Saving money is a priority for everyone, especially homeowners during tax season. With the right knowledge, you can achieve significant tax savings.

Homeownership unlocks numerous tax deductions. This guide explores mortgage interest deduction, property taxes, and other strategies to lower your tax bill. Looking to reduce what you owe? Let's dive in.

Key Takeaways

- Homeowners can lower their taxable income by deducting mortgage interest on loans up to $750,000 for those taken out after December 15, 2017. Married people filing separately have a limit of $375,000.

- Property tax deductions are capped at $10,000 for single filers and $5,000 for married couples filing separately in 2025.

- You can get tax credits for making energy-efficient upgrades like installing solar panels or efficient windows. Keep all receipts for these improvements.

- Interest on home equity loans and Home Equity Lines of Credit (HELOCs) is deductible if used to buy, build, or improve your home.

- Medically necessary home modifications might qualify you for tax deductions. This includes changes like adding ramps or grab bars.

Key Tax Deductions for Homeowners in 2025

Homeowners can reduce their tax burden in 2025 through various deductions including mortgage interest and energy upgrades. These savings extend to property tax deduction, home equity loan interest, and real estate taxes.

Mortgage Interest Deduction

This deduction allows homeowners to lower their taxable income through mortgage interest payments. It applies to a main home and one additional property. For loans taken after December 15, 2017, but before January 1, 2026, the deduction limit is $750,000. After 2025, unless laws change, the limit may revert to $1 million.

Married individuals filing separately each have a $375,000 limit.

For loans obtained before December 16, 2017, the limit remains at $1 million or $500,000 when filing separately. Points paid at closing and interest from home equity loans or lines of credit are deductible if used to buy, build, or substantially improve your home within these limits.

Property Tax Deduction

Reducing your taxable income is possible through property tax deductions. Homeowners can deduct state and local property taxes paid on their primary residence or a second home. In 2025, the maximum deduction is capped at $10,000 whether you are a single filer or married filing jointly, and $5,000 for married individuals filing separately.

This means only a portion of your payments may be deductible.

Maintain thorough records of property tax payments. These documents are essential when preparing your tax return, as the IRS requires payment proof to claim this deduction. While some homeowners pay mortgage insurance alongside property taxes, those payments typically don't qualify as deductible expenses under current rules.

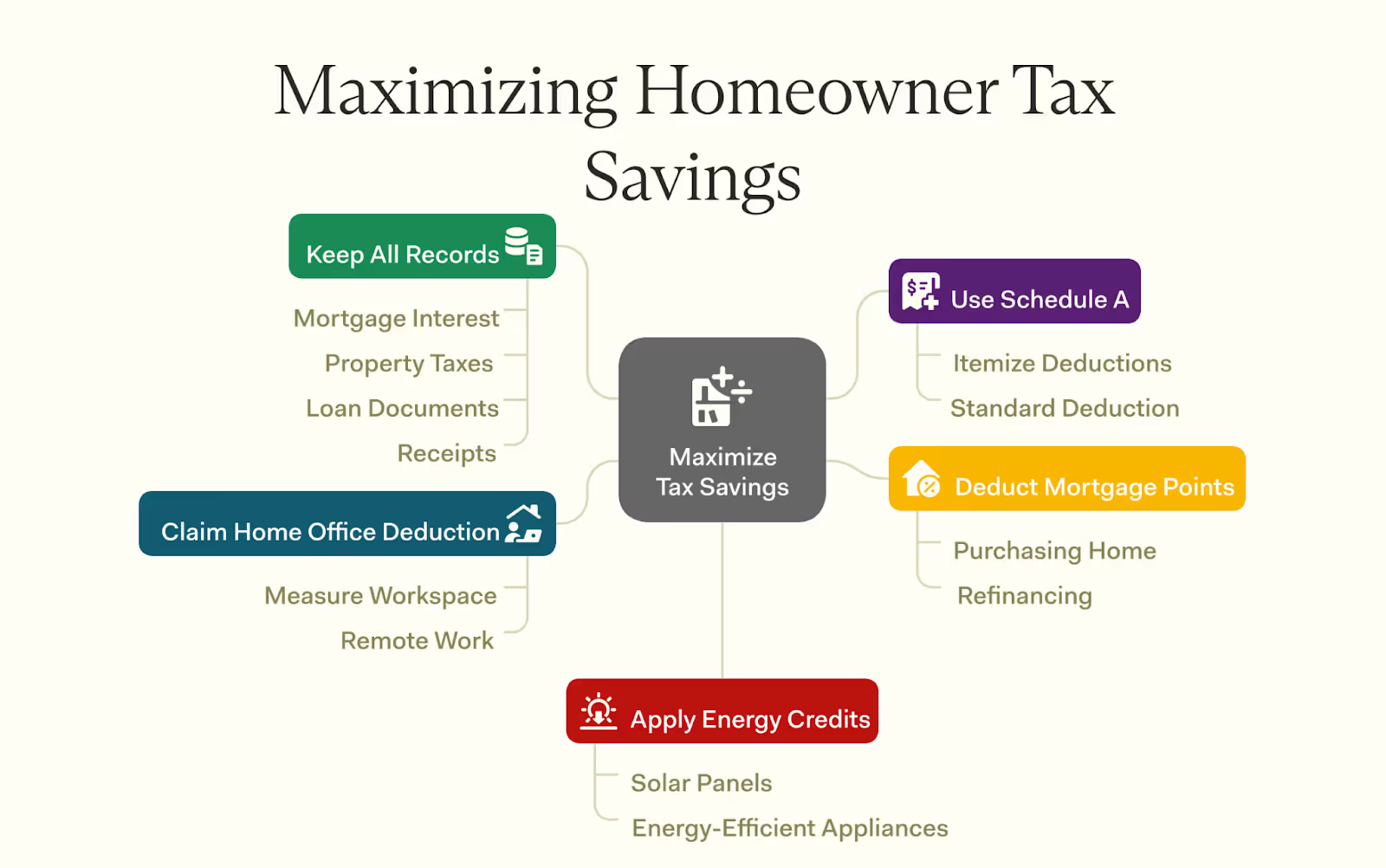

Home Office Deduction

Self-employed homeowners and independent contractors can claim a portion of their home expenses through the Home Office Deduction. This benefit applies to those who use part of their home regularly and exclusively for business.

The deduction can include a percentage of mortgage interest, state and local taxes, and utility bills based on the office's size.

Remote employees generally don't qualify for this deduction. Maintaining detailed records is crucial when filing your income tax return and claiming this benefit.

Residential Energy Credits

Energy-efficient home improvements can yield valuable tax benefits. These credits help offset costs for upgrades to your home's energy systems. Installing solar panels or energy-efficient windows may qualify you for these credits.

Between 2022 and 2032, you can claim 30% of the cost of qualified improvements.

Keep all receipts and documentation related to these upgrades. The IRS has specific guidelines about qualifying improvements, so research before filing. Using residential energy credits reduces your tax liability while supporting environmental sustainability.

Mortgage Points Deduction

When you pay points to reduce your interest rate, you may be eligible for tax deductions. Each point costs 1% of the mortgage amount. For example, two points on a $200,000 mortgage would cost $4,000.

These points are deductible if paid for your primary residence. Points paid on a home purchase loan can be deducted in full during the year paid, while points on refinanced loans must be deducted over the loan's lifetime.

Deducting mortgage interest can provide significant relief from monthly payment burdens. Consult a tax professional to ensure compliance with current tax code requirements.

Tax Benefits of Home Equity Loans and HELOCs

Home equity loans and HELOCs offer potential tax advantages. The interest on these loans may be deductible, providing savings during tax season.

Deductible Interest on Home Equity Loans

Interest paid on home equity loans can be deducted on your tax return under certain conditions. This provides a significant advantage for homeowners. The key requirement is using the loan to buy, build, or substantially improve the home securing the loan.

The IRS only allows this deduction when loan proceeds directly benefit the property securing the loan.

Total debt must not exceed $750,000 for loans originated after December 15, 2017, and before January 1, 2026. For loans after 2025, the limit is scheduled to revert to $1 million unless legislation changes. Interest on amounts above these limits won't qualify as deductible mortgage interest.

Consultation with a tax professional ensures proper application of these rules.

Eligible Lines of Credit for Tax Deductions

Tax deductions are available for certain home-based credit lines. Home equity loans and Home Equity Lines of Credit (HELOCs) may offer deductible interest when you borrow against your home's value.

Qualification depends on using the funds to buy, build, or substantially improve either your principal residence or second home that secures the loan. A tax professional can provide guidance on optimizing these deductions for your specific situation.

Tax Deductions for Specific Home Improvements

Certain home upgrades can lead to tax savings. Improvements related to health needs or energy efficiency may qualify for valuable deductions.

Medically Necessary Home Modifications

Home modifications for medical purposes improve quality of life for those with health challenges. These adaptations make homes safer and more accessible, such as installing ramps or grab bars for mobility assistance.

Tax deductions may be available for these expenses. Modifications supporting medical care often qualify for tax breaks. The IRS provides guidance on which expenses qualify under medical and dental deduction categories.

Eligible modifications include widening doorways or installing chair lifts. Maintaining comprehensive records and receipts for these improvements is essential for tax purposes.

Energy-Efficient Upgrades

Besides reducing utility costs, energy-efficient home improvements may qualify for tax benefits. The residential clean energy credit applies to installations like solar panels and other energy-saving enhancements.

Upgrading insulation, windows, and heating systems can also qualify. These improvements create more comfortable living spaces while potentially reducing your tax liability. Remember that these improvements typically qualify for tax credits rather than deductions, which can be even more valuable.

Common Homeowner Expenses That Are Not Tax-Deductible

Not all homeownership costs qualify for tax deductions. Certain regular expenses like homeowners insurance and routine maintenance don't reduce your tax liability, despite their importance to home maintenance.

Homeowners Insurance

This essential protection covers your home and belongings against risks such as fire, theft, and natural disasters. It also provides liability coverage for injuries occurring on your property.

Despite its importance, homeowners insurance premiums cannot be deducted on your tax return. The IRS doesn't recognize these payments as deductible expenses, even though they're necessary homeownership costs. Nevertheless, maintain good records of these payments for insurance claims and other purposes.

Routine Maintenance and Repairs

The IRS doesn't allow deductions for everyday home maintenance and repair costs. Though homeowners regularly spend on roof repairs, plumbing fixes, and other upkeep, these expenses don't qualify for tax deductions despite keeping homes safe and functional.

Some improvements may eventually qualify for energy efficiency credits or other deductions. Understanding what qualifies as deductible saves time and frustration during tax preparation.

How to Maximize Tax Deductions

Efficient organization of financial records and strategic use of tax forms can help homeowners maximize their deductions and potentially increase tax savings.

Organize Tax Records and Receipts

Maintaining an organized system for tax documents streamlines the filing process. Keep all relevant papers in a designated location, whether physical or digital. Use folders or specialized apps to categorize important documents like mortgage interest statements, property tax receipts, and loan origination fees.

Diligent tracking of homeownership expenses pays dividends at tax time. Store documentation for all potential deductions, including mortgage insurance premiums and business expenses for home office claims.

Organization reduces stress during tax season and helps ensure you claim all eligible deductions.

Use Schedule A for Itemized Deductions

Schedule A enables detailed listing of deductible expenses on your tax return. This form allows you to enumerate costs that reduce your taxable income, including mortgage interest and property taxes.

Include interest paid on home equity loans, but only if the funds were used to buy, build, or substantially improve your primary residence securing the loan.

For some homeowners, itemizing provides greater benefits than the standard deduction. Track all eligible expenses throughout the year and maintain supporting documentation such as receipts and statements.

Maximize Your Tax Savings as a Homeowner

Homeownership offers numerous tax advantages that can be leveraged with proper planning. Strategic management of deductions can significantly reduce your tax obligation.

You can deduct mortgage interest and property taxes on Schedule A. Self-employed individuals using part of their home exclusively for business may deduct home office expenses on Schedule C (Form 1040). Home equity loan interest is deductible on Schedule A only when the loan was used to buy, build, or substantially improve the home securing the loan.

Optimize your homeowner tax benefits. Speak with a Farther financial advisor to develop a tailored tax strategy today!

Conclusion

The 2025 tax landscape offers significant savings opportunities for homeowners. Key deductions include mortgage interest, property taxes, and home office expenses. With organized record-keeping, these benefits become easily accessible.

Applying these strategies consistently leads to tangible financial advantages.

For personalized guidance, consider consulting with a tax professional or financial advisor. Take control of your financial future by maximizing available benefits and enjoying the full advantages of homeownership.

FAQs

1. What tax deductions can homeowners claim in 2025?

Homeowners can claim a variety of tax deductions, including those related to mortgage interest and discount points paid to the mortgage broker. Deductions for state and local taxes, which include property taxes, have a cap of $10,000 for single filers and married couples filing jointly, or $5,000 for married individuals filing separately.

2. Can sellers deduct any costs from their capital gains in 2025?

Yes! In 2025, sellers can reduce their capital gains by subtracting certain expenses involved in selling a home, such as real estate commissions and legal fees. While transfer taxes and title fees generally cannot be deducted, they are added to the property's cost basis, thus potentially reducing the taxable gain when selling the property.

3. Are there specific rules for claiming discount points on my tax return?

Absolutely! Discount points paid to your mortgage broker can often be deducted in the year they are paid if they are for your primary residence under certain conditions. However, if the points are related to a refinance or a second home, they typically must be amortized over the life of the loan. It's important to consult a tax professional to understand how these deductions apply to your specific situation.

4. How do down payments factor into homeowner's tax deductions in 2025?

While down payments are not directly deductible, they can influence the total mortgage interest paid as a smaller mortgage results from a larger down payment. However, this does not affect the mortgage interest deduction, which is solely based on the actual interest paid during the tax year.