What if you could wake up tomorrow and every day after that knowing your time was completely your own? At 50, with $5 million carefully invested, early retirement isn't just a distant dream – it's a real possibility that's transforming lives.

How far can 5 million dollars take you at 50?

According to the Employee Benefit Research Institute's 2024 Retirement Confidence Survey, while the median expected retirement age is 65, approximately 28% of workers are planning to retire before age 60, showing an increasing interest in early retirement options.

They're trading boardrooms for bucket lists and morning commutes for morning adventures, all while they're young enough to fully embrace their freedom. But the question remains: how far will $5 million really take you when you could have decades of retirement ahead?

Let's explore what financial independence at 50 truly means, and how to turn your $5 million nest egg into a lifestyle that doesn't just sustain you, but helps you thrive in your next chapter.

Factors that influence a comfortable retirement

Life choices play a big role in how far $5 million will go for retirement. If you dream of fancy cars, big houses, and lots of travel, your money might run out faster. But if you live simply and keep costs low, the same amount could last much longer.

The age at which you retire also makes a difference. Retiring at 50 means your savings need to stretch over more years than if you retired later. Health costs go up as we get older too.

Planning for that is key to making sure your money lasts.

Importance of lifestyle choices

Making lifestyle decisions is crucial for an enjoyable retirement. When planning for retirement with $5 million at 50, consider future expenses like healthcare premiums and inflation. Your spending habits, such as preferring first-class travel or economical trips, and dining out versus cooking at home, will significantly impact your budget.

Some aim for an extravagant lifestyle with luxury items, while others prefer fiscal tranquility. Your retirement lifestyle influences how quickly you deplete your savings. Balancing spending on hobbies and saving for unforeseen expenses is key. As medical expenses rise with age, prioritizing insurance and wellness programs can prevent high costs later.

Remember, each choice directly affects the longevity of your $5 million retirement fund.

Breaking Down the $5 Million Nest Egg

Exploring the $5 million nest egg could require a detailed breakdown of asset allocation and liquid versus non-liquid assets.

Allocation of assets (stocks, bonds, real estate, etc.)

Putting your $5 million into different types of assets is smart. Stocks, bonds, and real estate are common choices. Stocks can grow your money fast but come with high risks. Bonds are safer but offer lower returns.

Real estate can provide steady income through rent and may increase in value.

You should spread your investment across these options to balance risk and return. This way, if one area does poorly, the others might still do well. Also, consider putting some money in liquid assets like cash or savings accounts for easy access without selling investments at a bad time.

Liquid vs. Non-Liquid Assets

Balancing liquid and non-liquid assets is vital for a sustainable retirement plan. Liquid assets, such as cash, savings accounts, and certain investments, are easily accessible and can be quickly converted to cash without significant loss of value. These assets provide the flexibility needed to cover immediate living expenses and unexpected costs, ensuring financial stability in your day-to-day life.

On the other hand, non-liquid assets, including real estate, retirement accounts, and long-term investments, often require more time and effort to convert into cash.

These assets are typically geared towards long-term growth and can significantly impact your retirement portfolio's overall value. While they may not be readily available for immediate needs, they play a crucial role in building wealth over time and securing your financial future.

Expected Annual Income from $5 Million

Breaking down the anticipated yearly income from a $5 million retirement fund, based on withdrawal rates and investment returns. It will give you an idea of how to sustain your lifestyle after early retirement with this amount.

Safe withdrawal rate

When it comes to early retirement with a $5 million nest egg, grasping the safe withdrawal rate is crucial. The safe withdrawal rate varies depending on the retirement age, with different strategies needed for those retiring early versus at the standard retirement age.

While the traditional 4% rule may work for standard retirement ages, those retiring at 50 may need to consider a more conservative withdrawal rate of 2.5-3% to account for a potentially 40+ year retirement horizon.

This strategy aims to balance annual withdrawals with potential market fluctuations and inflation, providing long-term financial security.

Understanding the safe withdrawal rate is essential in planning for an early retirement with a $5 million portfolio. Withdrawing too much too soon can jeopardize long-term financial security, while withdrawing too little could impact retirees' lifestyle and ability to cover expenses.

It's significant to assess this in detail before proceeding to expected annual income and investment returns considerations.

Investment returns and risks

Now that we've made tax assumptions and examined the safe withdrawal rate, let's explore investment returns and risks. When considering securing financial independence, comprehending the potential returns on investments is crucial.

It's essential to acknowledge that while higher-risk investments may offer higher returns, they also entail a greater chance of loss. Diversifying across various asset classes like stocks, bonds, and real estate can help manage risk and potentially enhance overall return rates over time.

Moreover, actively managing your investment portfolio with consideration for market volatility and long-term growth potential supports a sustainable retirement plan.

It's wise to seek more than just short-term stability; rather than merely pursuing low-risk options, a carefully crafted approach towards long-term growth within one's wealth management strategy could lead to sustained fiscal resilience in the constantly changing world of retirement planning.

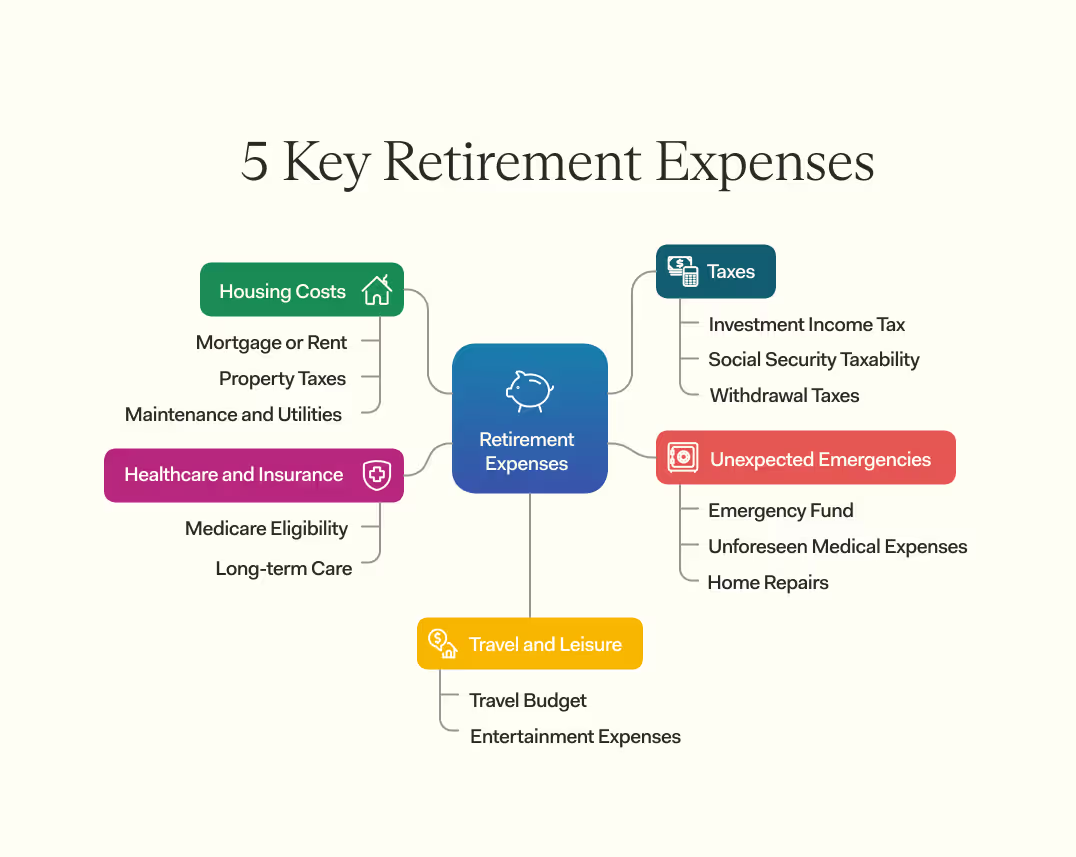

5 Key Expenses in Retirement

Here are the key retirement expenses and how they can impact your financial plan. Understanding these expenses will help you prepare your financial resources for a sustainable retirement.

1. Housing costs

Housing expenses play a significant role in retirement finances. Retirees typically allocate around 30% of their income to housing-related costs, such as mortgage or rent, property taxes, maintenance, utilities, and insurance.

Opting for a smaller residence or moving to a region with lower living expenses can assist in managing these costs. It's important to also consider potential long-term care needs and adjustments to your current home as you age.

These factors should be carefully incorporated into a sustainable retirement budget.

Retirees often overlook the lasting impact of housing expenses on their financial situation. According to the most recent Bureau of Labor Statistics Consumer Expenditure Survey data (2022), households headed by individuals aged 65-74 typically spend approximately $19,517 per year on housing costs. For those retiring at 50, these costs may be higher initially and would be subject to inflation over a longer retirement period.

Moreover, housing costs generally increase over time due to inflation and market trends. Hence, prudent financial planning that accommodates both immediate and future housing-related outlays is crucial for ensuring financial stability throughout retirement.

2. Healthcare and insurance

Healthcare costs in retirement can significantly impact your financial plan. Before Medicare eligibility at age 65, health insurance is crucial. Managing long-term care expenses also plays a vital role in securing your financial future.

The rising cost of healthcare and potential unexpected expenses for medical emergencies should be factored into your savings strategy to ensure your money lasts.

3. Travel and leisure

Transitioning from healthcare and insurance to travel and leisure, it's vital to factor in the costs associated with maintaining an active lifestyle during retirement. Retirees often allocate a significant portion of their budget towards travel, entertainment, and recreational activities.

According to the 2022 Bureau of Labor Statistics Consumer Expenditure Survey, households headed by individuals aged 65 and older spend an average of approximately $5,500 annually on entertainment and travel, though this varies significantly based on income level. It's crucial to consider these expenses when crafting your retirement plan to ensure that you can continue enjoying life without compromising your long-term planning.

Retirement doesn't mean putting an end to all fun activities. Ensuring that there is room in your budget for travel adventures or hobbies can significantly contribute to a fulfilling retirement experience, giving you the freedom and flexibility to explore new interests while remaining financially stable.

4. Taxes

When considering early retirement with $5 million, it's crucial to plan for tax implications. Income from investments like dividends and capital gains is subject to taxes, impacting the overall annual income in retirement.

Certain types of investment income, such as qualified dividends and long-term capital gains, are typically taxed at preferential rates (0%, 15%, or 20% depending on your taxable income) compared to ordinary income tax rates that apply to wages and short-term capital gains. However, other investment income, such as interest and non-qualified dividends, is taxed as ordinary income.

In addition, Social Security benefits may be taxable depending on total income. Furthermore, withdrawals from traditional retirement accounts such as 401(k)s and IRAs are also taxed at ordinary income rates upon distribution.

Careful tax planning in early retirement is essential to maximize the effective use of retirement funds while reducing your tax bill.

5. Unexpected emergencies

Managing unexpected emergencies is a crucial aspect of retirement planning. It's essential to set aside a portion of the $5 million nest egg for unforeseen circumstances such as medical emergencies, home repairs, or sudden financial needs.

Financial professionals typically recommend that early retirees maintain a larger emergency fund than traditional retirees - often 1-2 years of living expenses in cash or cash equivalents - to protect against sequence of returns risk in the crucial early years of retirement and to avoid being forced to sell investments during market downturns.

Family and Dependents Considerations

Planning for early retirement with $5 million at 50 involves considering family and dependents. The $5 million target is significantly above the average retirement savings amount of working-age residents. This includes providing for college tuition and supporting aging parents.

College tuition for children

Planning for your child's college tuition is a crucial part of retirement preparation. College expenses have been increasing at a rate nearly twice that of general inflation, posing financial challenges for many families.

According to the latest data from the College Board (2023-2024), the average total cost of attendance for an in-state student at a four-year public college is approximately $28,840 per year (including tuition, fees, room, and board), while attending a private non-profit four-year institution averages around $60,420 per year.

Considering these rising costs when planning your retirement is vital to guarantee financial peace of mind for both you and your child as you embark on this new chapter of life.

Shifting our attention from college tuition considerations, we now turn to the topic of supporting aging parents.

Supporting aging parents

As you plan for an early retirement with $5 million in the bank, attending to the potential of supporting aging parents is crucial. According to a study by AARP, 34% of caregivers are providing assistance to an aging parent.

It's essential to anticipate and budget for possible caregiving expenses as your parents age. According to Genworth's 2023 Cost of Care Survey, the national median annual cost for adult day health care in the U.S. is approximately $21,840.

Long-term care insurance premiums vary widely based on age, health, and policy features. According to the American Association for Long-Term Care Insurance (2023), a healthy 55-year-old couple might pay between $3,000 and $5,000 annually for a policy with a $165,000 benefit pool, 90-day elimination period, and 3-year benefit period.

Moving on from family considerations, let's explore the impact of inflation on your retirement plans.

The Impact of Inflation

Inflation can significantly impact retirement finances. Effective tax strategies can minimize tax liability and enhance the longevity of retirement funds. It affects the cost of living and erodes purchasing power over time.

Adjusting for future cost of living increases

To ensure your retirement savings can support you in the future, it's essential to account for possible increases in the cost of living. Inflation erodes the purchasing power of money over time.

Your $5 million nest egg may need to keep up with rising prices for housing, healthcare, and other essentials. By factoring in inflation when planning your retirement income needs, you can better prepare for potential higher living expenses.

Adjusting for future cost of living increases is crucial to maintaining your standard of living throughout retirement. Including a buffer for inflation in your financial plan helps safeguard against unexpected changes and ensures that your savings continue to provide sufficient funds as the cost of goods and services rise over time.

Passive Income Streams to Supplement Savings

Passive income streams like rental income, dividend-paying investments, and side businesses can help supplement your retirement savings. These income streams can enable you to retire comfortably without depleting your savings.

Rental income

Rental income can be a reliable source of passive income in retirement. Investing in rental properties can provide a steady cash flow, especially if the property is located in high-demand areas or tourist destinations.

Depending on the property's location and size, it's possible to generate significant monthly income from rent payments. However, managing rental properties also comes with responsibilities such as maintenance, repairs, and tenant management which should be factored into the overall financial plan for retirement.

Diversifying your retirement portfolio to include real estate investments allows you to benefit from potential appreciation of property values while earning consistent rental income.

Dividend-paying investments

Dividend-paying investments offer a consistent income stream for retirees. These investments are appealing to those looking for more than just capital growth. Dividends from stocks, bonds, or mutual funds can complement retirement savings and provide a buffer against market volatility.

Many retirees appreciate the dependable cash flow that dividends can offer, enabling them to sustain their lifestyle without frequently tapping into their principal savings.

Side businesses

Diversifying income sources is crucial in retirement. Besides dividend-paying investments, consider starting a side business to supplement your savings. Building a side business can provide additional cash flow and a sense of purpose in retirement, helping you maintain financial independence.

Many individuals have found success through small ventures like consulting, freelancing, or turning hobbies into profitable endeavors. It's an effective way to bolster your annual income and ensure long-term security beyond traditional investment strategies.

Starting a side business may require initial effort and investment but has the potential for substantial returns. This approach can be a valuable strategy to sustain your desired lifestyle without depleting your retirement savings.

Investment Strategies for Early Retirement

When planning for early retirement, it is crucial to diversify your investment portfolio to manage risks. Long-term growth should be balanced with short-term stability in your investment strategy.

How diverse is your portfolio?

Diversification is crucial to managing risk in your investment portfolio. By spreading your investments across different asset classes like stocks, bonds, and real estate, you can reduce the impact of a decline in any one investment.

It helps to balance potential returns with potential risks. Utilizing a mix of assets also provides the opportunity for growth while ensuring stability over time. This strategy aids in mitigating the impact of market volatility on your overall portfolio performance.

Long-term growth vs. short-term stability

When planning for early retirement with $5 million, it's crucial to balance long-term growth and short-term stability.

Long-term growth typically involves investing in stocks, which have historically provided higher returns but come with more volatility. Conversely, short-term stability focuses on preserving capital through investments like bonds or cash equivalents, which may offer lower returns.

A balanced approach is key to sustaining your retirement fund while allowing it to grow. A diversified portfolio with both growth-oriented and stable assets can help achieve this balance.

Real Estate as a Retirement Strategy

Real estate can be a smart retirement strategy. Downsizing your home and investing in rental properties are worth considering for additional income and asset growth.

Downsizing your home

Reducing the size of your home can release substantial funds for retirement. Selling a larger home and buying a smaller one could decrease your mortgage or pay it off completely. For example, if you sell a $400,000 home and purchase a $200,000 one, you might be able to add an additional $200,000 to your retirement savings.

Moreover, downsizing can lower ongoing expenses. A smaller property usually results in reduced utility bills, property taxes, and maintenance costs. This can establish a more sustainable living situation in retirement and release additional funds for other necessary expenses like healthcare or leisure activities.

Investing in rental properties

Investing in rental properties can be a smart way to build passive income during retirement. Rental income from properties can supplement your savings, offering consistency and stability.

With careful selection of properties and good management, you can enjoy steady cash flow and potential for property appreciation over time. Rental properties can be a reliable source of income that complements other investment assets, helping to sustain your lifestyle throughout retirement.

Moreover, real estate has historically proven to be a solid long-term investment with the potential for strong returns.

In reality, data shows that rental properties have provided consistent returns over the years. According to recent statistics, the average annual return on investment for housing rentals stands at around 10%.

Budgeting for a Sustainable Retirement

Budgeting for a sustainable retirement involves distinguishing essential from non-essential expenses and tracking spending habits to ensure long-term financial stability. It's crucial to understand future healthcare costs and manage them effectively, especially before becoming eligible for Medicare.

Essential vs. non-essential expenses

Essential expenses are the fundamental costs you need to cover for basic living, such as housing, food, and healthcare. On the other hand, non-essential expenses include things like leisure activities and luxury items that enhance your lifestyle but aren't necessary for survival.

Balancing essential and non-essential expenses is crucial in retirement planning to ensure financial stability while also enjoying a more comfortable retirement lifestyle.

It's important to prioritize essential expenses when creating a retirement budget because they form the foundation of your financial security. Non-essential expenses can be adjusted based on available funds after covering essential costs.

Tracking spending habits

It's advisable for retirees to carefully track their spending habits through detailed record-keeping and regular reviews. This approach ensures that they maintain control over their finances, allowing them to make informed decisions about where and how their money is allocated.

Healthcare Costs in Early Retirement

Looking at healthcare costs in early retirement, it's vital to consider health insurance options before Medicare eligibility and managing long-term care expenses effectively. These factors are crucial for ensuring financial stability during retirement.

Health insurance options before Medicare eligibility

Before turning 65 and becoming eligible for Medicare, those who retire early have various health insurance options to consider. One option is to prolong coverage through an employer's plan using COBRA for up to 18 months after leaving employment.

Another choice is purchasing a policy on the Health Insurance Marketplace within 60 days of losing employer-based coverage. In addition, some states offer extended Medicaid coverage for low-income individuals during transitional periods.

Retirees can also explore short-term health insurance plans, which provide temporary coverage until more permanent solutions are available. It's crucial to carefully compare premiums, deductibles, and out-of-pocket costs when evaluating these options before transitioning to Medicare at age 65.

Managing long-term care expenses

Managing long-term care expenses is a crucial aspect of retirement planning. According to Fidelity's 2023 Retiree Health Care Cost Estimate, a 65-year-old couple retiring in 2023 can expect to spend approximately $315,000 in after-tax dollars on healthcare expenses throughout retirement, including Medicare premiums, deductibles, copayments, and out-of-pocket costs.

Long-term care insurance can help cover expenses if assistance with daily living activities becomes necessary. It's important to consider this when creating a financial plan.

Long-term care costs vary based on location and the level of care required. According to Genworth's 2023 Cost of Care Survey, the national median monthly cost of a private room in a nursing home has increased to approximately $9,584.

Considering these figures is essential to ensure you can live comfortably as you age.

Risks of Retiring at 50

Retiring at 50 comes with the risk of outliving your savings as you may need financial support for a longer period. Market volatility can also impact your retirement fund, affecting its sustainability.

Longevity risk

Longevity risk refers to the possibility of outliving your retirement savings. With life expectancy on the rise, this risk is becoming more pertinent. It's crucial to plan for a retirement that could last several decades after leaving the workforce.

This involves carefully managing and allocating assets to ensure that you have enough income to sustain your desired lifestyle well into old age. It's important to consider potential medical expenses and long-term care, as healthcare costs tend to increase as individuals grow older, impacting their financial security.

Retirees face the challenge of stretching their savings over an extended period due to increasing lifespans. Inflation can also erode purchasing power over time, making it necessary to consider these factors when planning for a secure financial future in retirement - especially with $5 million at stake.

Market volatility

Market volatility, the fluctuation in asset prices, especially stocks, can significantly impact retirement savings. This could jeopardize early retirement plans and financial security.

For example, during the 2008 financial crisis, stock markets experienced a severe downturn with the S&P 500 declining by approximately 57% from its October 2007 peak to its March 2009 trough. Such events can result in significant portfolio losses for individuals relying on their investments for retirement income.

Consequently, it's crucial to diversify investment portfolios to mitigate the impact of market volatility on retirement savings. Research shows that diversification helps to spread risk across different assets and may shield retirees from large losses due to sharp declines in any one investment.

In addition to this historical evidence of market impacts on retiree finances, ongoing factors such as geopolitical tensions or interest rate changes can amplify market fluctuations.

Can You Return to Work if Needed?

If retirement funds run low, consider part-time work options or consulting/freelancing opportunities.

Consider exploring alternative work arrangements and flexible job opportunities for supplemental income.

Part-time work options

Consider the option of part-time work to supplement your retirement income. Many retirees find part-time employment as a way to stay engaged and add extra cash flow. It can offer the flexibility to balance leisure time with earning an additional income, helping you maintain financial stability.

Consulting or freelancing opportunities

As you contemplate early retirement, it's crucial to consider exploring consulting or freelancing opportunities as a potential source of income. Many retirees find that utilizing their expertise on a part-time basis can supplement their savings and provide financial stability.

With the rise of remote work and gig economy platforms, there are abundant opportunities for professionals to participate in consulting projects or freelance assignments within their industry.

This not only adds to financial security but also allows individuals to stay engaged in meaningful work while enjoying the flexibility that comes with retirement.

According to recent data, an increasing number of retirees are choosing consulting or freelancing roles post-retirement, contributing to their annual income and overall financial well-being.

As you plan for early retirement with $5 million in savings, exploring these flexible work options can help ensure a sustainable and fulfilling retirement lifestyle.

Recommendations for a Successful $5 Million Retirement

Plan with a financial advisor to ensure a sustainable and secure retirement now. Regularly review and adjust your financial plan for long-term security.

Work with a financial advisor

For an early retirement at 50 with $5 million, teaming up with a financial advisor is essential. They can help guide you through the intricacies and customize a plan for your financial milestones using investment strategies and wealth management expertise.

An advisor will carefully review and adjust your plan to support long-term financial security, considering the high cost of living and constantly evolving retirement goals, guiding you in accessing passive income streams such as rental properties or dividend-paying investments for sustainable retirement income.

Moreover, they aid in managing risks by diversifying the portfolio against market volatility, providing personalized recommendations on budgeting for essential vs non-essential expenses.

A Farther financial advisor brings specialized expertise in early retirement planning, creating tailored strategies that align with your unique vision for financial independence.

Don't leave your retirement dreams to chance—talk to an advisor today to transform your $5 million portfolio into decades of financial freedom.

Regularly review and adjust your retirement planning

To maintain financial stability throughout retirement, it's crucial to regularly review and adjust your financial plan. This involves tracking your investment returns, revisiting your asset allocation strategy, and making necessary adjustments as per changing market conditions.

Regular reviews help ensure that your retirement income remains aligned with your expenses, mitigating the impact of unforeseen fluctuations in the market.

A dynamic approach to managing your financial plan also includes staying updated on tax laws and regulations, potential changes in healthcare costs, as well as making modifications to accommodate evolving lifestyle choices and family responsibilities.

Conclusion

Is retiring at 50 with $5 million truly achievable? Absolutely—but your success depends on strategic planning and thoughtful execution. This significant nest egg can provide decades of financial freedom when properly managed against inflation, healthcare expenses, and life's inevitable surprises.

Smart diversification across multiple investment classes creates both stability and growth potential, while strategic development of passive income streams provides additional financial security beyond traditional portfolio withdrawals.

With careful planning and regular reassessment of your financial strategy, your $5 million can support the retirement lifestyle you've worked so hard to achieve, allowing you to enjoy life's opportunities while you're young enough to fully embrace them.

FAQs

1. Is $5 million enough to retire comfortably at age 50?

Yes, retiring at 50 with a net worth of $5 million is possible. It depends on your lifestyle choices and spending habits after retirement.

2. What factors should I consider for early retirement?

Consider your annual expenses, healthcare costs, and investment returns. These factors will impact how long your money lasts.

3. How can I manage my finances after retiring at 50?

Create a budget to track income and expenses. Invest wisely to grow your savings while ensuring you have enough for daily needs.

4. Is it wise to rely solely on $5 million for retirement?

Relying only on $5 million may not be wise if you do not plan carefully. Diversifying investments and having additional income sources can provide more security in retirement.