Afraid your retirement savings won't last? It's a valid concern as lifespans increase and healthcare costs rise.

Longevity risk—outliving your money—is one of retirement's biggest challenges. This guide explores practical strategies to extend your savings, including annuities for guaranteed income streams and sustainable withdrawal approaches that balance current needs with future security. Learn effective spending adjustments to ensure your retirement funds support you throughout your golden years.

Key Takeaways

- Living longer and health care costs can risk your retirement savings. Plan for these expenses early.

- Diversify investments and use the 4% withdrawal rule carefully to handle market changes.

- Annuities offer steady income, and long-term care insurance covers unexpected health costs.

- Cutting back on spending and considering part-time work can extend your savings during retirement.

- Tax-advantaged accounts like IRAs help save money with fewer taxes, making funds last longer.

Key Risks to Retirement Savings

Your retirement savings are at risk from longevity, healthcare costs, and market fluctuations. These factors can quickly deplete your funds.

Considering the retirement age and its implications on financial planning is crucial. Working beyond the full retirement age of 67 can lead to increased Social Security payments and enhanced savings.

Longevity risk

The prospect of outliving your retirement savings presents a significant challenge in financial planning. Delaying retirement age can help mitigate longevity risk by increasing Social Security payments and allowing more time to save. With life expectancy rising, retirees might need their funds to last 20 to 30 years after retiring. Addressing this longevity risk is essential to avoid financial trouble later.

Healthcare costs are another challenge for retirement savings.

Healthcare costs

Healthcare costs pose a big challenge for retirement savers. Planning for these expenses becomes even more crucial as one approaches retirement age. They can drain your funds quickly. As you age, these costs often rise due to long-term care needs and medical expenses.

For many retirees, healthcare takes up a large part of their budget. It's essential to plan ahead and set aside enough money to cover these unexpected bills.

Long-term care insurance can help manage some of these costs. Without it, seniors might struggle with high nursing home fees or in-home care expenses that eat into savings. Social Security benefits may not fully cover healthcare needs either.

Having a solid strategy for handling future medical costs is key to avoiding the risk of outliving your money. Planning for healthcare means planning for peace of mind.

Market volatility

Market volatility can shake your retirement savings. Prices of stocks and bonds go up and down all the time. This movement can hurt investors, especially retirees who rely on steady income.

A bear market, for instance, could reduce the value of your investments quickly. If you're not careful with your asset allocation, you might risk outliving your retirement savings.

To manage this risk, diversifying your investment portfolio is key. Spread your money across different assets like cash, bonds, or stocks to lessen potential losses. Keeping an eye on interest rates also matters—they impact bond prices and can add another layer of uncertainty to today's retirees' plans.

Strategies to Address Longevity Risk and Ensure Your Savings Last

To make your savings last, create a clear spending plan. This plan should show how much you can spend each month without running out of money.

Develop a realistic spending plan

Creating a realistic spending plan is key for retirement. Considering your retirement age is crucial, as delaying retirement can increase Social Security payments and enhance savings, impacting your overall spending plan. Start by tracking your income and expenses. Know how much you can spend each month without running out of money. Include all costs, like healthcare and long-term care.

Many people underestimate these needs.

Adjust your lifestyle if necessary to fit your budget. Cut back on discretionary expenses, such as dining out or vacations. Baby boomers often face tough choices about their retirement wealth.

Diversify your investment portfolio

Diversifying your investment portfolio is key to protecting your savings. This means spreading your money across different types of investments. You might choose stocks, bonds, and money market funds.

Each option carries its own risk and reward. A mixed portfolio can help you balance these risks.

Inflation can erode purchasing power over time. By diversifying, you aim for growth that outpaces inflation. Talk to financial professionals for advice on how to build a diversified portfolio that fits your retirement goals.

It's also important to adjust your portfolio as needed over time.

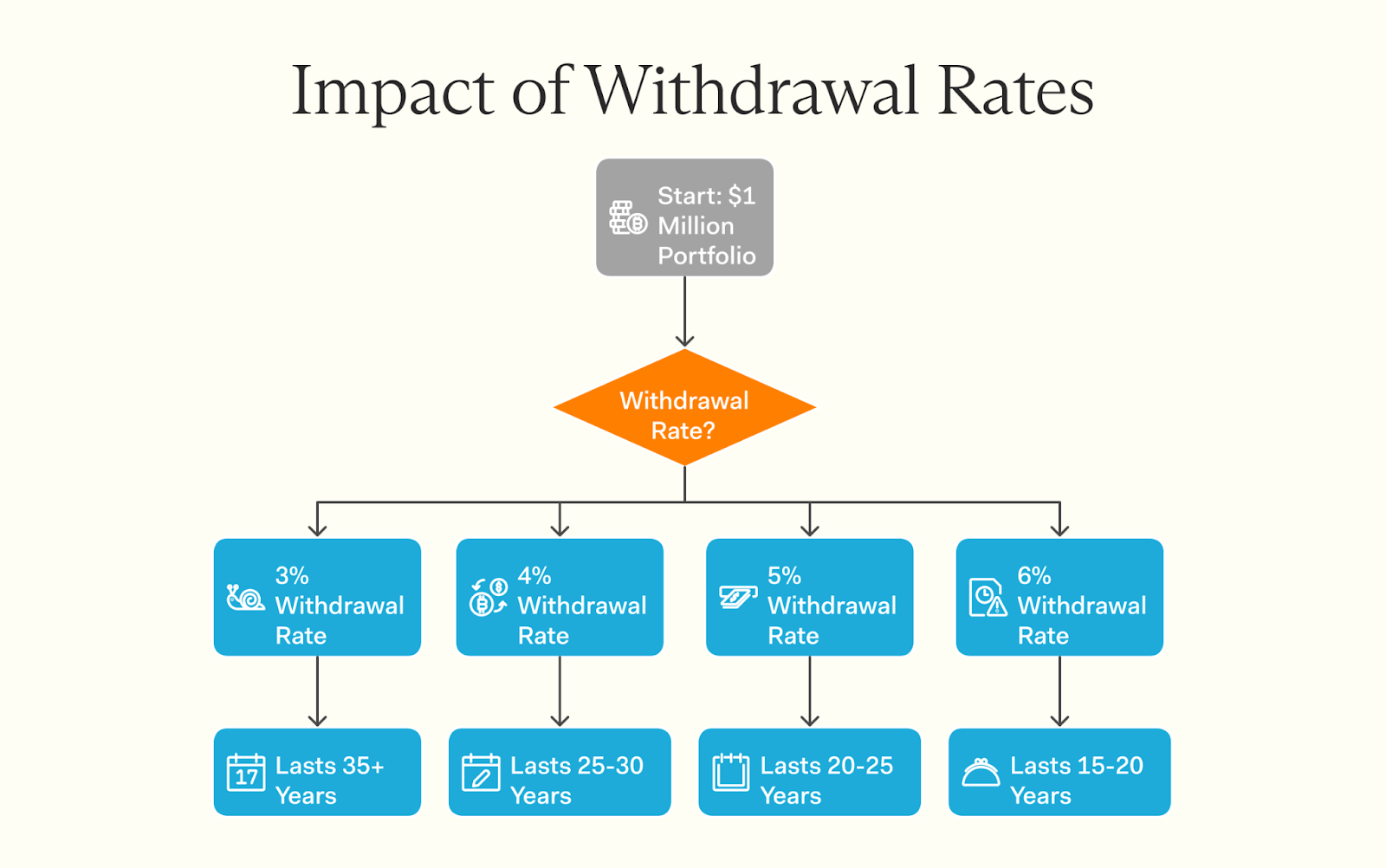

Use the 4% withdrawal rule cautiously

The 4% withdrawal rule advises withdrawing 4% of your retirement savings during the first year and then adjusting this amount for inflation in subsequent years. This principle might seem straightforward, but it involves complexities like market fluctuations.

Market volatility can change how much money your investments make over time.

If the market drops when you start withdrawing, it could hurt your account balance.

Consider adjusting that percentage based on your individual circumstances and market conditions. The average lifespan is longer these days, so you may need to stretch your funds further. It's advisable to think about health care costs too. They often rise as you age and can eat into your income benefit if you're not careful.

A balanced withdrawal strategy helps address longevity risk while keeping a good retirement budget in check.

Tools and Resources for Sustainable Retirement

For a steady retirement, consider tools like annuities for guaranteed income and long-term care insurance. They help protect your savings from unexpected costs. Tax-advantaged accounts can also boost your funds.

Annuities for guaranteed income

Annuities can provide guaranteed income in retirement. They are contracts with an insurance company. You pay a lump sum, and they promise to pay you back over time. This can help reduce the fear of outliving your retirement savings.

There are different types of annuities. Some offer fixed payments, while others vary with market performance. It's key to know what fits your needs best. Annuities often come with various fees, including mortality and expense risk charges, administrative fees, and investment management fees, which can vary significantly by the type of annuity and the insurance provider.

These tools can play a big part in managing long-term care costs or any unexpected expenses during retirement.

Long-term care insurance

Long-term care insurance helps pay for services you may need as you age. This includes help with daily tasks like bathing, eating, or dressing. Medicare provides limited coverage for long-term care services, majorly for short-term skilled nursing stays under certain conditions, and does not include custodial care.

Often, people face significant long-term care costs that can drain savings quickly.

Having this type of insurance can provide peace of mind. It ensures that your retirement savings don't vanish because of unexpected health needs. Today's workers should consider this option early to avoid a possible loss of funds later on.

With the right plan in place, you can focus more on enjoying your retirement rather than worrying about money issues related to healthcare.

Tax-advantaged retirement accounts

Tax-advantaged retirement accounts play a big role in your retirement planning. These accounts help you save money for the future while lowering your taxes.

Options like 401(k)s and IRAs offer traditional accounts where your money grows tax-deferred, and you pay taxes upon withdrawal. Alternatively, Roth 401(k)s and Roth IRAs use after-tax dollars for contributions but allow for tax-free withdrawals in retirement. Understanding these distinctions is crucial for effective retirement planning.

Saving early can significantly reduce the stress of outliving retirement savings later on. Keep this in mind as you plan for a secure retirement income!

Adjusting Your Lifestyle to Extend Savings

Cutting back on spending can help your savings last longer. Taking a part-time job during retirement might also boost your income, easing financial stress and keeping you active.

Reduce discretionary expenses

Discretionary expenses can drain your retirement savings fast. Start by cutting back on non-essential items—dining out, subscriptions, or expensive hobbies. Simple changes make a big difference.

Using a budget helps track your spending. Focus on needs over wants to save money. Put these extra funds into long-term care costs or growth investments. You'll have more security in retirement and less worry about outliving your savings.

Consider part-time work during retirement

Part-time work can help you stretch your retirement savings. Working beyond the full retirement age, which varies depending on your birth year (67 for those born in 1960 or later), can lead to increased Social Security payments and enhanced savings due to delayed retirement credits. Many retirees find that a small job keeps them active and brings in extra cash. This money can cover daily costs or fund fun activities, like vacations.

Working part-time might also ease some of your biggest fears about money running out. You'll keep your mind sharp and make new friends along the way. There are many options for part-time jobs; choose one that fits your interests and skills—like consulting in your field or working at a local shop.

Balancing work with leisure is key as you plan for a secure future.

Protect Your Retirement Savings from Inflation

Inflation can erode your purchasing power over time, making it essential to have a strategy in place. By diversifying investments, adjusting your withdrawal plan, and leveraging inflation-protected assets, you can safeguard your financial future.

Ready to strengthen your retirement plan?Speak with a Farther financial advisor today to explore the best strategies to combat inflation!

Conclusion

Retirement comes with risks—rising healthcare costs, market swings, and the challenge of making your savings last. But with the right strategies, you can take control. A smart spending plan, diversified investments, and careful withdrawal choices all help secure your financial future.

Small adjustments, like trimming expenses or exploring part-time work, can stretch your savings even further. The key is to plan ahead and take action now. Your retirement should be about enjoying life, not worrying about money—so start making moves today for a future you can feel confident about!

FAQs

1. What is the greatest fear people have about retirement?

The greatest retirement fear most people have is outliving their savings. This concern arises from uncertainty about long-term care costs, investment returns, and lifespan.

2. How can I determine my retirement date?

Your retirement date depends on multiple factors like your current age, savings amount, expected lifestyle including possible expenses such as a vacation home or long-term care costs.

3. Can a financial advisor help me with managing my retirement savings?

Yes! A financial advisor can provide valuable investment advice to ensure you don't outlive your funds.

4. Is there any way to manage withdrawals after retiring?

Effective management of withdrawals post-retirement is crucial for ensuring that your savings last longer. It's advisable to seek professional advice on this matter.

5. Will taking up a new challenge post-retirement affect my finances?

Taking up a new challenge post-retirement could indeed impact your finances - positively if it brings in additional income but also negatively if it involves significant expenditure.