Planning for retirement can be tricky. You want to make sure your money lasts as long as you do, but figuring out how much to save and spend isn't easy.

The 4 percent rule for retirement is a popular guide that many people use. This rule suggests withdrawing 4% of your retirement savings in the first year and adjusting it each year for inflation after that.

Key Takeaways

- The 4% rule helps retirees figure out how much to withdraw each year, starting with 4% of their savings and adjusting for inflation. It aims to make money last at least 30 years.

- Market conditions have changed since the rule was created in the 1990s. Interest rates are low and people live longer, which may affect how well the rule works now.

- Alternatives like dynamic withdrawal strategies or using annuities can offer more flexibility and security in retirement planning compared to sticking strictly to the 4% rule.

What Is the 4% Rule?

This retirement guideline helps retirees determine how much money they can withdraw from their savings each year without running out too soon. It's based on years of market study, suggesting you start by withdrawing 4% in your first retirement year, then adjust that amount for inflation after.

Definition and overview

The 4% rule is a retirement spending plan based on research by financial planner William Bengen. This rule suggests that you can withdraw 4% from your retirement portfolio in the first year of retirement. After that, adjust withdrawals for inflation each year.

With this method, there's a very high probability your money will last at least 30 years.

Using the 4% rule helps reduce the risk of running out of money in retirement.

Historical data backs up this strategy. It assumes a balanced portfolio of stocks and bonds to support annual withdrawals without depleting the nest egg too soon. Now, let's look at how exactly this rule works in practice.

Historical context of the rule

The 4% rule became popular in the 1990s. It started from a study known as the "Trinity Study." Researchers looked at different retirement scenarios. Their goal was to find a safe withdrawal rate from retirement funds.

They found that withdrawing 4% each year let people maintain their lifestyle for about 30 years without running out of money.

This finding helped many financial planners and retirees. It gave them a simple way to plan withdrawals for retirement expenses. But times have changed since then, and market conditions differ now.

Many wonder if the rule still works today.

How the 4% Rule Works

To implement this strategy, you begin by withdrawing 4% of your retirement savings each year, then adjust that amount for inflation as time goes on.

Initial withdrawal rate

The initial withdrawal rate is a key part of the 4% rule. This rate suggests that retirees can take out 4% of their retirement account each year. For example, if your retirement savings total $500,000, you could withdraw $20,000 in the first year.

This amount helps cover living expenses while preserving your investments for future years. The goal is to set a steady income stream without running out of money too soon. Adjustments are made over time for inflation to keep up with rising costs.

Adjusting for inflation

After setting the initial withdrawal rate, you need to think about inflation. Inflation means prices go up over time. This can eat into your retirement income. The 4% rule suggests you adjust your withdrawals each year based on inflation rates.

By doing this, you'll keep pace with rising costs.

For example, if you start with $40,000 in yearly withdrawals and inflation is 2%, you'd take out $40,800 the next year. This adjustment helps ensure that your spending needs are met throughout retirement years.

Failing to adjust for inflation could risk running short on money as prices rise. Consider using market data to track how inflation affects your budget and plan accordingly.

Assumptions Behind the 4% Rule

The strategy rests on a few key ideas. It assumes that your investment mix, like stocks and bonds, is solid enough to handle market ups and downs. Life expectancy also plays a big role—longer lives mean you'll need money for more years.

Portfolio composition

Portfolio composition is key to the 4% rule. It refers to how a retirement plan mixes different types of investments, like stocks and bonds. The right mix affects returns, risk, and overall growth.

Investors often look for a balance between large cap stocks and safer assets like bonds. This mix can help manage market fluctuations. Many financial advisors suggest having about 60% in stocks and 40% in bonds for a good starting point.

Each person's situation is unique, based on their net worth, life expectancy, and retirement goals. Adjusting the portfolio as needs change is essential too.

Market performance

Market performance plays a big role in the 4% rule. This rule is based on how stocks and bonds perform over time. Historically, solid market gains helped retirees withdraw that 4% safely.

But markets can change. Low stock and bond returns could put your retirement at risk.

During tough market times, the value of investments may drop. This affects what you can take out each year without running low on money. If market trends shift downward, your withdrawals might need to be adjusted, which complicates things for retirees today.

Next, we'll examine how life expectancy impacts these plans.

Life expectancy

Life expectancy affects retirement planning. People now live longer than before. The average life expectancy has increased over the years, and many retire at 65 or older. This adds more years to your retirement savings.

Longevity risk is a key issue. If you retire early or live longer than expected, you could run out of money. The 4% rule assumes retirees will spend their savings over 30 years. However, if life expectancy rises, withdrawals might need adjustment to avoid shortage later on. Retirement withdrawals require careful thought around how long your money needs to last.

Pros of the 4% Rule

The 4% Rule offers simplicity. It helps people manage their retirement savings without worry. You can take out a set amount each year, which reduces the chance of running out of money.

Simplicity and ease of use

The 4% Rule is simple and easy to understand. It suggests that retirees can withdraw 4% of their savings each year without running out of money. This straightforward approach makes financial planning less stressful.

Using the rule means you don't need complex calculations or formulas. Just take your total investment accounts, multiply by 0.04, and you have your annual withdrawal amount. Many find this helpful guideline very appealing, especially when considering market risks and future expenses like medical costs or required minimum distributions from traditional IRAs or Roth IRAs.

Helps reduce the risk of running out of money

The 4% rule offers a simple way to withdraw money. It helps reduce the risk of running out of cash during retirement. By withdrawing just 4% each year, retirees can stretch their savings longer.

This strategy aims to keep funds steady in good years and bad.

Many people worry about medical expenses or market crashes that could deplete their savings quickly. The 4% rule provides reassurance against these key risks. It allows for planned withdrawals while adjusting for inflation over time.

This makes retirement planning less stressful and more manageable for many individuals seeking social security benefits or other income sources.

Cons of the 4% Rule

This approach has some downsides. It might not work well when interest rates are low or during market dips.

Potential issues in a low-yield environment

In a low-yield environment, the 4% rule faces challenges. Investors often see lower returns on their investments. This can make it hard to maintain the initial withdrawal rate over time.

Research suggests that while retirees may face challenges in sustaining withdrawals when interest rates are low, the overall sustainability of retirement income depends on factors like portfolio diversification and spending flexibility. It's not solely reliant on the performance of interest rates.

Market performance affects how far your savings go. If stocks and bonds do not perform well, you may need to adjust your lifestyle or spending habits. Tax rates also play a role in retirement income.

A higher tax status can take away more from your withdrawals, further stretching resources thin during retirement years. Not everyone has enough saved for unexpected costs in this type of market climate.

Inflexibility during market downturns

The 4% rule has limits, especially during market downturns. It can restrict your ability to adapt. If the stock market drops, sticking to that withdrawal may hurt you more. You might withdraw too much when your investments lose value.

This inflexibility can lead to running out of money faster than expected. The rule is based on a fixed percentage withdrawal adjusted for inflation annually, not a fixed dollar amount each year. In tough times, adjusting withdrawals is crucial to preserve funds for retirement.

Without this flexibility, it's hard to feel secure in your financial future.

Does the 4% Rule Still Work Today?

Many experts think this approach needs a fresh look due to rising costs and longer lifespans.

Modern market conditions and challenges

Today's market conditions present significant challenges. Interest rates have been low for years, which can impact bond returns, though the overall sustainability of retirement withdrawals depends on factors such as portfolio diversification and spending flexibility. It's not solely determined by interest rates. Many people view the 4% rule as a guideline for how much to safely withdraw from retirement savings annually, but its effectiveness may vary based on current economic conditions.

Longer retirements pose a challenge too. People are living longer, which means more time in retirement. A lower withdrawal rate might be needed to avoid running out of money. Financial advisors suggest alternative strategies that could fit better with modern challenges and help ensure financial security during retirement.

Impacts of longer retirements

Longer retirements mean you need more savings. People are living longer. They want to enjoy their golden years, but this can strain finances. The 4% Rule was originally designed for a 30-year retirement period, but with increasing life expectancies, retirees may need to plan for longer durations.

If you live beyond that, your money may run low.

Social Security benefits are intended to supplement retirement income and are not designed to cover all expenses. Retirees should plan for additional income sources. Rising costs mean what worked for past generations may not work now. Inflation reduces purchasing power over time, affecting the real value of money. Retirees should consider inflation in their withdrawal strategies.

This increases the risk of running out of money if you're using the 4% Rule without thinking about long-term needs.

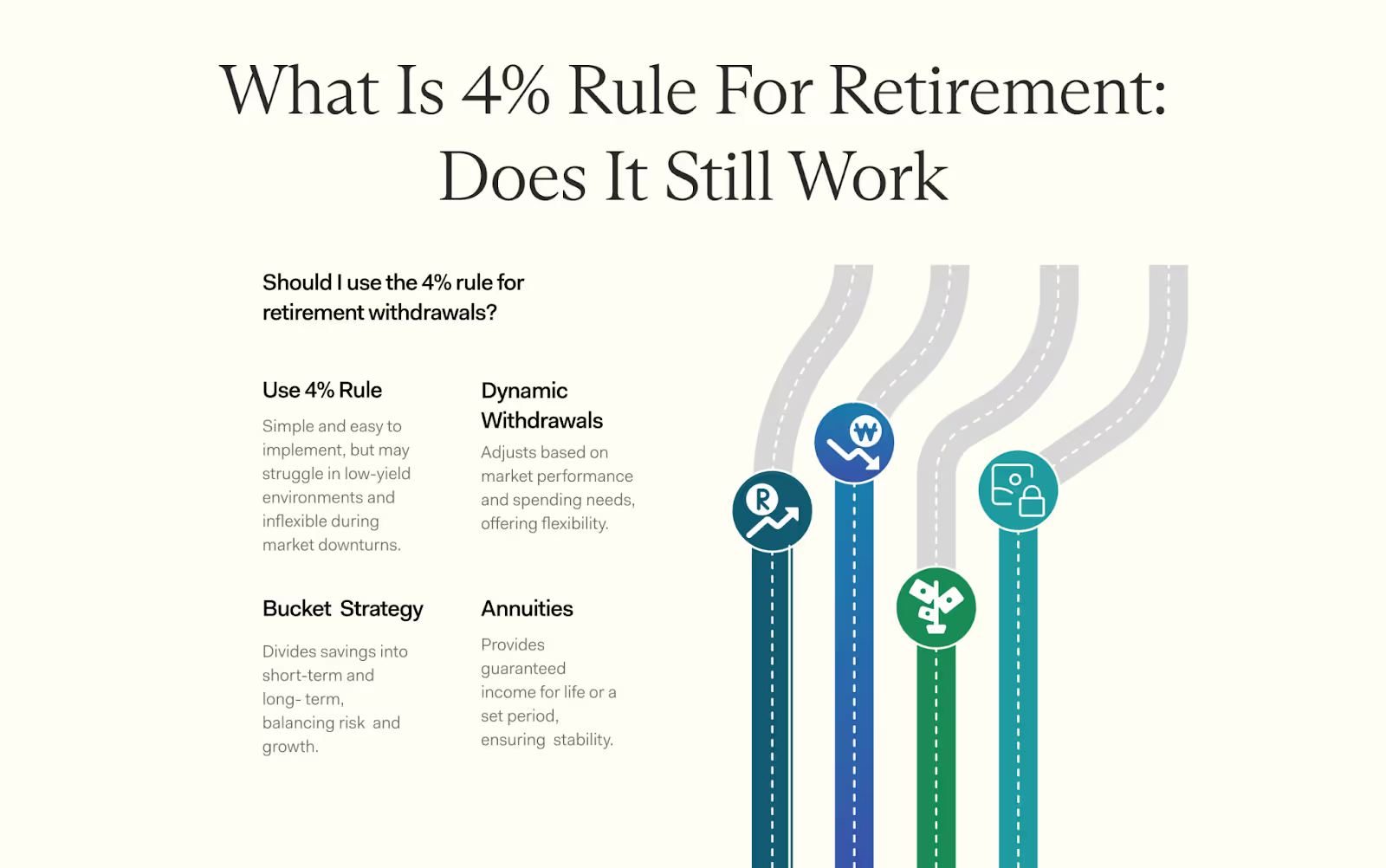

Alternative Strategies to the 4% Rule

There are other ways to withdraw money in retirement. You can try dynamic withdrawal strategies, or the bucket strategy for steady income. Annuities might also give you guaranteed cash flow.

Dynamic withdrawal strategies

Dynamic withdrawal strategies adjust how much money you take out each year. These methods can help you manage your retirement funds better.

- Adjust withdrawals based on market performance. If the market does well, you can take out more. If it struggles, lower your withdrawals to conserve money.

- Factor in personal spending needs. Your expenses might change over time. If they rise or fall, alter your withdrawal amount accordingly.

- Use a percentage of your portfolio balance for each year's withdrawal. This ties your income to how well your investments are doing. It helps avoid taking out too much during downturns.

- Incorporate a floor and ceiling for withdrawals. Set a minimum to cover essential costs and a maximum based on portfolio health.

- Review and adjust regularly—at least once a year is best—based on life changes and investment performance.

Dynamic strategies may offer flexibility that the 4% rule lacks. Next, let's explore the bucket strategy!

Bucket strategy

The bucket strategy divides retirement savings into different "buckets." Each bucket has a specific purpose and time frame for withdrawals. For instance, the first bucket can hold cash or short-term investments for near-term expenses.

This way, you don't need to sell stocks during a market dip. The next bucket can include longer-term investments that have more growth potential.

This method helps manage risk and offers flexibility in spending. With markets changing often, using the bucket strategy could be helpful against running out of money in retirement.

It's simple to understand and puts a plan in place for various needs, like covering bills now while also investing for later years. Now, let's look at annuities and guaranteed income as another option for retirement planning.

Annuities and guaranteed income

Annuities can be a solid choice for retirement. They offer guaranteed income, which adds security to your financial plan. With annuities, you pay a lump sum upfront. Then, the company pays you back through regular payments over time.

This can help ensure that you won't run out of money.

Options vary widely with annuities. Some let you take payouts for life while others may pay out for a set number of years. It's wise to compare types and fees before deciding on an option that fits your needs.

Using the 4% Rule alongside annuities might give you more peace of mind in retirement by balancing risks and ensuring steady cash flow during those golden years.

Is the 4% Rule Right for Your Retirement?

The 4% rule has long been a popular strategy for retirees, but with changing market conditions, inflation, and longer life expectancies, it may not be a one-size-fits-all solution. A personalized withdrawal strategy can help ensure your savings last while meeting your lifestyle needs.

A Farther financial advisor can assess your unique situation and create a sustainable retirement income plan. Schedule a consultation today to build a tailored approach for your retirement.