Outsourced CIO Model

In a ‘traditional’ Outsourced Chief Investment Officer (“OCIO”) model, the asset allocation takes on ‘standardized weightings.’ Stocks are around 55% to 70%, bonds 30% to 40%, and the remainder of 10% to 20% in alternatives.

Traditional asset-allocation theory, like mean-variance optimization, may be practical but lacks a focus on interest rate risk, which has become dominant in portfolios in recent years. Given the material effect of the change in Treasury yields on asset classes, the weightings of equity, bonds, and alternatives require interest rate risk adjustment.

Fed Watch indicators are an input to the asset allocation to finesse interest rate risk created in traditional equity-bond-alternatives portfolios:

*Risk-factor analysis of underlying interest rate risks in stock, bond, and alternative portfolio holdings.

*Interest rate risk analysis based on economic and Fed policy scenarios.

*Model portfolio analysis is specified for fixed-income and alternative fixed-income investments.

*Quantifiable input from the large language model-driven Fed Watch Index is used to derive optimized weightings of stocks, bonds, and alternative investments.

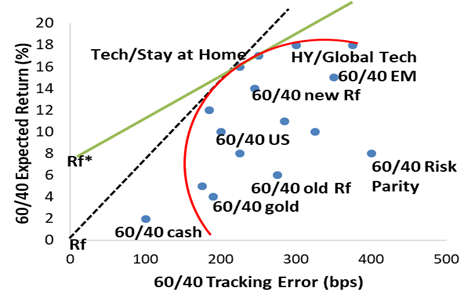

*Model portfolio research powered by Alladin, Bloomberg, Morningstar, and Ycharts that analyzes tracking error risk compared to expected returns and the alternate risk-free rate (Rf*, see graph below).

*Deep-dive, private credit loan portfolio analysis and research.

Efficient Frontier