Fed Trading Model

In 1997, Greenspan said in the Humprey Hawkins speech, “The decline of real (inflation-adjusted) long-term interest rates that has occurred in the last two decades has been associated with rising price-to-earnings ratios for stocks, real estate, and, in fact, all income-earnings assets. ”

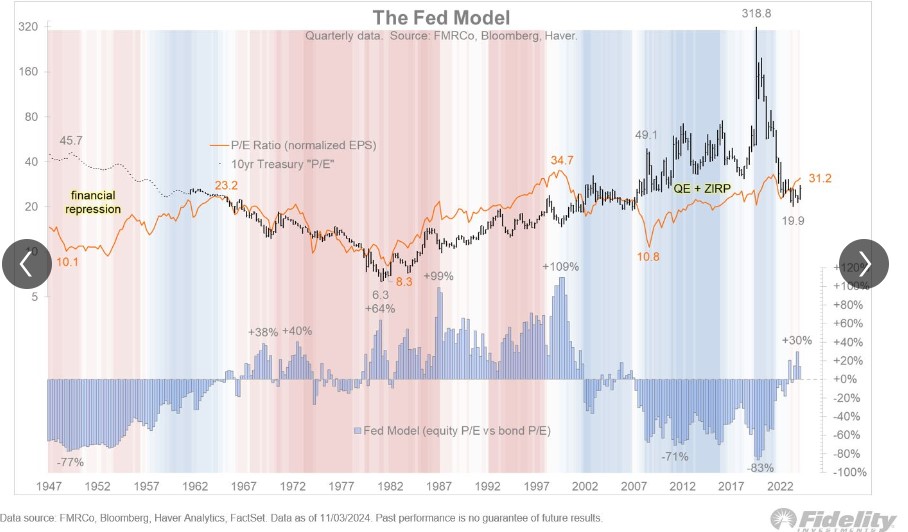

It became known as the “Fed model,” coined by Ed Yardeni. Over time, the model shows that the inverse of the stock PE ratio, aka the earnings yield, runs inversely to the Treasury PE ratio (the inverse of the Treasury yield).

When the equity PE ratio rises above the Treasury PE ratio, it is a period of high real rates of return. Conversely, when the PE ratio falls below that of the Treasury, long-term real rates of return decline. This version of the Fed model attempts to address the valuation of stocks and bonds relatively. But what the model misses is the Fed’s expectations of significant influence on real interest rates and asset valuations.

FedWatch created a “Fed trading model,” a systematic, AI-LLM driven model focused on the Fed expectations incorporated in the FedWatch RSI indicator to derive actionable, tactical weightings between stocks and bonds in 60/40 portfolios.