August witnessed equity markets achieving fresh record highs, while fixed income securities also delivered positive returns for investors. This performance materialized despite ongoing concerns regarding trade policy, central bank autonomy, and technology sector dynamics. The month opened with U.S. tariffs taking effect on key trading partners following the conclusion of a 90-day implementation delay. Subsequently, a federal appeals court determined these "reciprocal tariffs" violated federal law, potentially setting up a Supreme Court review.

Mid-month volatility emerged as investors worried the Federal Reserve might maintain elevated rates longer to combat inflationary pressures. Recent inflation data, including the Producer Price Index, indicated businesses were starting to transfer tariff expenses to end consumers. Nevertheless, market optimism returned quickly thanks to encouraging corporate earnings reports and increased expectations for Fed rate reductions at the September policy meeting.

September 2025 represents the most consequential month for global capital markets since the pandemic recovery. With the Federal Reserve's September 17-18 meeting carrying an 89% probability of a 25 basis point rate cut and critical economic data releases clustered throughout the month, investors face unprecedented decision points that will shape portfolio positioning through year-end and beyond.¹

Our comprehensive analysis integrating the latest data from half a dozen leading asset managers and economists reveals a market at a critical inflection point where artificial intelligence investment sustainability, extreme valuations, and emerging dollar strength converge with traditional September seasonal weakness.

Markets opened September 2025 with immediate confirmation of seasonal weakness patterns, as the S&P 500 declined 0.7%, the NASDAQ fell 0.8%, and the Dow dropped 249 points (-0.5%) in the first trading session.² This decline occurred amid a global bond selloff driven by renewed inflation concerns and debt sustainability questions, with the 10-year Treasury yield holding steady at 4.22% while the 30-year approached 5%.³

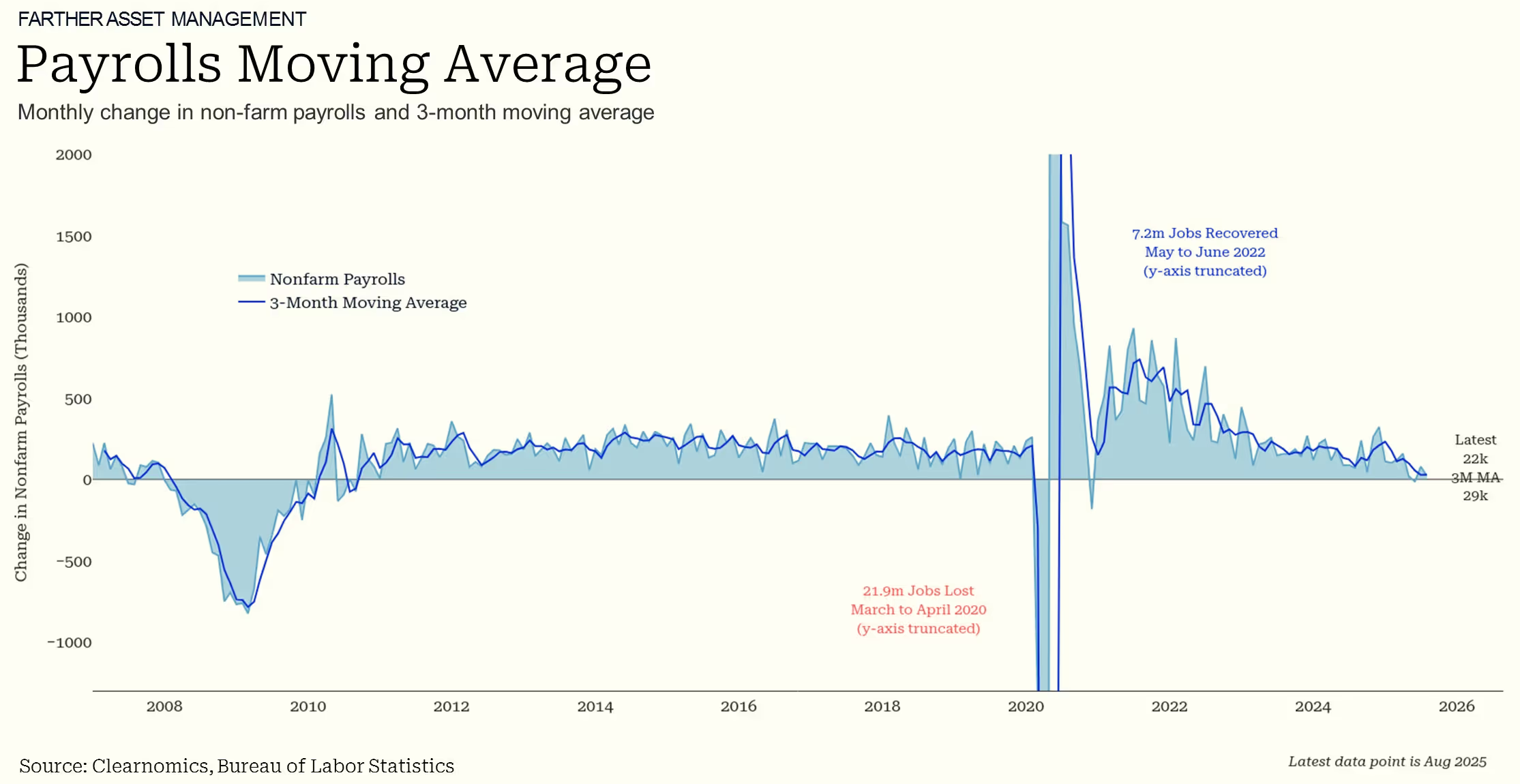

Economic indicators presented a mixed picture. Second-quarter GDP growth received an upward revision from 3.0% to 3.3%, representing a substantial recovery from the first quarter's 0.5% contraction. Conversely, the monthly employment report revealed a sharp drop in job creation, accompanied by significant downward adjustments to previous months' data. This development prompted the White House to dismiss the Bureau of Labor Statistics Commissioner, contributing to policy uncertainty.

Even with these headwinds, market volatility stayed relatively subdued compared to historical norms. August's robust gains across both equity and bond markets highlight the value of maintaining diversified, long-term investment approaches.

Key Market and Economic Drivers

- The S&P 500 advanced 1.9% in August, the Dow Jones Industrial Average climbed 3.2%, and the Nasdaq gained 1.6%. For the year, the S&P 500 has risen 9.8%, the Dow has increased 7.1%, and the Nasdaq has jumped 11.1%.

- The Bloomberg U.S. Aggregate Bond Index posted a 1.2% gain in August. The 10-year Treasury yield closed the month lower at 4.2%.

- International developed markets surged 4.1% in U.S. dollar terms via the MSCI EAFE index, while emerging markets rose 1.2% according to the MSCI EM index. Year-to-date, the MSCI EAFE index has risen 20.4%, and the MSCI EM index has increased 17.0%.

- The U.S. dollar index finished the month weaker at 97.8.

- Bitcoin declined in August, closing at 109,127 after suffering a "flash crash" on August 24.

- Gold prices reached a new record high of $3,487 by month-end.

- The Consumer Price Index increased 2.7% year-over-year in July, matching economist forecasts.

- The employment report revealed that only 73,000 new jobs were created in July. Major downward revisions to May and June data indicated the labor market was considerably weaker than initially reported. The unemployment rate held steady at 4.2%.

August Employment Report (September 6):

Only 22,000 jobs were added, versus the 75,000 expected, which was a significant disappointment. Additionally, unemployment rose to 4.3%, the highest level since October 2021. This represents a dramatic deterioration from already-weak July data. Additionally, US wholesale inflation unexpectedly declined in August for the first time in 4 months, adding to the case for the Federal Reserve to cut interest rates.

Strong earnings propelled market gains

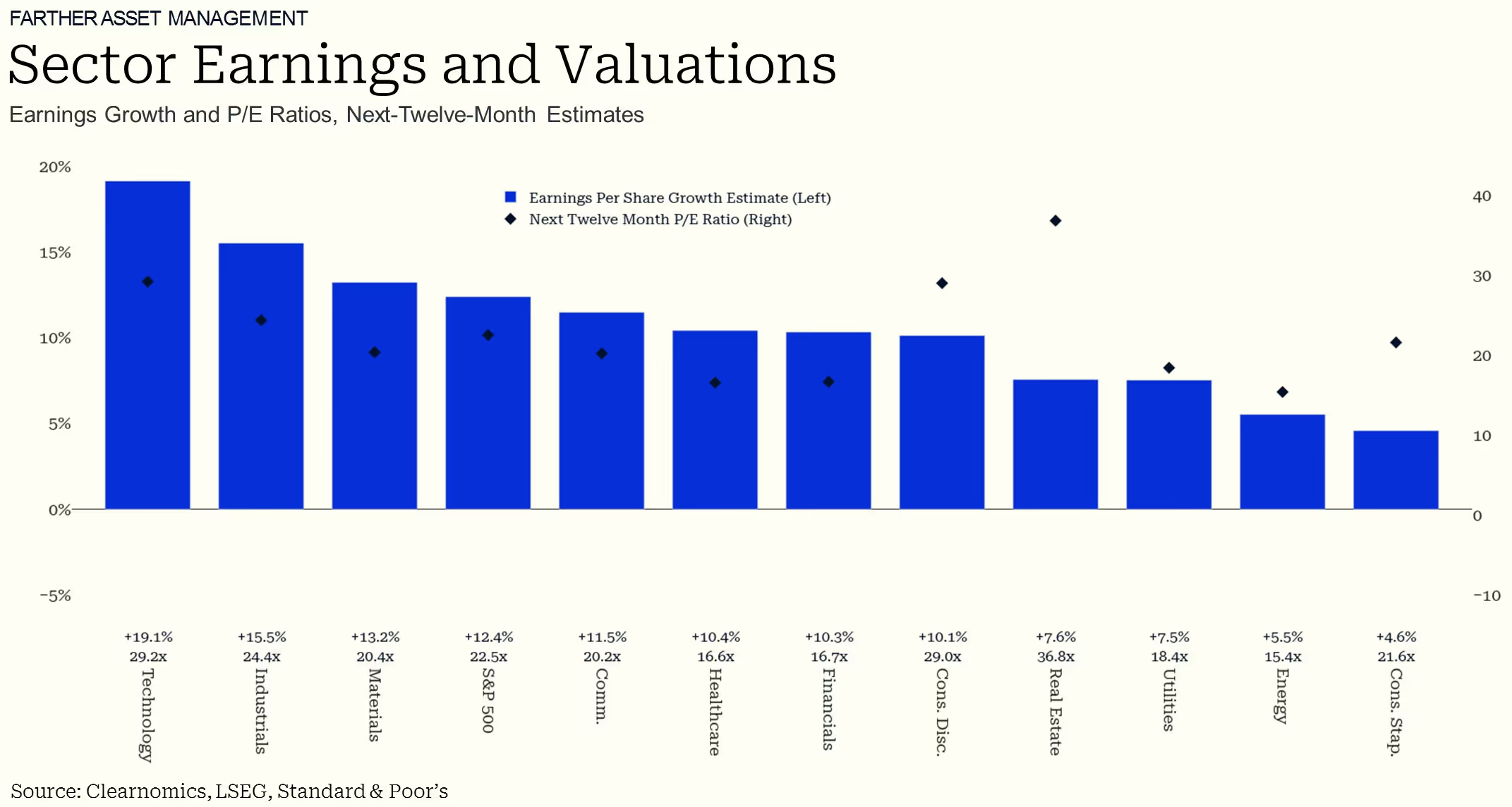

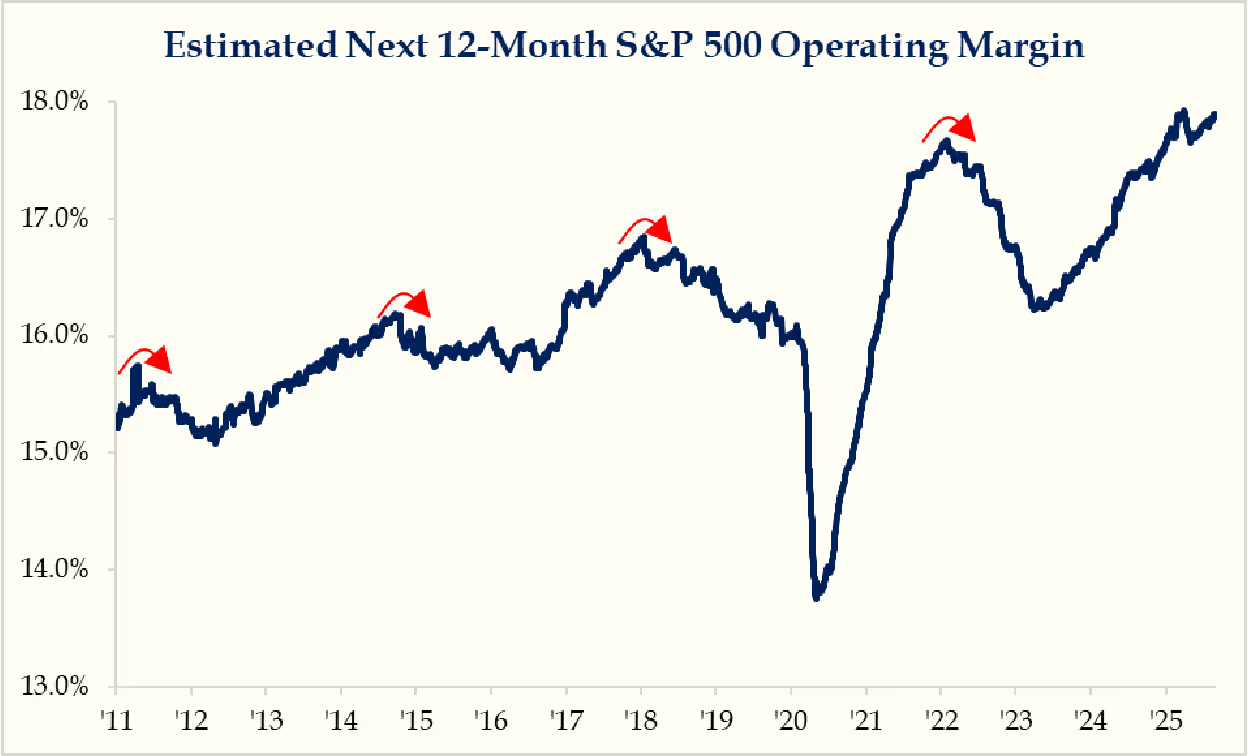

Although daily news cycles and headlines can influence short-term market movements, underlying fundamentals such as corporate profits and asset valuations ultimately determine long-term portfolio performance. While equity valuations remain elevated by historical measures, this is justified by companies demonstrating consistent earnings expansion.

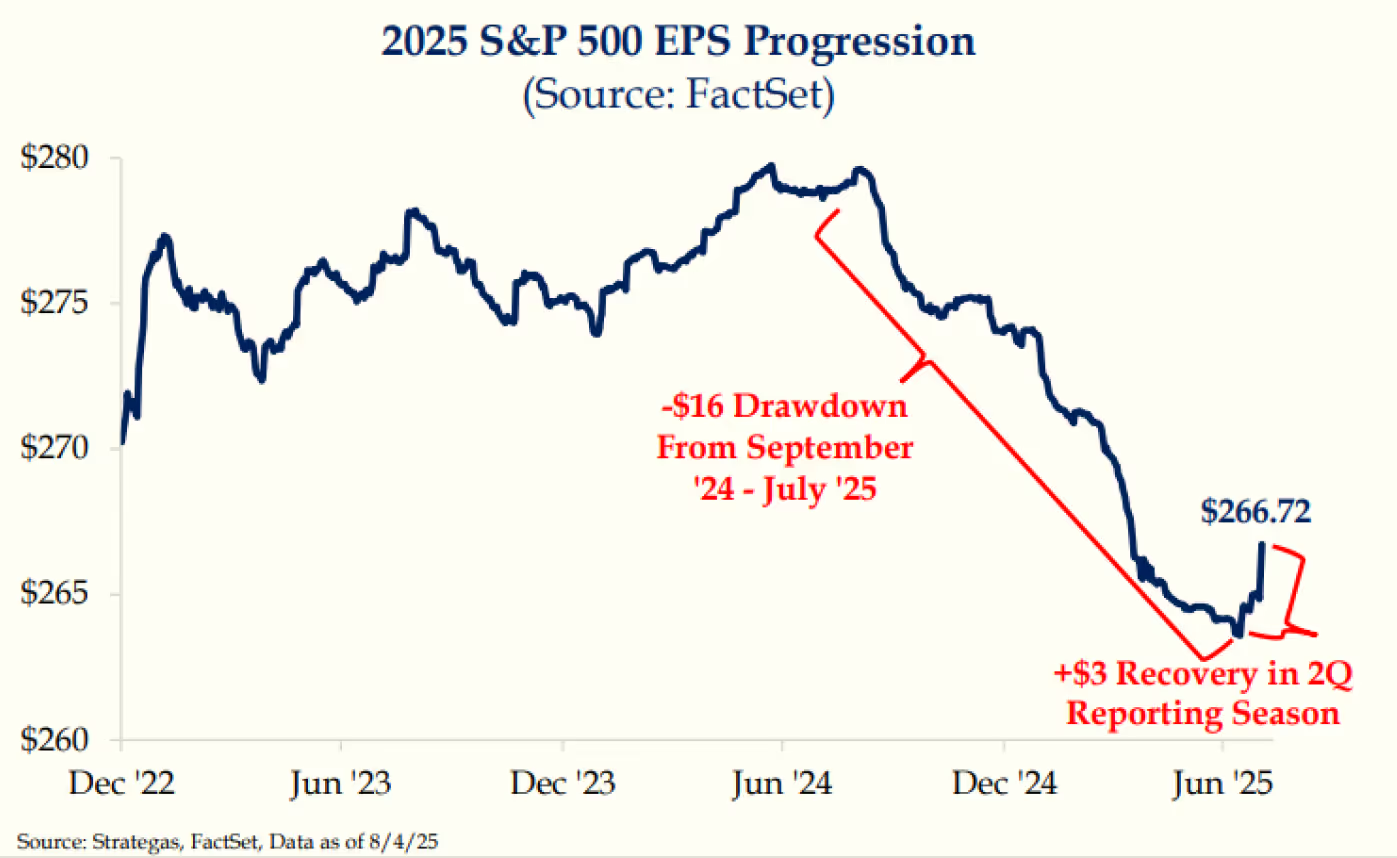

Recent quarterly earnings data reveal that 81% of S&P 500 firms exceeded analyst projections, as reported by FactSet. This represents the highest beat rate since Q3 2023, resulting in forward estimates being revised upwards.67 These results also highlight corporate resilience as businesses navigate tariff implementation, manage rising costs, and identify growth opportunities amid policy uncertainty.

Significant investor attention centers on the Magnificent 7, a collection of mega-cap technology companies, some with market values exceeding multiple trillion dollars. This group now comprises more than one-third of the S&P 500's total market capitalization, making their performance crucial for broader market direction. While earnings outcomes for this cohort were varied, several of these "hyperscalers" surpassed expectations. Despite ongoing "AI bubble" concerns, these positive results helped fuel a late-August market rally.

Fed signals rate reduction readiness

Meanwhile, consumer-oriented companies delivered varied results reflecting shifts in household spending behavior. Tariff implementation compounds these challenges as firms transfer an increasing share of trade costs to customers. Combined with disappointing employment data, markets began pricing in more aggressive rate cuts starting in September.

Fed Chair Jerome Powell delivered his clearest indication yet at the annual Jackson Hole conference that the central bank stands ready to resume interest rate reductions after this year's pause. The Federal Reserve operates under a "dual mandate" to maintain price stability and full employment. Recently, policymakers have maintained restrictive rates due to persistent inflation and robust labor conditions. Therefore, emerging signs of labor market weakness could shift Fed decision-making toward measured rate decreases.

Rate cuts may unlock cross-asset opportunities

Anticipated Fed rate reductions could generate opportunities across multiple asset categories. Beyond supporting broader economic expansion, lower borrowing costs can improve corporate financing conditions, reduce investment barriers, and enhance the present value of future earnings streams. For fixed income, declining rates increase the market value of existing bonds issued at higher coupon rates.

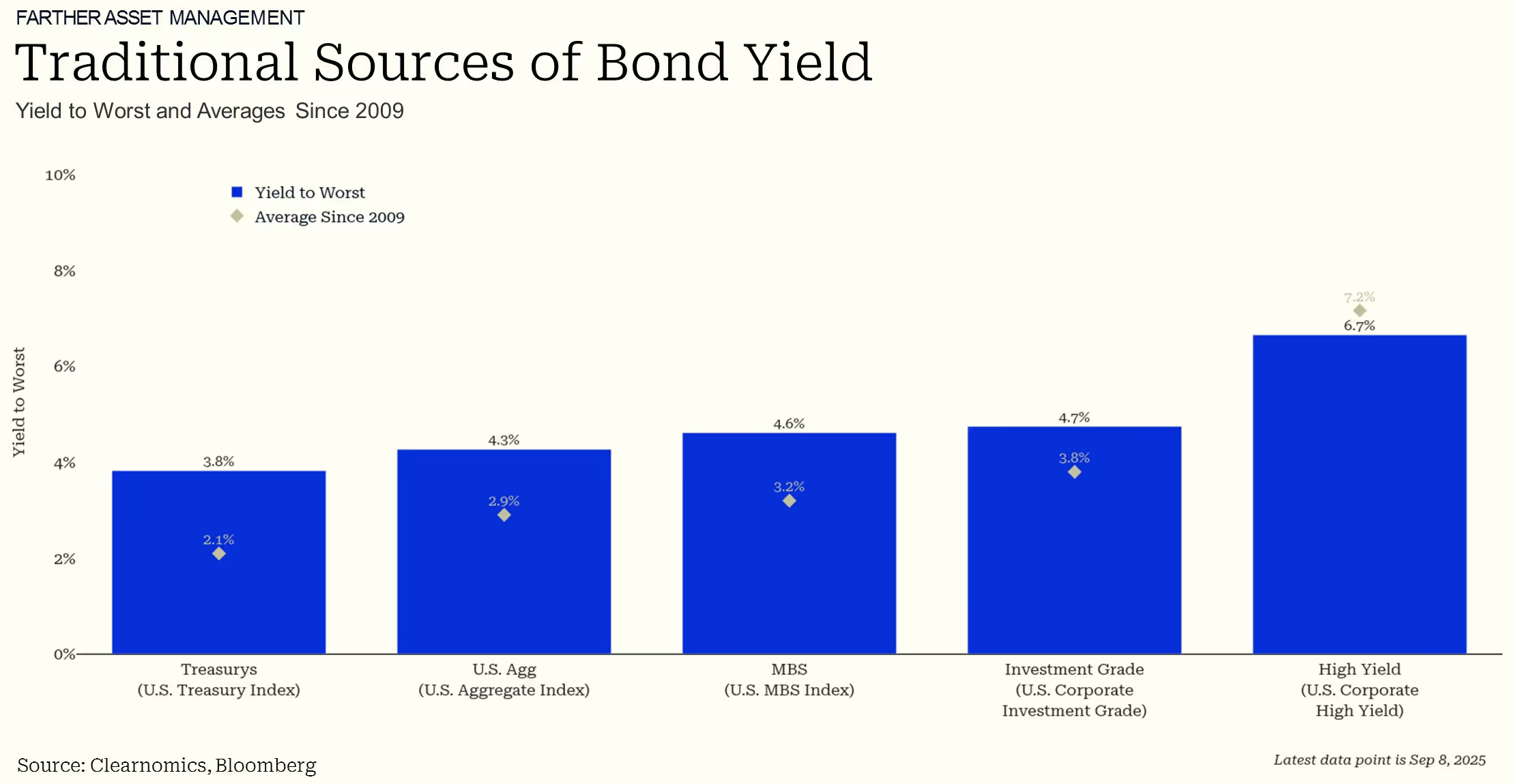

Bond yields have traded within a relatively tight band this year, with the 10-year Treasury generally oscillating between 4.0% and 4.5%. Even as short-term rates potentially decline through Fed action, numerous bond sectors continue offering attractive income levels. The U.S. aggregate bond index currently yields 4.4%, investment-grade corporate debt 4.9%, and high-yield securities 6.7%. These yields exceed long-term averages, providing a solid foundation for diversified portfolios.

For comprehensive portfolios, investors should maintain focus on balancing various risk and return factors. Issues including trade policy, monetary policy, and potential government funding disruptions represent just some of the challenges ahead. Rather than responding to individual events, maintaining portfolios capable of weathering volatility while delivering income and capital appreciation remains the optimal path toward financial objectives.

The bottom line? Markets achieved new record levels in August despite numerous policy uncertainties. While valuations remain demanding, robust earnings and economic fundamentals continue supporting portfolios through ongoing volatility.

Dollar Strength Thesis: Structural Factors Supporting Renewed Rally

Federal Reserve Independence and Policy Credibility

In general, currency strength plays a variety of critical roles. One of the most important aspects of investing is that when the dollar is strong, returns from international stocks and assets may be lowered once converted back to dollars, while a weak dollar can enhance returns from foreign investments.

Contrary to consensus expectations of continued dollar weakness, we identify multiple structural factors supporting dollar strengthening through year-end. The Federal Reserve's September rate cutting cycle, rather than weakening the dollar, may paradoxically strengthen it by demonstrating institutional independence and policy credibility amid political pressures.⁷

Key dollar strength catalysts include:

- Relative monetary policy advantage: While the Fed may cut 25 basis points, the European Central Bank and the Bank of Japan face more aggressive easing pressures

- AI infrastructure superiority: U.S. dominance in artificial intelligence investment creates sustained capital inflow requirements

- Energy independence dividend: Reduced oil import dependency provides structural current account support

- Safe haven demand: Geopolitical uncertainties drive capital toward U.S. Treasury markets despite rate cuts

The dollar's ability to maintain relative strength despite Fed easing expectations indicates underlying demand from international capital flows seeking AI investment exposure.

International Capital Flow Dynamics

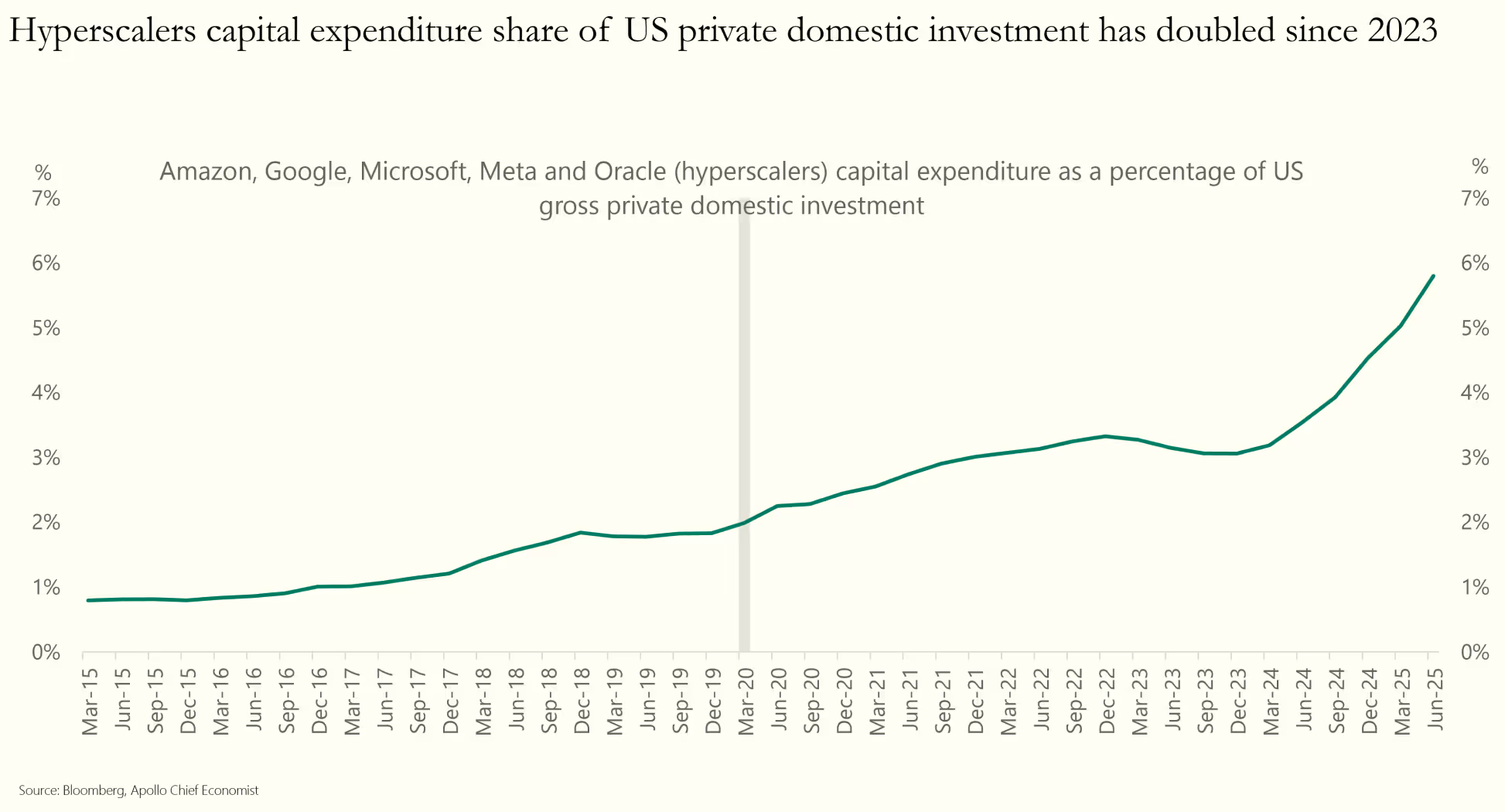

Artificial intelligence investment requires dollar-denominated funding, creating structural demand that transcends traditional interest rate differentials. With major technology companies planning $600 billion in annual infrastructure spending, international investors must acquire dollars to participate in the AI transformation.⁹

European and Asian central banks face more challenging economic conditions than the Federal Reserve, with the European Central Bank dealing with energy-related inflation persistence and the Bank of Japan managing ultra-loose policy normalization. These relative policy positions support dollar strength even as the Fed begins easing.¹⁰

Current Market Positioning:

Performance Analysis with Dollar Implications

International equity markets' 23.3% year-to-date outperformance (MSCI EAFE) and 19.6% gains (MSCI Emerging Markets) versus the S&P 500's 10.8% advance may prove vulnerable to dollar strength resumption.¹¹ Much of this outperformance stemmed from currency translation benefits that could reverse if dollar strengthening accelerates.

Small-cap rotation accelerated in August, with the Russell 2000 posting its best month of relative outperformance versus the S&P 500 in nine months, gaining 7.5% as rate cut expectations increased.¹² However, small-cap companies' typically higher domestic revenue exposure positions them favorably for dollar strength scenarios, as reduced import costs and competitive advantages versus international competitors boost profit margins.

Technology and AI Investment Analysis

Professional earnings analysis from FactSet confirms AI infrastructure investment remains the primary driver of U.S. economic growth, with Q2 2025 computer hardware investment surging 61% annualized and software investment rising 26%—the largest quarterly gain in 22 years.¹³ This investment concentration in U.S.-domiciled companies creates structural dollar demand that supports currency strength regardless of Federal Reserve policy.

Amazon, Google, Microsoft, and Meta have collectively doubled their annual infrastructure spending to an estimated $600 billion over the past two years.¹⁴ Even with this level of investment, we are still in the early stages of AI adoption.

Multi-Dimensional Valuation with Currency Support

These dollar strength scenarios may support current high U.S. equity valuations. The S&P 500's forward P/E ratio of 22.4 times becomes more reasonable if dollar strength reduces import costs and supports profit margins for domestic companies.⁵² Total U.S. corporate equity at 363% of GDP may prove sustainable if currency strength supports economic competitiveness.⁵³

Concentration risk in mega-cap technology companies could benefit from dollar strength, supporting international competitiveness and market share gains. International equity valuations at significant discounts may prove less attractive if dollar strength resumes, reducing currency translation benefits that supported recent outperformance.⁵⁵

Earnings and Profitability Analysis

U.S. corporate profit margins at 10.8% of GDP could expand further under dollar strength scenarios through reduced input costs and competitive advantages versus international competitors.⁵⁷ This contrasts with the March 2000 technology bubble comparison, as current profit elevation has structural rather than speculative foundations.⁵⁸

More impressive has been the structural growth in S&P profit margins from 15% to 18% since the Great Recession of 2007-2009, further supporting the case for higher multiples.59

Q2 2025 earnings growth of 11.9% driven by technology and communication services sectors gains additional sustainability under dollar strength scenarios, as U.S. companies maintain competitive moats in global markets.⁵⁹

Strategic Framework with Currency Considerations

Based on comprehensive analysis incorporating dollar strength expectations, we recommend a domestic-focused growth approach that emphasizes U.S. assets while selectively hedging international exposure.

Conclusion: Positioning for Dollar Strength Resumption

September 2025 represents a critical inflection point where dollar strength could emerge as a dominant theme, challenging consensus expectations of continued weakness. Analysis suggests that Federal Reserve policy independence, AI infrastructure advantages, and relative economic resilience create conditions for currency appreciation that could reshape global asset allocation strategies.

The dispersion among professional investment firms creates opportunities for investors positioned for dollar strength scenarios. Morgan Stanley's bullish equity outlook, combined with dollar appreciation, could generate superior returns for domestic-focused strategies. At the same time, Goldman Sachs' cautious economic view may prove overly pessimistic if currency strength supports economic competitiveness.

Key success factors for September positioning with dollar strength expectations:

- Domestic Focus: Emphasizing U.S. assets with limited international revenue exposure

- Currency Hedging: Maintaining international diversification through hedged instruments

- Quality Emphasis: Selecting companies with pricing power that benefit from reduced input costs

- Tactical Flexibility: Adapting to dollar strength signals from Fed communications and economic data

The month ahead will provide crucial signals about the sustainability of dollar strength, the effectiveness of Federal Reserve policy, and the market's ability to digest elevated valuations supported by currency advantages. Professional data sources suggest that while consensus expects dollar weakness, structural factors support appreciation that could drive superior domestic asset performance through year-end.

Investment themes for September and beyond emphasize dollar strength beneficiaries, maintaining strategic domestic overweight while using currency-hedged instruments for international diversification. This positioning capitalizes on U.S. economic exceptionalism while protecting against potential dollar volatility.

Footnotes:

1. Edward Jones Weekly Stock Market Update, September 1, 2025; CME FedWatch Data, September 2, 2025

2. Wall Street Journal, "Stocks Kick Off September on a Down Note," September 2, 2025

3. Bloomberg Terminal Data, September 2, 2025; FactSet Interest Rate Data

4. Bloomberg, "Morgan Stanley's Wilson Says US Stock Rally Has Further to Run," September 2, 2025

5. Goldman Sachs Research, Fed Rate Cut Forecast, August 2025; Reuters Poll Data

6. Citigroup Global Markets Analysis, August 31, 2025; BlackRock Weekly Commentary, August 2025

7. Federal Reserve Communications; New York Fed President Williams Statements, August 2025

8. Bloomberg Terminal Currency Data, September 2, 2025; FactSet FX Analytics

9. Edward Jones Analysis, Technology Infrastructure Investment, September 2025

10. European Central Bank Policy Assessment; Bank of Japan Communications, August 2025

11. MSCI Index Data via Bloomberg Terminal; FactSet International Equity Analytics

12. Russell Investment Analytics; Edward Jones Small Cap Analysis, August 2025

13. FactSet Earnings Insight, Q2 2025; Department of Commerce Investment Data

14. Edward Jones Technology Sector Analysis, September 2025

15. BlackRock Investment Institute, Fall Investment Directions 2025; Apollo, September 8, 2025

16. CME FedWatch Tool, September 2, 2025; Bloomberg Fed Probability Analytics

17. Goldman Sachs Research, "Why the Fed May Cut Rates Earlier than Expected," July 2025

18. Goldman Sachs Economics, Fed Forecast Update, August 2025

19. Morgan Stanley Research, Fed Independence Analysis, August 2025

20. Federal Reserve Bank of New York, President Williams Communications

21. Vanguard Market Perspectives, August 2025; Census Bureau Immigration Data

22. Bureau of Labor Statistics Benchmark Revision Preview; Reuters Employment Analysis

23. Bureau of Labor Statistics CPI Preview; Bloomberg Inflation Expectations

24. Morgan Stanley Research, Mike Wilson Strategy Commentary, September 2025

25. CNBC Interview, Mike Wilson, September 2, 2025

26. Morgan Stanley Small Cap Analysis, August 2025

27. MarketWatch, Morgan Stanley September Outlook, September 2, 2025

28. CNBC, "Morgan Stanley Names Stocks with More Upside," August 30, 2025

29. Goldman Sachs Research, Tariff Impact Analysis, March 2025

30. Goldman Sachs Economics, Trade Policy Assessment, August 2025

31. Goldman Sachs Research, Fed Policy Historical Analysis

32. Goldman Sachs Interest Rate Forecast, August 2025

33. BlackRock Investment Institute Weekly Commentary, August 2025

34. BlackRock, "Fed Rate Cuts & Potential Portfolio Implications," August 2025

35. BlackRock Fall Investment Directions, August 2025

36. iShares Investment Insights, Fall 2025 Outlook

37. Vanguard Economic and Market Outlook 2025, Global Summary

38. Vanguard Capital Markets Model, Long-term Return Projections

39. Vanguard Market Perspectives, Currency Analysis, August 2025

40. Vanguard Advisors, International Investment Strategy, August 2025

41. Citigroup Earnings Call Transcript, Q2 2025; Nasdaq Analysis

42. Investing.com, "Citi Expects Global Stocks to End 2025 Above Current Levels," June 2025

43. Citi Wealth 2025 Outlook, Sector Recommendations

44. Institute for Supply Management, Manufacturing PMI Preview; FactSet Economics

45. FactSet Manufacturing Sector Analysis, September 2025

46. Bureau of Labor Statistics JOLTS Preview; Bloomberg Employment Analytics

47. Department of Labor Employment Situation Preview; Reuters Survey

48. Bureau of Labor Statistics Annual Benchmark Revision Process

49. Bureau of Labor Statistics CPI Release Schedule; FactSet Inflation Analytics

50. Federal Reserve Board Meeting Schedule; Bloomberg Fed Coverage

51. Federal Reserve Chair Powell Press Conference Archive

52. FactSet Equity Valuation Analytics; S&P Index Characteristics

53. J.P. Morgan Asset Management, Weekly Market Recap, September 1, 2025

54. FactSet Index Analytics; Bloomberg Terminal Concentration Data

55. MSCI International Equity Analytics; Bloomberg Global Index Data

56. FactSet International Valuation Metrics; MSCI Regional Analysis

57. FactSet Earnings Analytics, Corporate Profit Margins; BEA Corporate Profits Data

58. Federal Reserve Economic Data (FRED), Historical Corporate Profits

59. Strategas, August 28, 2025

60. FactSet Earnings Insight, Q2 2025 Earnings Analysis

61. FactSet Valuation Models; Bloomberg Equity Risk Analytics

62. Federal Reserve Policy Effectiveness Studies; Academic Research Citations

63. Bloomberg Historical Seasonality Data; FactSet Calendar Analytics

64. Federal Reserve Independence Literature; Central Bank Credibility Studies

65. Technology Sector Investment Data; AI Infrastructure Spending Reports

66. Energy Information Administration Data; Current Account Balance Analysis

67. FactSet Earnings Insight PDF: https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_082925.pdf