Tax time can seem complicated. Many people look for ways to reduce what they owe or increase their refund. A key tool for this is the Earned Income Tax Credit (EITC). It benefits workers with low to moderate income by providing a significant tax break.

In 2020, around 25 million taxpayers received over $62 billion from EITC. This guide will simplify EITC, explaining eligibility, calculation, and how to claim it. This information could lead to extra money for eligible individuals.

Key Takeaways

- The Earned Income Tax Credit (EITC) is for low to moderate income workers. It can lower taxes and give bigger refunds.

- You need earned income from a job or self-employment to qualify. Filing status, income level, and having children affect eligibility.

- In 2025, singles without qualifying children can claim the EITC if they earn less than $19,104; this income limit increases with the number of qualifying children.

- To claim EITC, provide Social Security numbers and proof of income. File your tax return by the deadline using correct forms.

- Common reasons for EITC denial include missing documents and filing errors. Check everything carefully before submitting.

What is the Earned Income Tax Credit (EITC)?

This credit helps working individuals with low to moderate income. The IRS states this credit can reduce the tax you owe and might result in a refund if your earnings are below a certain threshold.

According to the National Tax Journal, the EITC aims to assist those with the lowest incomes.

To qualify for this credit, you need to earn money from employment or from running a business or farm. Your filing status, whether you have children, and your income level also play crucial roles in eligibility for EITC.

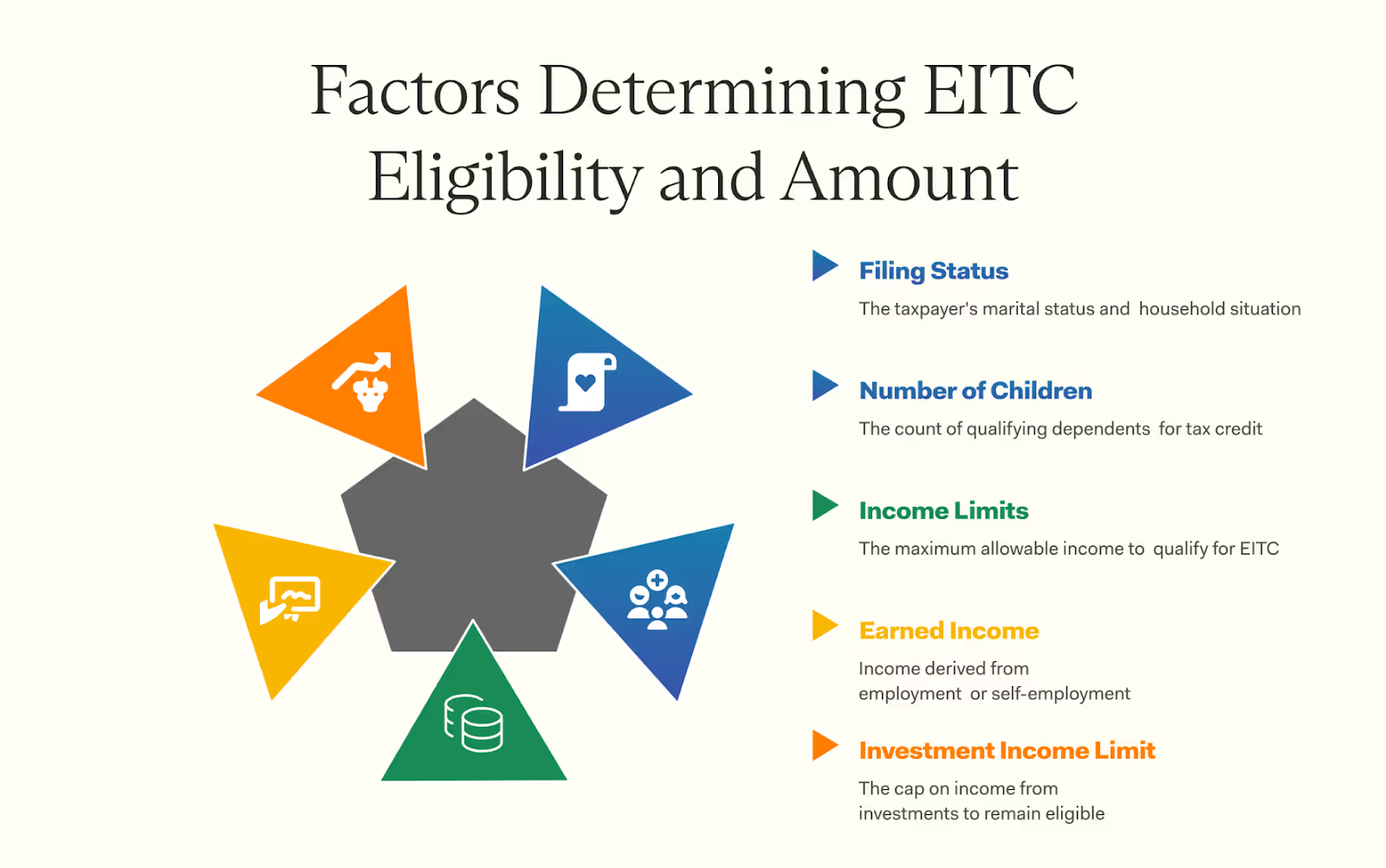

Who Qualifies for the EITC?

To get the Earned Income Tax Credit (EITC), your income, family size, and filing status must fit specific rules. This includes if you have children or other dependents and how much you earn.

Basic eligibility rules

To qualify for the Earned Income Tax Credit (EITC), you must meet some basic rules. First, you need earned income from a job or self-employment. Your income should fall below specific limits set for each tax year.

These limits change based on how many qualifying children you have and your filing status.

You cannot claim EITC if you file as "married but filing separately." If you're single or married with a joint return, you'll meet more eligibility options. You also can't have investment income over a certain amount—this is usually around $10,000.

Meeting these basic requirements can help you get this valuable income tax credit in your federal taxes!

Special qualifying rules

Special qualifying rules help some people get the Earned Income Tax Credit (EITC). If you have a child who is a foster child, you can claim them. That means they lived with you for more than half the year.

Your household must also meet income limits to qualify.

Single filers and married couples both face different maximum credit amounts based on their earnings and family size. For families with three or more children, the EITC can provide a bigger benefit.

Young adults who work but don't have kids may still qualify under certain conditions too, like age and earned income levels.

Filing status requirements

Filing status matters for the Earned Income Tax Credit (EITC). You can file as single, married filing jointly, married filing separately, or head of household. Your status must match your tax return and affect how much you can claim.

If you're married but file separately, you can't get the EITC. The Internal Revenue Service has strict rules here. Be aware that qualifying children also play a role in deciding your credit amount based on your filing status.

Ensure all details are accurate to avoid problems with your claim later on.

Claiming without a qualifying child

You can still claim the Earned Income Tax Credit (EITC) even if you don't have children. To do this, you must meet certain rules.

First, your earned income needs to be less than $18,591 for individuals and $25,511 for married couples in 2024. Age matters too; you must be at least 25 years old but under 65 during the tax year.

Your investment income also can't exceed $11,600 in 2024. If you meet these guidelines, you may be eligible for an EITC amount up to $632 in 2024, which is smaller compared to those with qualifying children but still a helpful income credit!

How to Calculate Your EITC

To find your EITC, check your earned income. It varies based on how many qualifying children you have and meets certain limits.

Earned income limits (2024, filing in 2025)

Understanding the earned income limits is key to figuring out your eligibility for the Earned Income Tax Credit (EITC). The limits vary based on your filing status and the number of qualifying children you claim.

If you're single, head of household, or widowed, here are the income limits to qualify:

- With no qualifying children, your income must be under $18,591.

- With one child, the limit rises to $49,084.

- With two children, it's $55,768.

- With three or more children, your income must be less than $59,899.

If you're married filing jointly, the thresholds are a bit higher:

- With no children, your income must be under $25,511.

- With one child, the limit increases to $56,004.

- With two children, it becomes $62,688.

- With three or more, you must earn less than $66,819.

These limits are important because they determine whether you’re eligible to claim the EITC. For example, a single parent with two kids must earn less than $55,768 to qualify. Always check the current year’s guidelines, as these figures can change.

Number of qualifying children

The more qualifying children you have, the higher your EITC can be.

- With no children, the maximum credit is $632.

- With one child, it jumps to $4,213.

- With two children, it increases to $6,960.

- With three or more children, the maximum credit tops out at $7,830.

The income limits also scale with the number of children. For example:

- A single filer with three children must earn under $59,899.

- A married couple filing jointly with the same number of kids must earn less than $66,819.

These figures are crucial when estimating your potential EITC benefits and ensuring you're not over the income threshold.

How to Claim the EITC

To claim the EITC, gather your documents. These include proof of income and any qualifying children you have. Then, file your tax return—this can be done online or on paper.

Required documentation

Claiming the Earned Income Tax Credit (EITC) needs specific papers. These documents help verify your income and eligibility.

- A valid Social Security number for you, your spouse, and any qualifying children is necessary.

- Proof of earned income must be included. This can come from W-2 forms or 1099s from your employer.

- If you have other sources of income, provide proof for those too. This could include self-employment earnings.

- Document any qualifying children. This includes their names, ages, and Social Security numbers.

- You may need to show your filing status. If you're married, both partners might need to sign the tax return.

- If claiming a foster child as a qualifying child, include legal documentation showing the arrangement.

- Keep copies of all documents for your records. This helps if you face questions later.

Having this required documentation ready can make filing smoother. It can also reduce delays in receiving tax refunds.

Filing your tax return

Filing your tax return is simple, but you need to do it right. Here's how to get started.

- Gather all necessary documents. This includes W-2 forms and any other income statements. You'll also need proof of your Earned Income Tax Credit (EITC) eligibility, such as information on qualifying children or foster children.

- Choose how to file. You can go with paper filing or use tax software. Many people prefer e-filing because it's faster and helps reduce mistakes.

- Fill out the correct forms. Use Form 1040 for most taxpayers. Make sure to include the EITC on your form if you qualify.

- Check your calculations. Errors can lead to delays or even denials of your EITC claim. Double-check everything before submitting.

- Submit your tax return by the deadline. It's usually April 15 each year unless it falls on a weekend or holiday—keep an eye out for changes!

Properly filing your return can help secure benefits like refunds and lower taxes owed, which many find helpful.

Benefits of the EITC

The EITC helps lower your tax bill. It can also boost your refund, putting more cash in your pocket.

Reducing tax liability

This credit helps lower your tax bill. It puts money back in your pocket when you file your taxes. If you qualify, the EITC can reduce what you owe to the federal government.

For many, this means a bigger refund.

For the 2024 tax year, families can receive payments based on their income and number of children, with the maximum credit for taxpayers with three or more qualifying children being $7,830. The EITC phases help decide how much credit you get. This is especially helpful for low- to moderate-income earners.

With less tax liability, it can make a big difference in financial stability for those who need it most.

Increasing tax refunds

The EITC can boost your tax refund. For many, it means extra money in their pockets. The credit helps low to moderate-income workers pay less tax. It may even turn a tax bill into a refund.

If you qualify based on your earned income and the number of qualifying children, you can see significant savings. Even if you have no kids, some people still qualify for this income tax credit EITC.

That means more cash back when you file your taxes. However, ensure all required documentation is in order to avoid any issues with your claim.

Common Reasons for EITC Claim Denials

Claiming the EITC can be tricky. Many people get denied due to missing documents or mistakes on their tax forms.

Missing documentation

Missing documentation can lead to EITC claim denials. If you don't provide the right papers, your claim might be rejected. Common missing items include proof of income and accurate Social Security numbers for every member of the household.

Without these documents, the IRS cannot verify your eligibility.

Many people miss out on credits because they don't keep good records. It's key to file with accurate information and all necessary forms. This helps avoid errors that could result in denial.

Now let's look at filing errors next!

Filing errors

Filing errors can lead to denied Earned Income Tax Credit (EITC) claims. Common mistakes include incorrect Social Security numbers and math errors on the tax forms. If your information does not match what the IRS has, it raises a red flag.

Be sure to check all requirements carefully before submitting your return. Errors can delay refunds or cause you to miss out on valuable credits like the child tax credit.

Proper preparation helps avoid pitfalls when claiming EITC benefits.

Conclusion

The Earned Income Tax Credit offers significant financial relief to many working families. It can reduce your tax burden and potentially increase your refund. Eligibility depends on your income, family composition, and filing status. Before applying, ensure you've gathered all necessary documentation.

Claims are often rejected due to incomplete paperwork or errors. Review your tax return carefully to avoid mistakes. Understanding how the EITC works can substantially improve your financial situation.

Consider whether this credit might benefit you or someone you know. There are many resources available if you want to learn more. Taking the time to explore the EITC could make a meaningful difference in your financial wellbeing!

FAQs

1. What is the Earned Income Tax Credit (EITC)?

The EITC, or earned income credit, is a refundable tax credit designed to benefit low- to moderate-income working individuals and families, helping to reduce poverty and encourage employment.

2. Who can qualify for the EITC?

To qualify for this credit, you must meet eligibility criteria set by the Internal Revenue Service (IRS), which includes having earned income within certain limits, specific filing statuses, and the presence of qualifying children.

3. How does the amount of EITC get determined?

The amount of EITC you receive depends on your earned income for the current year, your filing status, and the number of qualifying children you have.

4. Has there been any significant change in EITC recently?

Yes, though the EITC had been temporarily expanded due to the COVID-19 pandemic, those expansions expired as of 2025, and the credit has now reverted to its pre-pandemic rules and amounts.

5. Where can I find more information about EITC?

For accurate and updated information regarding all aspects of the Earned Income Tax Credit, including eligibility rules and application procedures, consult resources provided directly by the Internal Revenue Service (IRS).