The steady rhythm of giving during your working years – where each paycheck made charitable donations straightforward – shifts dramatically in retirement.

Now, with income flowing from multiple sources at different times, you may want to maintain your commitment to giving while protecting your long-term financial security. It's a balance many retirees seek but aren't sure how to achieve.

Smart Strategies for Retirement Giving

Whether you're receiving Social Security payments, pension deposits, or making strategic withdrawals from retirement accounts, there's a clear path to maintaining your charitable commitments. Your income sources may have changed, but your dedication to giving back doesn't have to.

Let's explore how to structure donations in retirement so you can give meaningfully while ensuring your own needs are met – creating a sustainable approach that supports both your tithing goals and your financial independence.

Give cheerfully and according to what you have. Tithing should fit into your new budget without causing stress. Decide if you want to tithe on gross income or net income after taxes. Knowing this helps plan your generosity in retirement years.

1. Calculate Tithes on Retirement Income

When calculating tithes on retirement income, consider sources such as Social Security benefits, pensions, annuities, and other lifetime fixed income sources.

Each of these sources may have different tax implications, and it's important to manage these intricacies when determining your tithing amount.

a. Social Security Benefits

Social Security benefits are a key income source for many people in retirement.

You contribute to Social Security through payroll taxes during your working years. Your Social Security benefit is calculated based on your highest 35 years of indexed earnings history, not simply on how much you paid into the system.

This makes it different from other retirement income sources. Some individuals choose not to tithe on their Social Security benefits because they've already paid FICA taxes on their earnings during working years, while others view it as current income eligible for tithing regardless of previous taxation.

When considering tithing on Social Security benefits, it's important to understand that up to 85% of your benefits may be subject to federal income tax depending on your combined income. Some individuals choose to tithe on the net amount after taxes, while others tithe on the gross amount. This decision is personal and often guided by your spiritual beliefs and financial situation.

b. Pensions and Annuities

Transitioning from Social Security, pensions, and annuities are integral to many retirement revenue streams, especially when an employer's pension plan pays you post-retirement.

This disbursement is determined based on your work duration and the earned salary during that period. Many pensions provide consistent payments throughout retirement, similar to receiving a regular paycheck. However, pension structures vary—some may offer lump-sum distribution options or payments for a specific period rather than lifetime guarantees.

Annuities function somewhat distinctively. You purchase an annuity with a lump sum or via installments over a period. Later, it starts reimbursing you from a future date. These disbursements can extend throughout your life or for a specified number of years.

Pensions and annuities both ensure a steady inflow of income but it's crucial to verify their federal and state tax obligations.

c. Investment Income and Capital Gains

Investment revenue and capital profits in retirement can affect your tithing calculations.

Revenue from brokerage accounts, dividends, and rental properties are all taxable sources that may need to be considered when calculating tithes on retirement income.

Capital gains tax is also something to keep in mind as it applies to the earned gains over time from investment accounts.

Retirement savings often include investments that generate taxable income and potential tax benefits, which could influence the ability to tithe while enjoying retirement comfortably.

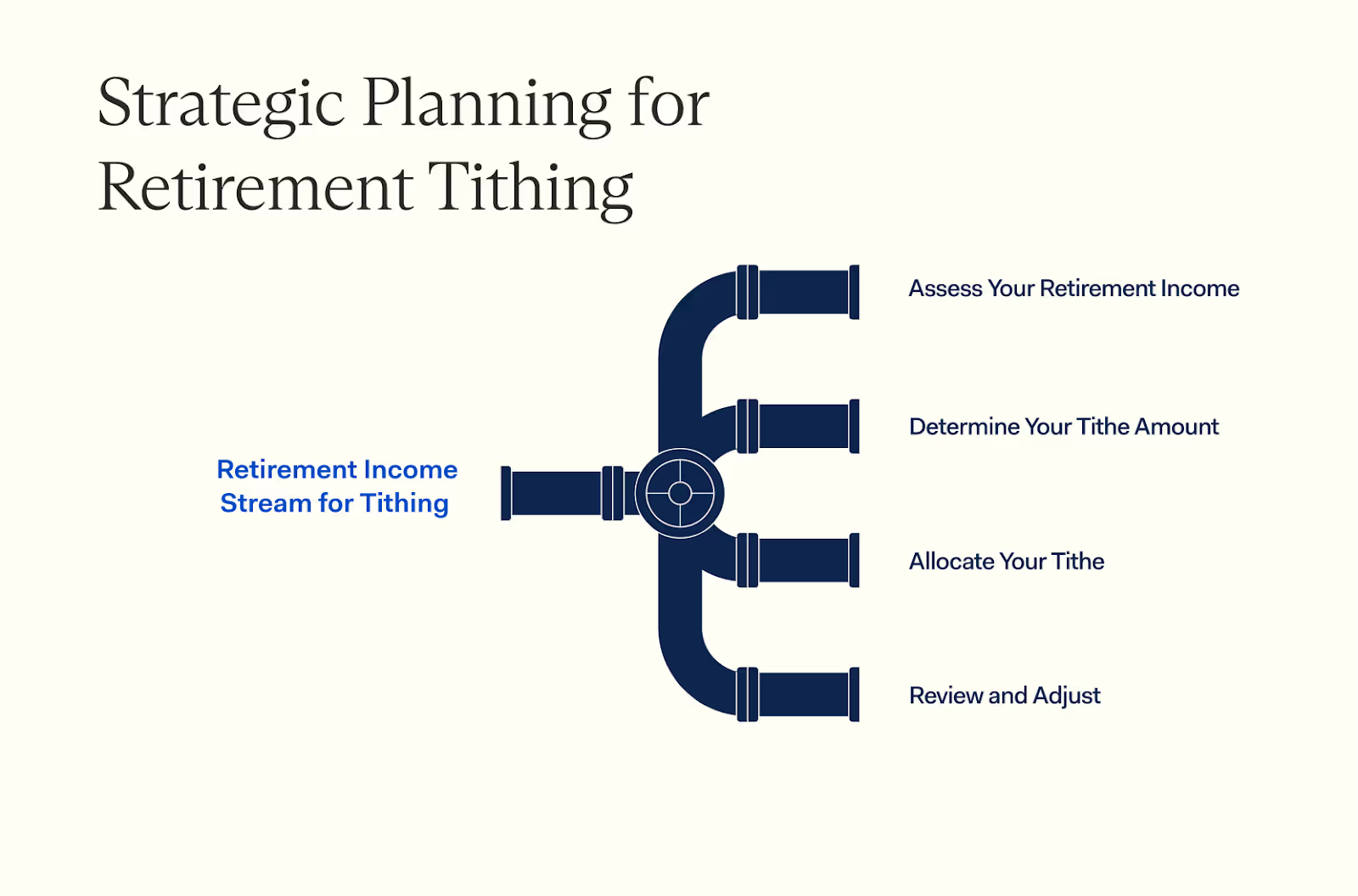

2. Create a Retirement Income Stream for Tithing

Creating a retirement income stream for tithing requires careful planning and consideration of various factors.

One approach is to allocate a portion of your total retirement income to tithing, taking into account your gross income, social security income, and other sources of retirement income.

It's essential to consider the tax implications of your retirement distributions, including tax withheld money, to ensure that you're optimizing your tithing strategy.

When creating a retirement income stream for tithing, consider the following steps:

- Assess Your Retirement Income: Determine your total retirement income from all sources, including social security benefits, pensions, annuities, and retirement accounts. This comprehensive calculation will give you a clear picture of your financial landscape.

- Determine Your Tithe Amount: Decide on a tithe amount based on your gross income. Consider your personal financial situation and goals to ensure that your tithing is both generous and sustainable.

- Allocate Your Tithe: Set aside your tithe amount from your retirement income stream. Be mindful of tax implications and potential deductions to maximize the efficiency of your giving.

- Review and Adjust: Regularly review your retirement income stream and tithe amount. Life changes and financial shifts may require adjustments to ensure that you continue to meet your financial and spiritual goals.

3. Tax Implications of Tithing in Retirement

When withdrawing funds from your traditional IRA to donate to charity, you will pay ordinary income tax on those amounts unless you utilize strategies like Qualified Charitable Distributions (QCDs). Qualified withdrawals from Roth IRAs are already tax-free, but different rules apply for their use in charitable giving.

a. Qualified Charitable Distributions (QCDs)

When retired, you have the option to donate directly from your IRA to a qualified charity, known as a Qualified Charitable Distribution (QCD).

The amount donated counts towards the required minimum distribution (RMD) and is excluded from your taxable income.

This provides a tax-efficient way for retirees who don't itemize deductions to support charitable causes.

Utilizing QCDs enables retirees to back causes they are passionate about while lessening their taxable income.

b. Tax Deductions for Charitable Giving

When considering tax deductions for charitable giving in retirement, it's beneficial to explore Qualified Charitable Distributions (QCDs) and the potential advantages they provide.

Starting in 2025, QCDs enable individuals over 70½ years old to contribute up to $108,000 directly from their IRA to qualified charities without it being considered taxable income, resulting in substantial tax savings while supporting charitable causes.

Discussing these approaches with a financial advisor can offer personalized perspectives on optimizing tax deductions for charitable giving during retirement, guaranteeing that your charitable efforts align with your comprehensive financial plan and goals.

4 Strategies for Stress-Free Tithing

1. The "Same Dollar Amount" Approach

Tithing the same dollar amount regardless of income changes allows for a consistent approach to giving in retirement. It can be a simple and stable method, bringing peace of mind and ease to your giving practice.

- Consistency: This approach involves steadfastly tithing the same fixed dollar amount regardless of fluctuating income in retirement.

- Predictability: You can plan and budget effectively as you know the exact amount you will tithe each time, providing stability in your charitable giving.

- Peace of Mind: By adhering to a set dollar amount, you avoid stress or confusion related to varying income sources and their impact on tithing.

- Honoring Commitment: It allows you to uphold your commitment to tithing without being overly affected by financial fluctuations.

- Simplicity: This approach is easy to execute, requiring minimal calculations and adjustments over time compared to other methods.

Keep in mind that adjusting this fixed amount may be necessary based on changes in your financial circumstances, ensuring that your tithing remains sustainable within your means.

2. The "Percentage of Spending" Approach

To use the "Percentage of Spending" approach:

- Calculate your annual spending.

- Determine a percentage of your spending to allocate for tithing.

- Adjust the tithing amount based on changes in your spending.

- Monitor your spending regularly to maintain the appropriate tithing percentage.

3. The "Percentage of Portfolio Growth" Approach

When transitioning from the "Percentage of Spending" Approach to the next approach, consider the "Percentage of Portfolio Growth" approach.

This approach focuses on allocating a percentage based on the growth of your investment portfolio.

Here's how it works:

- Calculate the annual growth of your investment portfolio.

- Determine a suitable proportion to donate based on this growth.

- Regularly review and adjust your donation percentage as your portfolio grows or declines.

- This approach allows for flexibility in giving, aligning your donations with the performance of your investments.

- It ensures that your giving is sustainable and adjusts in accordance with changes in your financial situation.

Keep in mind, this method enables you to contribute in proportion to how well your investments are performing without affecting your financial stability.

4. The "Finish Line" Approach

The "Finish Line" approach focuses on dedicating a specific amount or percentage towards the end of your retirement, aligning with the goal of leaving a legacy or giving generously after ensuring one's own financial security.

This approach allows retirees to prioritize their own needs during retirement while putting aside a portion for giving as they near the later stages of life.

- Rather than committing to regular tithing throughout retirement, this approach involves setting a target age or milestone when retirees plan to start giving more substantially.

- It enables them to enjoy their retirement and take care of their needs first before dedicating to increased giving at a set point in time.

- Retirees can plan for this by gradually increasing their savings and investments leading up to the designated "finish line," ensuring they have resources available for both personal use and generous giving.

Balance Tithing and Other Financial Priorities

When you're retired, tithing needs to be balanced with your other financial obligations.

During your working years, you pay payroll taxes into Social Security, which provides an income stream in retirement. It's important to prioritize essential living expenses like housing, healthcare, and food before tithing.

Assess your retirement income sources such as social security, pensions, annuities, and investment gains to determine how much you can comfortably tithe without compromising your financial stability.

To maintain a healthy balance between tithing and other financial priorities during retirement, seek professional advice from financial advisors who specialize in retirement planning and charitable giving.

Faith-Based Approach to Tithing

A faith-based approach to tithing involves trusting in God's provision and guidance in your financial decisions.

It's essential to remember that tithing is a spiritual practice that demonstrates your faith and trust in God's goodness.

When adopting a faith-based approach to tithing, consider the following principles:

- Trust in God's Provision: Believe that God will provide for your needs, even as you tithe. This trust can bring peace and confidence in your financial decisions.

- Prioritize Giving: Make giving a priority in your financial decisions, recognizing that it's a spiritual practice that honors God. By putting tithing first, you align your finances with your faith.

- Seek Guidance: Seek guidance from scripture, prayer, and spiritual leaders to inform your tithing decisions. This spiritual support can provide clarity and direction.

- Cultivate Gratitude: Cultivate a spirit of gratitude for God's blessings, recognizing that everything you have belongs to Him. Gratitude can transform your perspective on giving and increase your joy in tithing.

Overcome Common Obstacles to Tithing

Common obstacles to tithing include financial constraints, uncertainty about how to tithe, and lack of motivation.

To overcome these obstacles, consider the following strategies:

- Start Small: Begin with a manageable tithe amount and gradually increase it over time. This approach allows you to build the habit of giving without overwhelming your budget.

- Educate Yourself: Learn about tithing principles, tax implications, and retirement income streams to make informed decisions. Knowledge can empower you to tithe confidently and effectively.

- Seek Accountability: Share your tithing goals with a trusted friend or spiritual leader to increase motivation and accountability. Having someone to support and encourage you can make a significant difference.

- Focus on the Benefits: Remember the spiritual benefits of tithing, including increased faith, gratitude, and generosity. Keeping these benefits in mind can inspire you to continue giving, even when it's challenging.

Giving Beyond Money: Time and Talent

Giving beyond money involves sharing your time, talent, and resources to serve others and honor God. Consider the following ways to give beyond money:

- Volunteer: Share your time and skills with local charities, churches, or community organizations. Volunteering can make a significant impact and provide a sense of fulfillment.

- Mentorship: Offer guidance and mentorship to others, sharing your experience and expertise. Mentorship can be a powerful way to invest in the next generation.

- Skill-Based Giving: Use your skills to create products or services that benefit others, such as crafting, writing, or designing. Your unique talents can be a valuable gift to those in need.

- Prayer and Intercession: Offer prayer and intercession for others, recognizing the power of spiritual support. Prayer can be a profound way to give, even when financial resources are limited.

Adapt Tithes to Life Changes in Retirement

As retirement brings changes in income, it's crucial to adapt your tithing practices.

Consider adjusting the amount or method of tithing based on your new financial situation.

For example, if there's a decrease in income, you might tithe based on social security benefits or other retirement income sources instead of the pre-retirement salary.

Moreover, re-evaluate strategies like giving a percentage of spending or portfolio growth rather than fixating on a set dollar amount. This adaptability can help ensure continued support for causes you value while maintaining financial stability during retirement.

Consult Financial Advisors for Tithing Guidance

When it comes to managing the complexities of tithing in retirement, seeking guidance from financial advisors is crucial.

A Farther financial advisor can help you create a giving strategy that aligns with your values while ensuring your retirement funds last. When selecting an advisor, look for proper credentials such as CFP® certification and verify they operate under a fiduciary standard.

These experts can provide personalized strategies for calculating and managing tithes on various sources of retirement income, such as social security benefits, pensions, annuities, and investment income.

They can offer detailed advice on tax implications, including qualified charitable distributions (QCDs) and deductions for charitable giving, ensuring that retirees optimize their giving while minimizing tax burdens.

In Closing: Your Path to Purposeful Giving

Tithing in retirement should energize your spirit, not drain your peace of mind. Armed with the right strategies, you can confidently direct your retirement cash flow – whether from Social Security, investment gains, or pension payouts – toward the causes that matter most to you.

By choosing an approach that aligns with your values and financial reality, you're not just maintaining a giving practice – you're creating a lasting legacy of generosity that works in harmony with your retirement dreams.

FAQs

1. What does it mean to tithe in retirement?

Tithing in retirement means giving a portion of your retirement income, usually 10%, to a religious organization or charity. It can come from various sources such as social security income, rental income, and withdrawals from brokerage investment accounts.

2. Do I need to pay tithes on my Social Security amount and pension plan?

You may choose to tithe on your net social security income after federal and state taxes are paid. If your employer's pension plan pays you an income stream that has already been tithed when you were working, then you might not need to tithe again.

3. How do I calculate the amount for tithing during retirement?

When calculating your tithe, consider all potential tax-free income sources including returns of principal amounts from investments that have already been taxed or tithed before retirement. Then decide whether to give at least 10% based on this total.

4. Should I still be paying tithes if my only source of money is what I saved while working?

If you already tithed on income before it was placed in retirement accounts, some faith traditions consider it acceptable not to tithe again on withdrawals. However, religious interpretations vary widely on this matter, and you may wish to consult with your spiritual leaders about the approach that best aligns with your faith tradition.

5. Is there any way around paying taxes on my retired life's earnings?

Yes, there are legal tax planning strategies that can help minimize taxes in retirement. These include strategic withdrawal timing from different retirement accounts, tax diversification (using a mix of traditional and Roth accounts), managing income to stay in lower tax brackets, and utilizing tax-advantaged investment options. However, these strategies should be implemented with guidance from qualified tax professionals to ensure compliance with tax laws.

6. What if it becomes hard for me financially but I still want to continue with the habit of giving?

If it becomes hard for you financially to continue tithing, consider the following strategies:

- Reassess Your Budget: Review your budget to identify areas where you can reduce expenses and allocate more funds to tithing. Small adjustments can free up resources for giving.

- Seek Financial Guidance: Consult with a financial advisor to explore options for optimizing your retirement income stream and reducing taxes. Professional advice can help you find ways to continue tithing without compromising your financial stability.

- Prioritize Needs Over Wants: Distinguish between essential expenses and discretionary spending, prioritizing needs over wants. This prioritization can help you maintain your commitment to tithing.

- Consider Alternative Forms of Giving: Explore alternative forms of giving, such as volunteering or skill-based giving, to continue honoring God and serving others. Even when financial resources are limited, your time and talents can make a significant impact.

By incorporating these strategies into your tithing practice, you can continue to honor God with your finances, even in retirement.

6. What options do I have if I can't make room in my budget for a regular tithe?

Everyday philanthropy is a concept where even though one might find it hard making ends meet during old age; they still contribute smaller amounts regularly towards causes they believe in. It helps them enjoy retirement comfortably while still making a difference.