Are annuities the right retirement solution? This financial product promises steady income from insurance companies, offering potential security for your post-working years.

This guide examines the three primary types—fixed, variable, and indexed annuities—and their key features including guaranteed income streams and tax-deferred growth opportunities.

We'll break down what an annuity is and its pros and cons to help determine if they belong in your retirement strategy.

Key Takeaways

- Annuities provide a steady income in retirement and grow tax-deferred, but they come with high fees and can be hard to get money from early.

- There are different types of annuities—fixed, variable, indexed, immediate, and deferred—with varying levels of risk and potential growth.

- Before buying an annuity, consider your financial goals, how much risk you want to take on, the fees involved, and make sure you have enough liquid savings.

- Alternatives like bonds, CDs, and mutual funds offer various benefits that might better fit your retirement plan without locking up your money.

- Always read the contract terms carefully for any annuity or investment product to understand all costs and conditions before making a decision.

What Is an Annuity?

An annuity is a financial product that you buy to get a steady income during retirement. You pay an insurance company money now—either as a lump sum or through payments. In return, the company promises to pay you back with interest over time.

This can start immediately or later on, depending on what kind of annuity you choose.

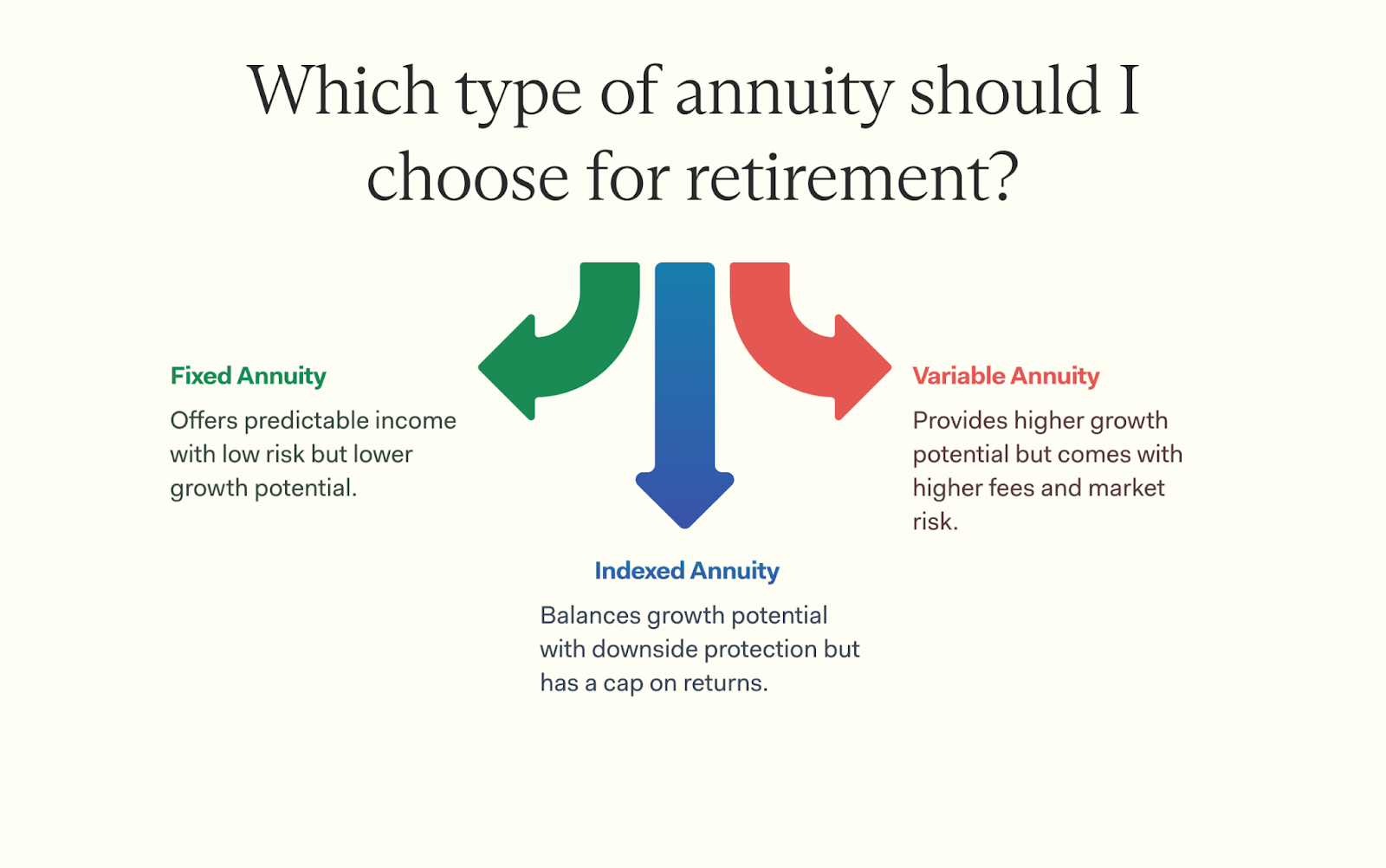

There are several types of annuities—fixed, variable, and indexed. Fixed annuities offer a guaranteed income stream based on a fixed interest rate. Variable annuities let your earnings vary with the stock market.

Indexed annuities combine features of both, linking earnings to a stock market index but also guaranteeing a minimum return. Immediate versus deferred decisions depend on when you want to start receiving payments.

Types of Annuities

Annuities come in several flavors, each with its own set of rules and benefits. From the steady pace of fixed annuities to the more adventurous variable options, there's a type designed to match your financial appetite.

Fixed Annuities

Fixed annuities provide a steady income during retirement. They guarantee a fixed payout over time. This means you get stable payments, often monthly, for the rest of your life or a set period.

You can also grow your money on a tax-deferred basis until withdrawal. Most fixed annuities offer security and less risk than other investments.

Fees can be high with these contracts, but they usually come with low market risk. You won't have to worry about losing money due to market downturns. Just ensure to check the specific terms of each contract before buying one.

Fixed annuities work best for those wanting guaranteed income.

Variable Annuities

Unlike their fixed counterparts, variable annuities allow your investment to grow based on market performance. You choose different options to invest your money, like stock and bond funds. This gives you the chance for higher returns.

Variable annuities come with risk. Your income payments may go up or down based on how well your investments perform. They also have high fees and surrender charges if you withdraw money early.

Yet, they allow tax-deferred growth until you pay taxes on withdrawals. Ensure you're aware of the risks before buying an annuity contract like this—it's vital to consider whether they fit your financial goals and risk tolerance.

Indexed Annuities

Indexed annuities link your returns to a stock market index, like the S&P 500. They offer a balance between safety and growth. These products provide tax-deferred growth on earnings, meaning you won't pay taxes until you withdraw money.

You can earn more when the index does well but still have a minimum return guarantee if it doesn't. This feature helps protect against market downturns while giving potential for higher gains compared to fixed annuities.

Fees vary widely in most annuity contracts, so check those before buying.

Immediate vs. Deferred Annuities

Immediate and deferred annuities serve different needs. An immediate annuity starts paying you right away. It provides quick, steady income for your retirement. You usually buy it with a lump sum.

A deferred annuity works differently. You put in money now but receive payments later. This type lets your funds grow tax-deferred until you start taking withdrawals. It can help build more retirement income over time since compound interest boosts your savings.

However, there might be fees involved when cashing out early. Each choice has its benefits depending on how you want to manage your money in retirement.

Key Benefits of Buying an Annuity

An annuity can give you a steady stream of income in retirement. It also helps your money grow tax-deferred, which means you won't pay taxes on it right away.

Guaranteed Income Stream

A guaranteed income stream is one of the main benefits of buying an annuity. This means you can receive steady payments throughout your retirement. Annuity payments begin either right away or after a set time, depending on the type of annuity you choose. Fixed annuities guarantee these payments for a specific period or even for life.

These regular payments provide financial security during retirement. You don't have to worry about how long your savings will last. With tax-deferred growth, your money can grow without immediate taxes eating into it.

This feature helps in generating income that supports your needs over time, making it easier to manage monthly retirement income effectively.

Tax-Deferred Growth

Tax-deferred growth helps your money grow faster. With annuities, you don't pay taxes on earnings until you withdraw them. This means your retirement funds can compound over time without the tax bite hanging around.

This feature can be great for long-term savings. You only face ordinary income tax when you take out money from the annuity. If you decide to hold onto your investment longer, it may generate more income down the line while enjoying tax-advantaged status.

Inflation Protection (for Specific Types)

Annuities can offer inflation protection with specific types. Indexed annuities adjust your payments based on a market index. This means as prices rise, so could your income. It helps keep pace with the cost of living.

Fixed annuities usually provide stable payments, but they may not guard against inflation. Some companies add features to help protect against rising costs. Always check how these options work before buying an annuity for retirement.

Be aware of any extra fees tied to these benefits too—you want to make sure it fits your financial goals.

Potential Drawbacks of Annuities

Annuities can have high fees and commissions that eat into your returns. You might also find it hard to access your money, as surrender fees can apply if you withdraw funds early.

High Fees and Commissions

High fees and commissions can be a big downside of buying an annuity. Many contracts come with high costs that eat into your returns. Fees may include administrative fees, surrender charges, and commissions for insurance agents. These costs can reduce the amount you earn from your investment.

Some annuities have ongoing management charges too. Variable annuities usually have higher fees compared to fixed options. This can make it hard for your money to grow on a tax-deferred basis as planned.

Before you buy, check all the fee details closely to avoid losing money down the road.

Lack of Liquidity

An annuity has a big drawback: lack of liquidity. This means your money can get stuck in the annuity for a long time. If you need cash quickly, that could be a problem. With an annuity, you may face penalties if you want to take out money early.

Many people use these products to generate income in retirement, but tying up funds can affect your financial planning. You might owe taxes on withdrawals too, which adds another layer of complexity and cost.

Annuity fees can make it harder to access your savings when needed most.

Tax Implications at Withdrawal

Withdrawals from annuities can have tax implications. Money you take out is taxed as income. This means if you withdraw funds, the IRS may take a cut. Tax deferred growth applies while your money sits in the annuity but not when it's withdrawn.

If you've contributed after-tax dollars, only earnings are taxed. If contributions were pre-tax, expect taxes on the full withdrawal amount. Understanding these rules helps avoid surprises during retirement withdrawals and ensures better financial planning for your future needs.

Always check with a financial advisor to understand your specific situation well.

Market Risk (for Variable Annuities)

Variable annuities come with market risk. Your money can go up or down based on market performance. If stocks and bonds do well, your investment grows. But if the markets fall, you could lose money. This risk makes variable annuities different from fixed ones that guarantee returns.

Investors must think about their comfort level with risks before buying a variable annuity. Some people prefer safety over potential gains. Others may want to take risks for higher rewards.

It's crucial to understand how these investments fit into your financial goals and plans for retirement contributions, especially given that you might also rely on social security in the future.

Key Considerations Before Buying an Annuity

Before purchasing an annuity, you'll need to carefully evaluate your financial situation. Think about your financial goals and risk tolerance—these factors will help guide your decision.

Assessing Your Financial Goals

Start by thinking about your financial goals. What do you want for retirement? Do you need a steady income? An annuity could help with that. Consider if you'll rely on it for daily expenses or just as an extra source of funds.

Next, know how much risk you're comfortable with. Fixed annuities offer guaranteed returns, which can provide peace of mind. On the other hand, variable and indexed annuities come with more risks but may yield higher returns over time.

Make sure to also evaluate fees and contract terms when reviewing different types of annuities. This can impact your total savings and growth on a tax-deferred basis.

Understanding Risk Tolerance

Understanding risk tolerance is key before buying an annuity. It helps you know how much risk you're willing to take with your money. Some people prefer safety and choose fixed annuities, which offer guaranteed income streams. Others may seek growth and opt for variable annuities, which can be more unpredictable.

Knowing your comfort level with market fluctuations is vital. If the thought of losing money makes you anxious, a safer option might be best. Annuity owner decisions should reflect personal finance goals and risk comfort.

Always evaluate fees and contract terms closely because they vary widely among different types of financial vehicles.

Evaluating Fees and Contract Terms

Fees and contract terms can eat into your returns. Many annuities come with high fees and commissions. This can make a big difference in how much money you keep. Look for fixed annuity guarantees to understand what you will earn.

Pay attention to withdrawal penalties too. These are costs you'll face if you take out money early.

Each contract has its own rules. Make sure you read the fine print carefully. Know what you're agreeing to before committing your funds. Understand tax advantages, like how it grows on a tax-deferred basis until withdrawal.

A clear picture of these details helps avoid surprises down the line. Always evaluate whether the benefits outweigh any cons of annuities for your personal finance goals.

Ensuring Adequate Liquid Savings

Having enough liquid savings is key. You need cash that you can access quickly. Annuities lock your money for a long time. This makes it hard to get funds when you need them.

Look at your expenses and how much money you have in easy-to-reach accounts. A good rule is to keep three to six months' worth of living costs saved up. That way, if an emergency happens, you're not relying solely on an annuity or other investments like mutual funds, which could take time to turn into cash.

Always make sure you're comfortable with the balance between buying an annuity for retirement and having enough liquid savings available for unexpected needs.

Alternatives to Annuities

There are other options besides annuities that can help grow your money wisely. Bonds, CDs, and mutual funds all offer different benefits. These choices might suit your needs better.

Bonds

Bonds can be a good choice for your retirement plan. They are loans made to companies or governments. In return, you get interest payments over time. This income is often stable and predictable.

Buying bonds means you hold them until maturity or sell them before that. You also gain tax-deferred growth on interest until withdrawal. Unlike annuities, bonds usually have lower fees and better liquidity.

However, they do come with risks like market changes impacting their value. Still, many people find bonds appealing as part of their financial strategy for retirement—a solid alternative to buying an annuity for retirement.

Certificates of Deposit (CDs)

Certificates of Deposit, or CDs, are a safe way to save money. You deposit a fixed amount for a set time, usually months or years. In return, the bank pays you interest that is often higher than regular savings accounts. This interest grows on a tax-deferred basis until you take it out.

CDs have specific terms. If you withdraw your money early, there may be penalties. They offer stability and help with planning your savings goals. Since they guarantee returns through the claims paying ability of banks, they can fit into retirement plans well—especially if you're looking for safer options rather than buying an annuity for retirement.

Mutual Funds

Mutual funds pool money from many investors. This allows you to invest in a mix of stocks, bonds, or other assets at once. They are managed by professionals who choose the investments for you. You can buy shares of a mutual fund easily and sell them when needed.

Investing in mutual funds can help grow your savings on a tax-deferred basis. This means you won't pay taxes on gains until you withdraw money from the fund. Some funds even offer dividends or income that can add to your retirement savings.

Plus, they provide diversification, which reduces risk compared to individual stocks.

Hire a Financial Advisor

Annuities can provide guaranteed income, but they're not the right fit for everyone. Understanding the fees, payout options, and tax implications is crucial before making a decision.

A Farther financial advisor can help you evaluate whether an annuity aligns with your retirement goals. Get expert guidance today!

Conclusion

Annuities can be a useful tool for retirement, offering steady income and tax-deferred growth. However, it's important to understand the associated fees and risks before committing.

Make sure your retirement plan aligns with your financial goals. If an annuity feels too complex, consider alternatives like bonds or CDs that might be a better fit.

Take action now—review your options and choose what works best for you. Every decision shapes your financial future, so make it count.

FAQs

1. What does it mean to buy an annuity for retirement?

Buying an annuity for retirement means you contribute money into a financial product that promises to grow tax deferred and pay out a stream of income later, usually during your retirement years.

2. Why should I consider buying an annuity for my retirement?

Annuities can be beneficial because they allow your contributions to grow on a tax-deferred basis. This might lead to more significant growth over time compared to taxable accounts.

3. How do I decide if an annuity is right for me?

Consider factors like the financial strength of the company offering the annuity, how much you can contribute, and whether or not it offers features such as a death benefit.

4. Are there any risks associated with buying an annuity for retirement?

Yes, one key risk is that your money is typically locked in until you reach at least 59½ years old. If you withdraw funds earlier than this age, penalties may apply.