Worried about inflation eating away your retirement savings? As prices rise, your carefully saved dollars lose purchasing power, threatening your future financial security.

Strategic planning can shield your retirement from inflation's impact. This guide reveals practical ways to protect your savings, including diversification strategies, inflation-resistant investments, and smarter withdrawal approaches to maintain your lifestyle regardless of economic conditions.

Key Takeaways

- Diversify your investment portfolio with stocks, bonds, commodities, and real estate to guard against inflation.

- Consider using TIPS and other inflation-protected securities for stable income that keeps up with rising costs.

- Keep saving money in retirement accounts like IRAs or 401(k)s and take advantage of tax breaks to grow savings faster.

- Delay Social Security payments if possible to increase monthly benefits and better handle inflation's impact on income.

- Monitor spending habits closely, reduce unnecessary expenses, and regularly check your financial plan to adjust for inflation.

Understand Inflation's Impact on Retirement Savings

The rising cost of everyday items and health care can lower the value of retirement savings because money won't buy as much. For example, with a 3% inflation rate annually, an item costing $100 today will be about $134 in 10 years.

This situation is tough for retirees relying on fixed income from social security benefits or retirement accounts.

Protecting savings against high inflation is crucial for financial security in retirement. Smart planning and choosing investments that grow faster than inflation are important steps.

Strategies include focusing on investments known to offer protection against rising prices to safeguard your nest egg from losing its purchasing power due to inflation.

Strategies to Protect Retirement Savings from Inflation

To protect your retirement savings from inflation, diversify your investments and favor those that offer inflation protection. This strategy helps shield against the financial risks of rising prices.

Diversify your investment portfolio

A well-diversified investment portfolio is key to protecting your retirement savings from inflation. A mix of asset classes, like stocks and bonds, helps spread the risk. If one area weakens, others may hold strong.

Inflation affects everything; higher prices can eat away at your savings if you're not careful.

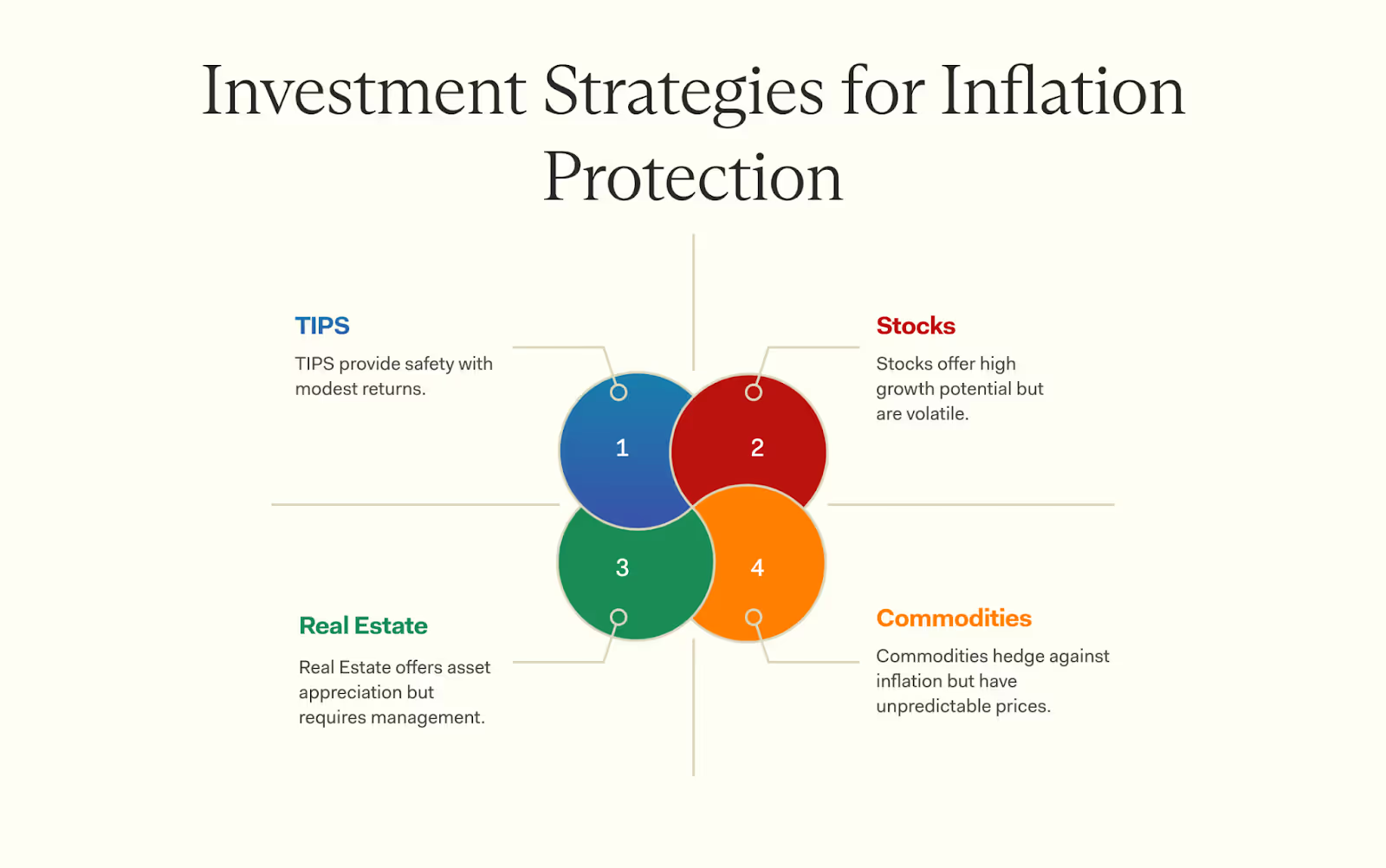

Consider adding commodities and real estate to your investments. These can often outpace inflation when prices rise. Treasury Inflation-Protected Securities (TIPS) are also a good choice as they adjust with inflation rates.

Build a balanced allocation that suits your needs and goals. This gives you more financial stability in tough times.

Invest in inflation-protected securities (TIPS)

TIPS can be a smart choice for your retirement savings. These bonds adjust their value based on inflation rates. As prices rise, the principal amount of TIPS increases.

This means you can keep up with inflation's impact on retirement income.

TIPS offer a fixed interest rate along with protection against rising costs. They help combat inflation while providing guaranteed income over time. Many investors use TIPS to maintain purchasing power as commodity prices increase and interest rates fluctuate.

Include commodities and real estate investments

Commodities and real estate can help shield your retirement savings from inflation. Commodities like gold, oil, or agricultural products often rise in price when inflation increases.

They can provide a hedge against inflation's impact on retirement.

Real estate is another solid option. Property values tend to grow over time. Rental income can also offer steady cash flow during periods of high inflation. A mix of both assets in your investment plan may boost growth potential and protect your retirement security as prices climb.

Maintain a balanced allocation of stocks and bonds

Investing in both stocks and bonds helps reduce risk. Stocks can grow your money, while bonds provide steady income. A mix of these assets can protect you from inflation risk. Maintaining a balanced allocation is key for retirement planning.

Many experts recommend an asset allocation based on your age and risk tolerance. Younger investors might choose more stocks since they have time to recover from market dips. As you approach retirement age, shifting to bonds can help maintain stability during rising interest rates or declining markets.

This balance promotes long-term growth and protects against economic conditions that may affect your savings.

Optimize Your Budget during Inflation

Keep an eye on your spending. Adjust your habits to save more during inflation.

Track and adjust spending habits

Monitoring your expenses is essential. Write down everything you buy for a month. Look at your habits closely. Identify what is necessary and what isn't. This can help you cut back on extra costs.

Adjust how much you spend each month based on inflation rises. Prices keep going up, which means money doesn't stretch as far. Stay aware of your situation, so you're prepared to make changes when needed.

It's vital to control expenses now, especially since most retirees rely on their savings during retirement years.

Reduce unnecessary expenses

Cutting down on extra costs helps your savings grow. Focus on what you really need. Review subscriptions, dining out, and shopping habits. Small changes can add up fast. For example, cancel unused services or switch to cheaper options.

Use this new budget to boost your retirement accounts. Every dollar counts against inflation's impact on retirement savings.

Maintain Consistent Contributions

Consistency in saving money, even when prices rise, is crucial. Use retirement accounts wisely to boost your savings and grow your nest egg.

Continue saving during periods of high inflation

Saving during times of high inflation is crucial. Inflation can eat away at your retirement savings. Prices rise, making it hard to maintain your lifestyle later on. Don't stop contributing to your retirement account because of rising costs.

Keep putting aside money regularly, even if it's a smaller amount.

Consider using tax-advantaged accounts like IRAs or 401(k)s to save more efficiently. For instance, in 2026 the 401(k) contribution limit is $24,500, whereas the IRA limit is $7,500. Additionally, catch-up contributions allow those aged 50 and over to contribute extra funds — $8,000 for 401(k)s and $1,100 for IRAs.

The federal reserve might raise interest rates in response to inflation, which can impact your investments too. However, as of March 2025, rates are maintained in the range of 4.25%-4.50% due to economic uncertainties. It's important to be aware of these current policies while also considering possible future changes when planning long-term investments.

Take advantage of retirement account benefits

Use your retirement accounts wisely. They often offer tax breaks that can help your savings grow faster. For example, you might not pay taxes on the money you put in until later. This means more of your money stays invested.

Contributing regularly to these accounts is key. Even small amounts add up over time. You can also benefit from employer matches if available—this free money is a no-brainer for boosting savings.

Don't miss out on any opportunities that help protect against inflation and keep your retirement plans strong!

Delay Social Security Payments (if possible)

Waiting to claim Social Security can substantially increase your benefits. For example, if you delay until age 70, you could receive up to 76% more than at age 62, if your full retirement age (FRA) is 66. Those with an FRA of 67 might see an increase of about 77%. It's important to note that these increases depend on your FRA.

Many experts suggest this strategy if possible. You may not need to tap into Social Security right away, especially during high inflation periods. Delaying allows more time for other assets to grow and can lead to a larger payout later.

This approach also provides a cushion against rising healthcare costs and taxes as expenses increase over time.

Plan for Rising Healthcare Costs

Healthcare expenses continue to increase at a rate that often outpaces general inflation. They can take a big bite out of retirement savings. It's wise to plan for these expenses ahead of time. A key factor is knowing how much you might need in the future.

Medicare helps, but it may not cover everything. Many retirees face high out-of-pocket costs.

One way to prepare is by opening a Health Savings Account (HSA), though you must be enrolled in a High-Deductible Health Plan (HDHP) to qualify. This account allows you to save money tax-free for medical expenses. However, it's important to remember that while contributions to an HSA are tax-deductible and withdrawals for qualified medical expenses are tax-free, withdrawals for non-qualified expenses are subject to income tax and, if undertaken before age 65, an additional 20% penalty.

Investing in long-term care insurance can also be smart, but it's essential to be aware that premiums can be substantial, not all applicants may qualify due to health conditions, and the benefits can vary significantly between policies. Extensive research and comparison are necessary before making a purchase.

Keeping track of your healthcare spending habits now will help you budget better down the road. Start planning today with a broader strategy that includes various financial tools to manage healthcare expenses effectively, although these measures may not fully protect against inflation or all unexpected healthcare costs.

Manage Taxes and Fees

Effective tax and fee management is essential. Choose investments that save you money on taxes. Keep an eye on any fees that might eat into your savings. Doing this can help you keep more of what you earn.

Choose tax-efficient investments

Tax-efficient investments can help you retain more of your money. These types of investments reduce the amount you pay in taxes on gains. Choosing options like municipal bonds or index funds can save you cash.

They often come with lower fees and fewer taxable events.

Additionally, long-term capital gains are taxed at lower rates than ordinary income. For 2025, single filers with taxable income up to $48,350 are taxed at 0%, those with income between $48,351 and $533,400 at 15%, and income over $533,400 at 20%. Holding onto your investments for over a year may benefit you here. Working with a tax professional is wise too; they can provide personalized advice that fits your situation well.

Even small choices about investment types matter when planning for retirement savings against inflation!

Minimize investment-related fees

Investment-related fees can diminish your returns. They often reduce the overall growth of your assets. Seek low-fee options when selecting investments. High fees don't always indicate better performance.

Choose tax-efficient investments to help increase savings too. Avoid funds with high transaction costs or management fees. Every dollar saved on fees helps safeguard your retirement from inflation over time.

Ensure to review those costs regularly, as they can accumulate quickly.

Reassess Your Financial Plan Regularly

Regular review of your financial plan is essential. Inflation affects retirement savings over time. Regular check-ups can help spot changes in spending or investment needs. Review your investments often, especially as interest rates rise.

Adjust your budget if inflation takes a toll on your savings. Focus on tax-efficient investments to keep more of what you earn. A good financial plan helps assets grow and protects against long-term inflation impacts.

Protect Your Retirement Savings From Inflation

Inflation can erode your hard-earned retirement savings if you don't plan ahead. Strategies like investing in inflation-protected assets, adjusting your withdrawal rate, and diversifying your portfolio can help safeguard your wealth.

Want a tailored strategy to fight inflation? Talk to a Farther financial advisor and secure your financial future!