access.

- Withdrawals are taxed as ordinary income. The money is taxed in the year you take it out since contributions were made pre-tax.

- Withdrawing funds before age 59½ triggers a 10% early withdrawal penalty unless exceptions apply. Exceptions include disability or certain hardships.

- Required Minimum Distributions (RMDs) start at age 73 (updated via SECURE Act 2.0). You must take out a minimum amount each year after this age.

- Loans may be allowed from both account types, but terms depend on your plan documents. Check with your plan administrator for the rules.

- Hardship withdrawals may be permitted for emergencies like medical expenses or buying a home. These typically still face taxes and possible penalties.

- Rolling over funds to another qualified retirement plan or IRA avoids taxes and penalties if done properly within 60 days of distribution.

- After-tax contributions in a Roth-based option of either plan allow tax-free withdrawals if held for five years and distributed after qualifying events like reaching age 59½.

- The employer-sponsored retirement accounts must follow IRS withdrawal rules strictly to avoid disqualification as a tax-advantaged account type.

Rollover Rules Between 401(a) and 401(k)

You can roll over funds from a 401(a) plan to a 401(k) if the new plan allows it. This process moves pre-tax dollars without owing taxes, keeping your savings tax-advantaged.

Ask your plan administrator for details on eligibility and steps. Rollovers must follow IRS rules to avoid penalties or additional taxes. Next, we'll explore pros and cons of 401(a) plans.

Vesting Rules for 401(a) and 401(k) Plans

Understanding vesting rules is crucial for maximizing the benefits of your retirement plan. Vesting determines when you gain full ownership of the employer contributions made to your retirement account.

In 401(a) plans, vesting rules are often more stringent. Employers may require a specific number of years of service before you become fully vested. For instance, you might need to work for five years to be 100% vested in the employer's contributions. This means if you leave the job before completing the required years, you might forfeit some or all of the employer's contributions.

On the other hand, 401(k) plans typically offer more flexible vesting schedules. Some employers provide immediate vesting, granting you full ownership of employer contributions from day one. Others may implement a graded vesting schedule, where you gradually become vested over a period, such as 20% per year over five years.

These vesting rules can significantly impact your retirement savings, especially if you change jobs frequently. It's essential to review your plan documents to understand the specific vesting schedule that applies to your retirement account. Knowing these details helps you make informed decisions about your career and retirement planning, ensuring you maximize the benefits of your employer's contributions.

Pros and Cons of 401(a) Plans

401(a) plans are employer-sponsored retirement accounts. They have unique rules and benefits but come with a few drawbacks.

Pros:

- Employer decides the rules for contributions, which can include mandatory employee participation.

- Both employee and employer contributions grow on a tax-deferred basis.

- Plans are typically offered to employees in public or non-profit sectors, making them accessible to many workers.

- Employers can contribute larger amounts compared to some retirement plans, offering higher savings potential.

- Provides pre-tax contributions, reducing an employee's adjusted gross income for tax purposes.

- Eligible employees can benefit from a tax credit, such as the savings credit, which incentivizes retirement savings by reducing tax liability based on age, dependency status, and adjusted gross income.

Cons:

- Limited investment options—employer controls where funds can be invested.

- Mandatory contributions may reduce take-home pay if required by the plan's design.

- 401(a) withdrawals before age 59½ usually face a 10% IRS penalty, along with taxes owed on amounts withdrawn early.

- Catch-up contribution limits may not apply in the same way as private-sector 401(k) plans, potentially reducing late-career saving opportunities.

- Not widely available like 401(k) plans—primarily focused on government or educational employers.

Pros and Cons of 401(k) Plans

401(k) plans are popular employer-sponsored retirement accounts. They offer many benefits but come with some drawbacks.

Pros:

- Employees can contribute pre-tax dollars, reducing taxable income. This helps save on taxes now.

- Employer matching contributions add free money to employees' accounts. Many companies offer this perk.

- Contributions grow tax-deferred until withdrawal. Earnings compound without yearly taxes eating into gains.

- Plans often include diverse investment options like mutual funds and stocks, allowing flexibility.

- Loans against the account may be allowed if needed for emergencies or major expenses.

Cons:

- Withdrawals before age 59½ are subject to a 10% IRS penalty plus regular income taxes. Exceptions apply but are limited.

- Contributions are capped annually—once limits are hit, no more savings in that year's plan is possible.

- Investment fees and administrative costs can reduce growth over time.

- Market performance affects account value; poor choices or downturns pose risks.

- Not all employers provide matching contributions; this varies widely between companies.

Which Plan Is Right for You?

Your choice depends on your job and savings goals. 401(a) plans are common for government or non-profit workers, offering more employer control over contributions. In contrast, 401(k) plans are typical in the private sector, giving employees flexibility with how much they contribute.

Think about whether you value fixed rules or prefer more control over your retirement account. Consider factors like catch-up contributions, tax benefits, and investment options specific to each plan's limits.

Review withdrawal rules before deciding which works best for long-term needs.

Conclusion

So, which retirement plan is right for you? While both 401(a) and 401(k) plans help you save for the future, they're designed for different situations. If you work in the public sector, a 401(a) might be your path. In the private sector, a 401(k) is more likely your ticket to retirement savings.

Take time to understand what your employer offers and how it fits your long-term goals. Your contributions today - and how they're taxed - can make a big difference in your retirement. Not sure about the details? A quick chat with your HR team or a financial advisor can help you make the right choice.

FAQs

1. What is the main difference between a 401(a) and a 401(k)?

The main difference is that a 401(a) plan is typically offered by government or non-profit employers, while 401(k) plans are more common in for-profit companies.

2. How are contributions made to these retirement accounts?

In a 401(a), both the employer and employee may contribute, but the employer decides how much employees must contribute. In contrast, with a 401(k), employees decide their contribution amount, often matched partially by employers.

3. Are contributions pre-tax or after-tax dollars?

Both plans allow tax-deferred contributions using pre-tax dollars, though some 401(k) plans also permit after-tax contributions depending on plan documents.

4. What are the similarities between these two types of retirement accounts?

Both are defined contribution plans that offer tax-advantaged growth and require taxes to be paid when funds are withdrawn during retirement.

5. Is there a catch-up contribution limit for older employees?

Yes! Employees aged 50 or older can make catch-up contributions—up to $8,000 annually—in both types of plans under current Internal Revenue Code rules. Additionally, in 2026, individuals aged 60 to 63 can make enhanced catch-up contributions of up to $11,250 annually.

6. Where can I find specific details about my plan?

Check your plan documents or contact your plan administrator for information on limits, employer matches, and other features unique to your account type.