Would you rather have guaranteed monthly income or the chance to double your retirement savings?

This question faces every retiree. Annuities promise security with predictable payments for life, regardless of market conditions. They provide peace of mind but typically offer lower returns and less flexibility.

Stocks offer growth potential that can outpace inflation and build significant wealth over time. However, this comes with market volatility and no income guarantees.

This guide helps you evaluate which approach aligns with your retirement timeline, risk tolerance, and lifestyle goals. Understanding the strengths and limitations of both options is crucial for creating a retirement strategy that works for your specific situation.

Overview of Annuities

Annuities are contracts with an insurance company that provide either immediate or deferred regular income in exchange for an initial payment. Immediate annuities start paying shortly after the investment, while deferred annuities begin payments at a future date.

Types of Annuities: Fixed, Variable, and Indexed

Different types of annuities suit various financial needs, each offering unique benefits and risks.

- Fixed annuities promise a guaranteed return rate and provide benefits similar to CDs, such as tax-deferred growth and potential for lifetime income, distinct from CDs which do not offer these features.

- Variable annuities let you invest in portfolios similar to mutual funds. Your payouts can go up or down based on how these investments perform. It's riskier than fixed annuities because you can lose money if the market performs poorly. Still, there's potential for higher returns.

- Indexed annuities are a mix of fixed and variable types. Your returns are tied to a stock market index, like the S&P 500, but you have some protection against loss. If the market goes up, you get more money, up to a cap. If it goes down, you usually won't lose your initial investment. This gives you a chance at higher gains without full market risk.

Benefits of Annuities

Steady income is a key advantage of annuities. They provide regular payments during retirement, making them popular for those seeking reliable income streams. Fixed annuities guarantee a set amount of money, while variable annuities allow you to invest in stocks and mutual funds, giving you growth potential.

Tax-deferred growth is another advantage. You don't pay taxes on your earnings until you withdraw them. This can enhance your overall returns over time. Annuities are backed by the claims-paying ability of insurance companies, which varies based on the insurer's financial stability and ratings, adding a varying level of security to your financial future.

Many investors appreciate this stability as they plan their retirement savings options.

Drawbacks of Annuities

Several drawbacks come with annuities, depending on their type and structure. They often include fees, which can vary widely, such as administrative fees and surrender charges that can affect your returns over time. With variable annuities, market performance directly affects your income. If the market drops, so does your payout.

Liquidity is another issue. Annuities tie up funds for many years. You might face penalties if you withdraw money early. Unlike stocks, which have greater liquidity, getting cash from an annuity isn't easy or quick.

Plus, once you start taking income from the annuity, it gets taxed as ordinary income—this isn't always ideal for retirement planning.

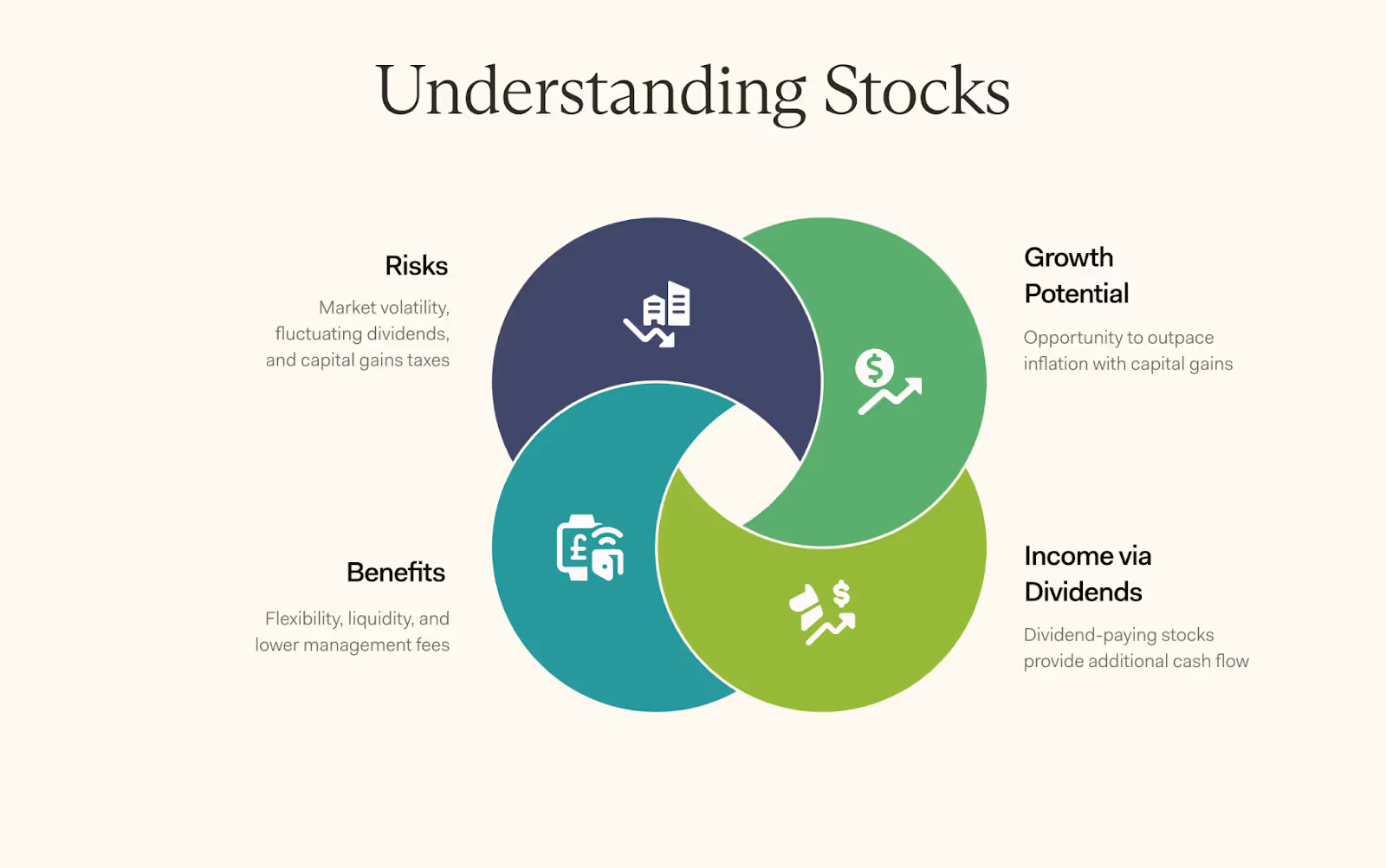

Overview of Stocks

Shares of companies that you can buy represent stocks, though not all provide dividends. Some companies reinvest profits back into the business instead of distributing them to shareholders. This, along with their growth potential, makes them a popular choice for many investors.

Dividend Stocks and Growth Potential

A way to earn income from your investments comes through dividend stocks. These stocks pay out dividends regularly, providing cash flow for retirement income. Some companies increase their dividend payouts over time.

This growth potential can add value to your portfolio.

Investing in dividend stocks can also have tax benefits. Qualified dividends are generally taxed at capital gains tax rates, which can be lower than ordinary income tax rates, depending on the investor's income and filing status. You can reinvest these dividends or withdraw funds as needed.

Growth prospects look good for many blue-chip companies that have strong track records of paying dividends. Many investors like this steady income stream, especially during market volatility.

Benefits of Stocks

Many benefits come with stocks for retirement income. They can provide growth potential, meaning that over time, the stock price might increase. Investors can earn money when they sell at a higher price than they bought.

Stocks also include dividend stocks, which pay out cash regularly. These dividends come from the issuing company's profits.

While stocks themselves do not incur management fees, investing in stocks through vehicles like mutual funds or ETFs can involve management fees. Annuities might have higher fees due to their insurance features and guarantees.

Building a diverse dividend stock portfolio helps manage risk and maximize returns over time. Many investors find stocks appealing because of their liquidity and flexibility—meaning it's easy to buy or sell them when needed.

Risks of Investing in Stocks

Several risks accompany stock investments. Stock prices can rise or fall quickly, meaning you could lose money fast. Market changes, economic shifts, and company news all affect stock value.

Stocks also carry investment risk. Unlike fixed annuities, where returns are steady, stocks are less predictable. You might not receive a dividend if the company struggles. Capital gains taxes apply to profits from the sale of stocks, but the actual impact depends on the holding period and the investor's tax bracket, with long-term gains typically taxed at lower rates.

It's vital to assess your risk tolerance before investing in stocks or other mutual funds for retirement income.

Key Differences Between Annuities and Stocks

The contrast between these options is significant. Annuities offer steady income, while stocks can grow your money over time. Stocks come with risks, but they also have the potential for big gains. Annuities provide guaranteed payments, which can feel safer.

Each option has tax implications and different levels of flexibility.

Risk and Return

High returns can come from investing in stocks. Common stocks may grow over time and often pay dividends, providing regular income. However, they come with risks too. The stock market can be unpredictable.

Prices may rise and fall quickly.

More stability but usually lower returns than stocks come with annuities. A fixed annuity guarantees a steady payment, while a variable annuity's return depends on the market performance of certain investments like mutual funds.

Annuity contracts allow for tax-deferred growth until you withdraw your money, which is an appealing feature for many savers planning retirement incomes. Still, some fees might apply with these contracts!

Tax Implications

Different tax rules apply to annuities and stocks. Annuities often grow without taxes, called tax-deferred growth. You pay taxes on your earnings only when you take money out. This can be a good thing if you plan to wait until you're in a lower tax bracket.

Stocks may offer dividends that are taxed as income. This means you pay taxes on those earnings each year. When selling stocks for profit, you might face capital gains taxes too. It's smart to think about these tax implications before deciding between annuities vs stocks for retirement income.

Liquidity and Flexibility

More liquidity comes with stocks than annuities. You can buy or sell stocks anytime during market hours. This gives you quick access to cash if needed. Annuities, on the other hand, often lock your money in for a specified number of years.

Cashing out early could lead to penalties and fees from the issuing insurance company.

Flexibility is another key factor. Stocks let you choose different investment options like dividend stocks or mutual funds based on your goals. Annuities may provide fixed income options but limit how much you can change your plan later on.

Conclusion

Distinct paths to retirement security come from annuities and stocks. Each option serves different needs.

Consider your personal risk tolerance and timeline. Your comfort with market fluctuations versus desire for guaranteed income should guide your decision.

Review all fees, growth potential, and income stability before committing. A balanced approach often works best—many successful retirees incorporate both vehicles into their retirement strategy.

Take control of your financial future today by making an informed choice aligned with your long-term goals.

FAQs

1. What's the difference between stocks and annuities for retirement income?

Stocks and annuities differ in how they provide retirement income. Stocks, including dividend growth ones or those in mutual funds, offer potential growth and income through dividends. Annuities, on the other hand, can provide tax-deferred growth with a lump sum investment.

2. Are there any fees associated with both stocks and annuities?

Yes, both types of investments come with fees. Stocks may have brokerage fees while annuities could have insurance charges among other fees.

3. How do taxes impact these two options for retirement income?

The tax implications vary between stocks and annuities. With stocks, you pay taxes on gains when sold; however, if held within a retirement account like an IRA or 401(k), the gains are tax deferred until withdrawal. For annuities funded with after-tax dollars—the cost basis—you won't be taxed again on that portion at withdrawal.

4. Should I consult a financial advisor before choosing between stocks and annuity for my retirement plan?

Absolutely! It's crucial to consult a financial advisor who understands your unique needs before deciding which type of investment—stocks or any type of annuity—is best suited for your retirement goals.