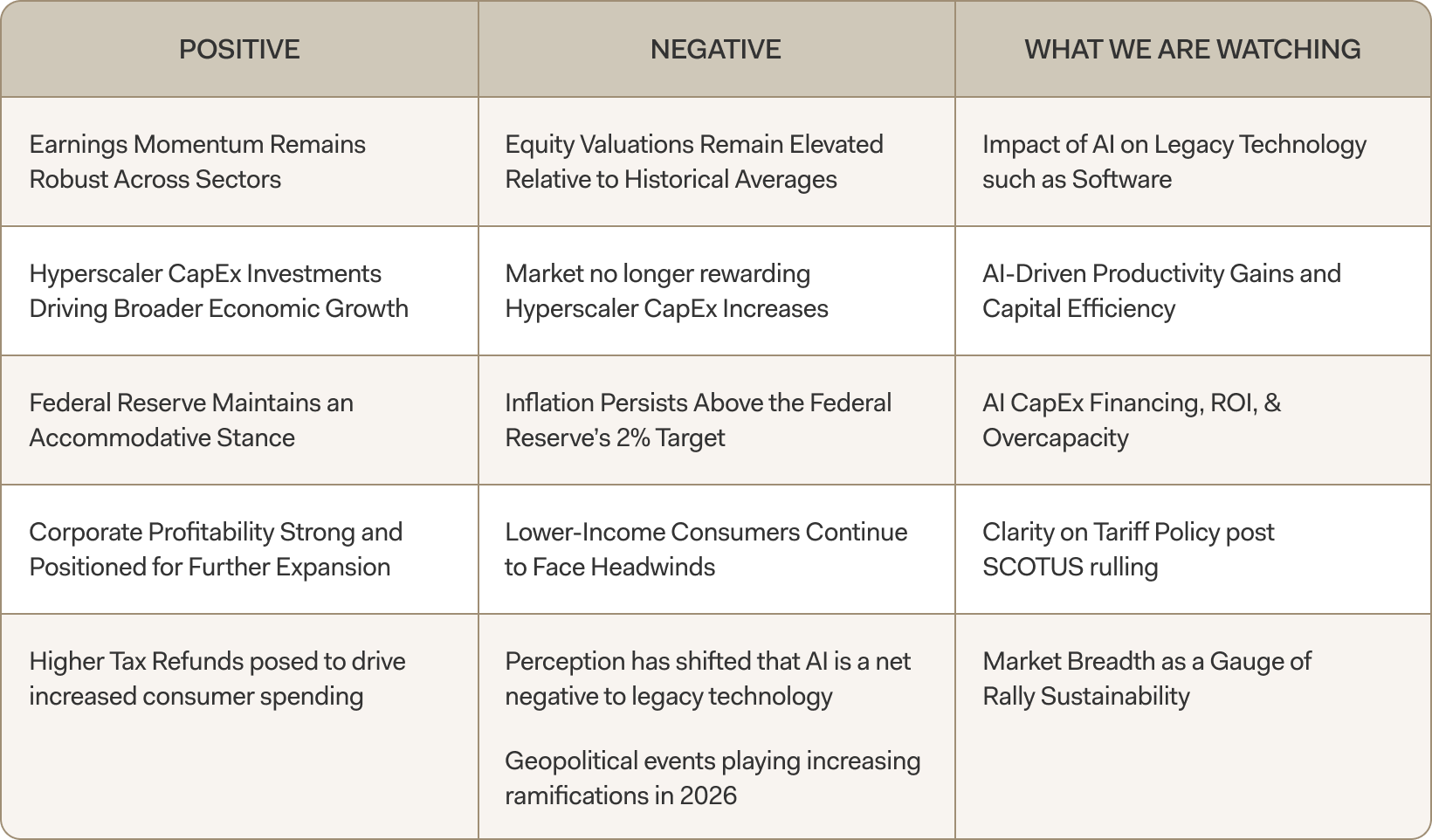

Executive Summary

February may have been the shortest month of the year, but it was far from uneventful. Between geopolitical shocks, AI disruption, tariff rulings, and sector rotation, markets are digesting a wide range of crosscurrents.

Football season may be over, but “Wildcard Weekend” seems alive and well in global markets – and this past month took that to a new level.

Last month, we highlighted the increasing frequency of geopolitical events unfolding over weekends — from the reported capture of Nicolás Maduro, to President Trump’s rhetoric toward the EU regarding Greenland, and a DOJ investigation involving Jerome Powell. The events of Saturday, February 28th, however, eclipsed them all.

At approximately 10:00 a.m. Tehran time, the U.S. and Israel launched coordinated air and missile strikes targeting ballistic missile sites, air defense systems, and command facilities in Tehran and Qom in an operation referred to as “Epic Fury.” Later that weekend, Iranian state sources confirmed the death of Ali Khamenei, along with dozens of senior leaders of the Islamic Republic.

What happens from here remains uncertain. Survey data from GAMAAN in 2024 suggested that only about 20% of the population supported the Islamic Republic1. That said, regime change is rarely straightforward. It is too early to determine whether remaining leadership — including the Revolutionary Guard — can consolidate power or whether an alternative government will emerge.

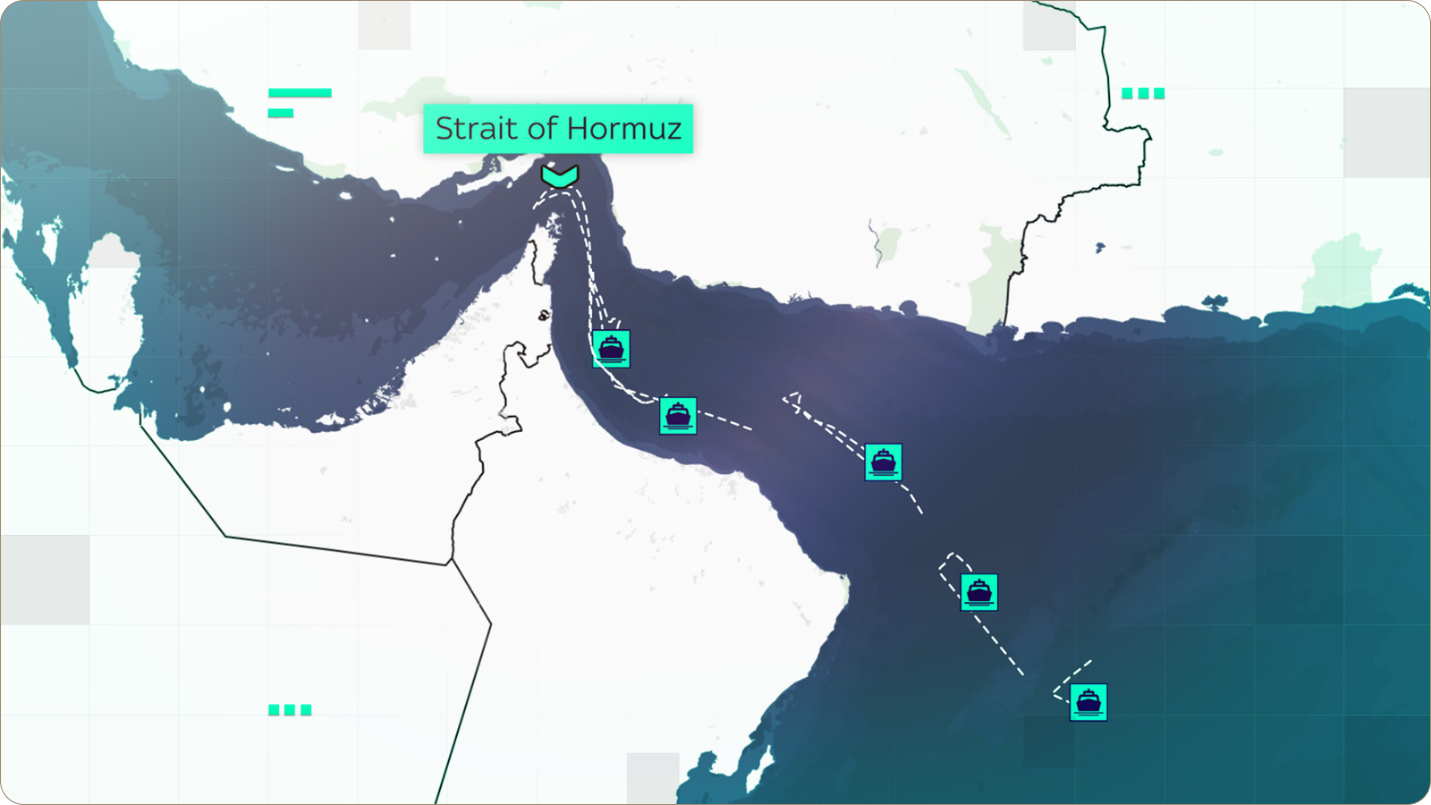

From a market perspective, the primary concern is oil. Iran accounts for 3–4% of global oil production. More importantly, its proximity to the Strait of Hormuz — through which approximately 30% of global seaborne oil and 20% of LNG supply transit — makes the region the most critical energy chokepoint in the world.2 Even a partial disruption could drive oil prices sharply higher and reintroduce global inflation pressures. As of this writing on March 8th, Iran has retaliated by shutting down traffic in the Strait of Hormuz, resulting in a spike of Brent crude to approximately $117 (+61% vs. February 27th close).

We generally advise against trading around geopolitical headlines. In a recent analysis by Goldman Sachs of seven major geopolitical shocks since 1950, the S&P 500 has historically dropped an average of 4% immediately following the event, but typically recovers within a month.3 However, a sustained rise in energy prices would have material implications for growth, inflation, and central bank policy, so we are monitoring developments closely.

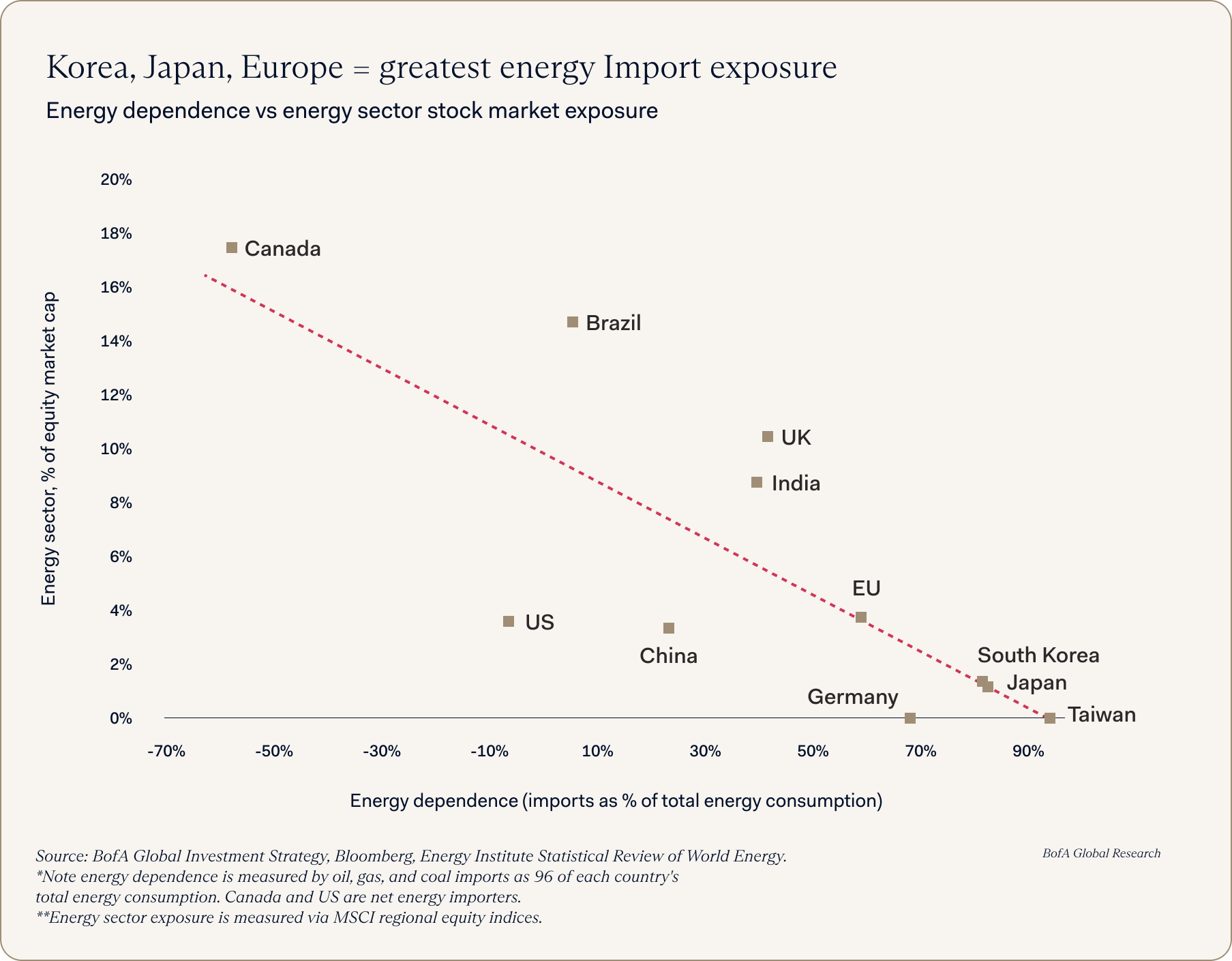

We find the below chart by BofA Global research particularly interesting, illustrating that South Korea, Japan, and Taiwan are most sensitive to energy dependence. As US oil production has roughly doubled to 13 million barrels per day over the past 25 years, the US economy has become meaningfully less sensitive to oil price spikes.

Brent Crude 2-day performance

The 2026 TACO (Trump Always Chickens Out) trade appears to be alive and well. In a CBS interview on March 9th, Trump said “I think the war is very complete, pretty much.” Following these comments, oil has plummeted 32% from the intraday high of $119.50 reached on the evening of March 8th.

As we have previously stated, we remain reluctant to make investment recommendations based solely on geopolitical events. The situation remains very fluid, with unprecedented volatility in the commodity markets. That said, history suggests that President Trump often views stock market performance as an important benchmark of his administration’s success.

SaaSpocalypse5

For years, software companies commanded premium valuations based on capital-light models, recurring revenue, and durable competitive advantages. The AI narrative, however, is shifting from growth accelerator to business model disruptor and, as a result, the correct valuations for SaaS businesses has been put into question.

The concern centers on whether AI agents — such as those introduced by Anthropic — can replace traditional software workflows. Two bear cases are emerging:

- AI replaces substantial portions of existing software demand.

- AI reduces headcount, thereby shrinking per-seat SaaS licensing models.

We view the first scenario as less likely in the near term. The second — pressure on seat-based pricing as organizations become leaner — is more plausible.

The selloff has been sharp and broad. The iShares Expanded Tech-Software Sector ETF is down 23% year-to-date. According to JPMorgan Chase, this represents the largest non-recessionary drawdown in software history, with nearly $2 trillion in market cap erased and software’s weighting in the S&P 500 falling from 12% to 8.4%.6

Software Index back to April 2025 Liberation Day lows

Importantly, not all companies will be affected equally. Some models face real disruption; others will adapt and potentially expand their total addressable markets. We are meeting with several technology-focused managers to identify businesses with high barriers to entry, durable cash flows, and leadership teams capable of integrating AI rather than being displaced by it.

AI and private markets

The ripple effects are extending into private equity and private credit, where software represents approximately 11% of the Bloomberg Leveraged Loan Index7. Many transactions were underwritten assuming high retention, rising ARR, and minimal disruption risk. Those assumptions are now being reassessed.

The risk is not uniform. Some managers have meaningful exposure to software refinancings at potentially unfavorable terms, while others are less exposed. We believe the indiscriminate nature of recent selling may ultimately create opportunities in select private equity managers and their respective strategies.

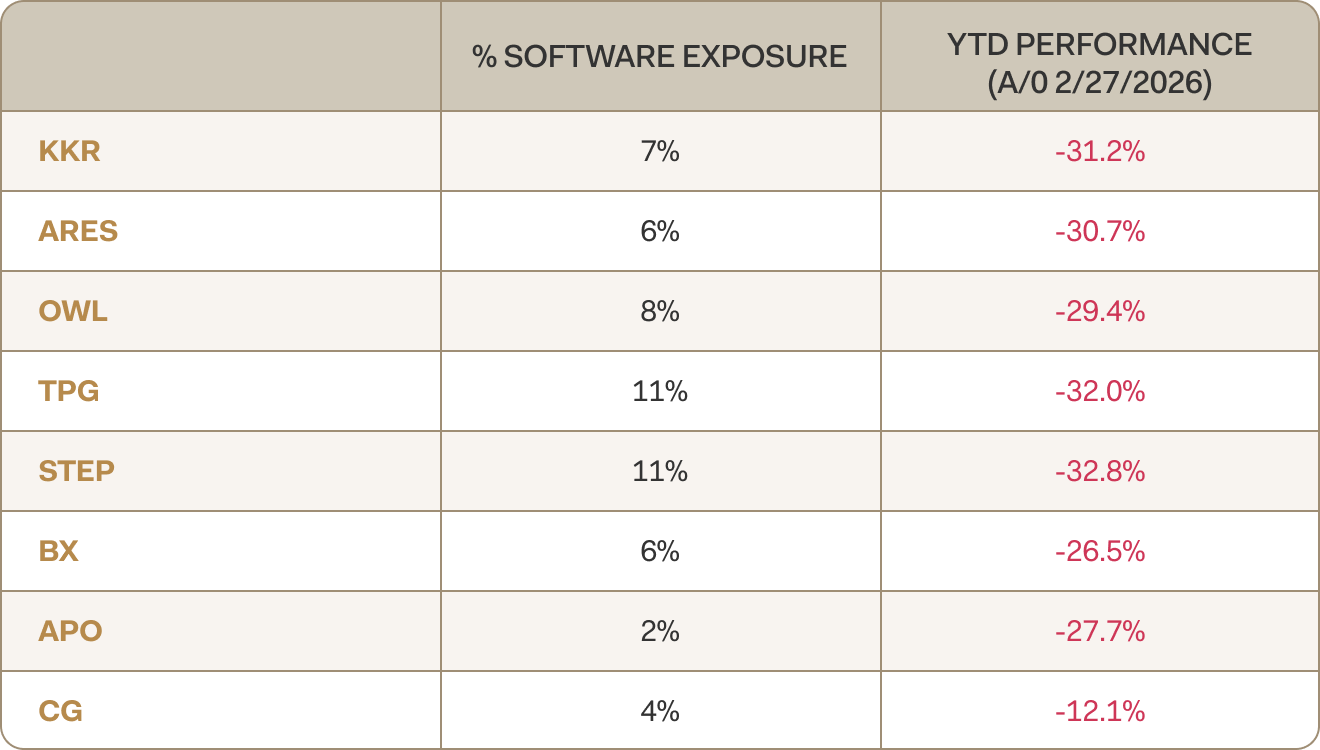

Alternative asset manager’s exposure to software

AI capital expenditures

One of the most notable developments this earnings season has been upward revisions to AI-related capital expenditures. Consensus expectations now call for +53% next-twelve-month growth, versus +38% one quarter ago. AI CapEx is projected to reach $750 billion by year-end 2026 — exceeding the combined CapEx of the rest of the S&P 500, which totals about $630 Billion.9

Interestingly, markets reacted negatively to this acceleration in spending. Investors are increasingly focused on free cash flow and demanding clearer returns on AI investments. Hyperscalers will face pressure to translate this spending into revenue and earnings growth.

At the same time, this level of investment represents a meaningful tailwind for the broader U.S. economy.

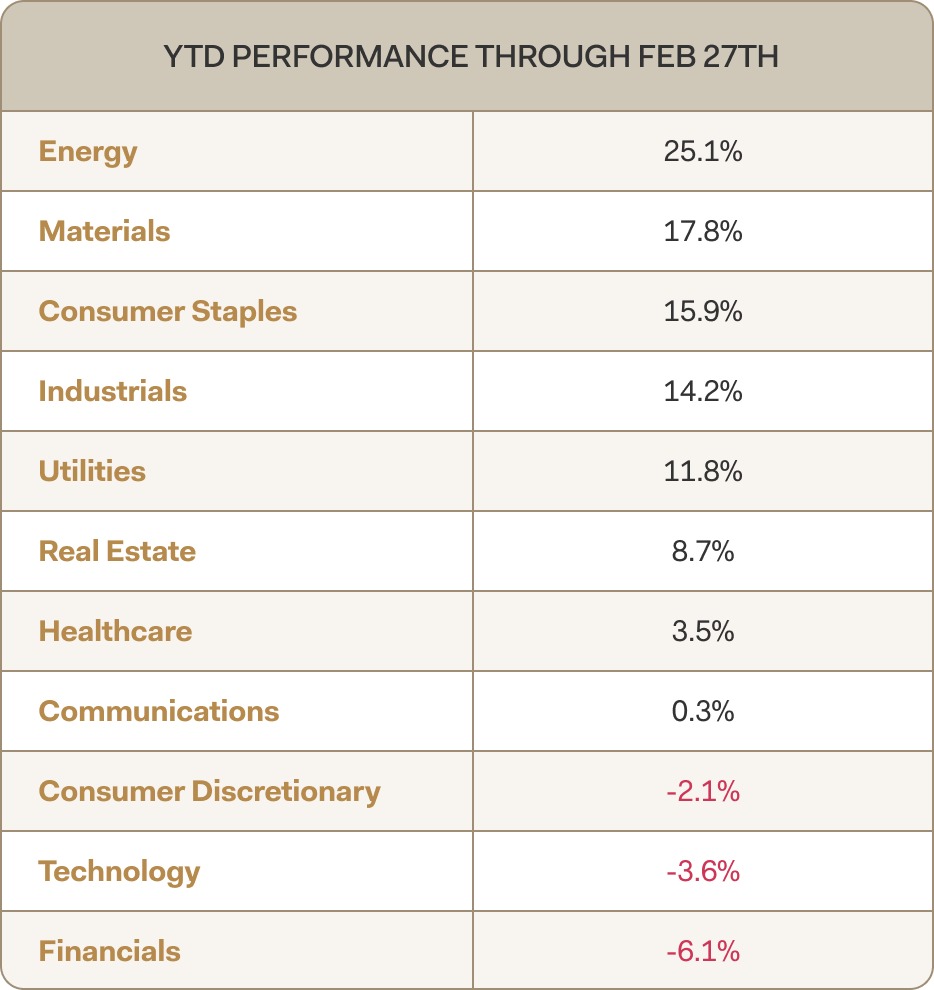

Defense wins championships

In what feels like a market homage to the defensive dominance of the Seattle Seahawks in their Super Bowl run, leadership has rotated. Technology and communications — last year’s leaders — have lagged year-to-date, while traditionally defensive sectors such as Utilities and Consumer Staples have outperformed. Energy remains the strongest sector, driven by geopolitical concerns.

Earnings remain a bright spot

Fourth quarter earnings have been solid. Approximately 75% of S&P 500 companies have reported:

- Revenue surprise: +1.6% (vs. 1.3% historical average)

- EPS surprise: +6.8% (vs. 4.4% historical average)

- 2025 EPS growth: +12% consensus

- 2026 EPS growth: +14% consensus

- Realized TTM EBIT margins: 18.3%10

If this momentum continues, elevated valuations may remain justified. Earnings ultimately drive markets, and profit growth continues to provide a supportive foundation even against a noisy macro backdrop.

Tariffs and the Supreme Court

As discussed in our 2026 outlook, the Supreme Court ruled on February 20th that President Trump’s use of the International Emergency Economic Powers Act exceeded constitutional authority, invalidating certain tariffs. What remains unclear is the disposition of previously collected tariff revenue and whether refunds will be required.

Within hours, President Trump issued a new 15% tariff under Section 122 authority. The legal and economic implications remain fluid. Notably, Justice Brett Kavanaugh suggested in dissent that alternative mechanisms for tariff authority may exist.

The markets responded with an initial “relief rally,” with retail, technology and automotive stocks seeing immediate spikes, along with European and Asian markets. The rally was short-lived as the administration moved to “Plan B,” and the market adjusted to reflect ongoing uncertainty.

Each of these updates reflects what we outlined in our 2026 market outlook: We expect 2026 to continue to be a year of uncertainty which will likely continue to drive heightened volatility in the markets. Diversified portfolios are built for uncertain times like this. Over the past several months, we have advocated for more defensive positioning.

As Warren Buffet says, “The future is never clear; you pay a very high price in the stock market for a cheery consensus. Uncertainty actually is the friend of the buyer of long-term values.”

We remain focused on discipline, valuation, and long-term fundamentals — while staying alert to the risks and opportunities emerging from this period of rapid change.

Thank you for your continued trust and support.

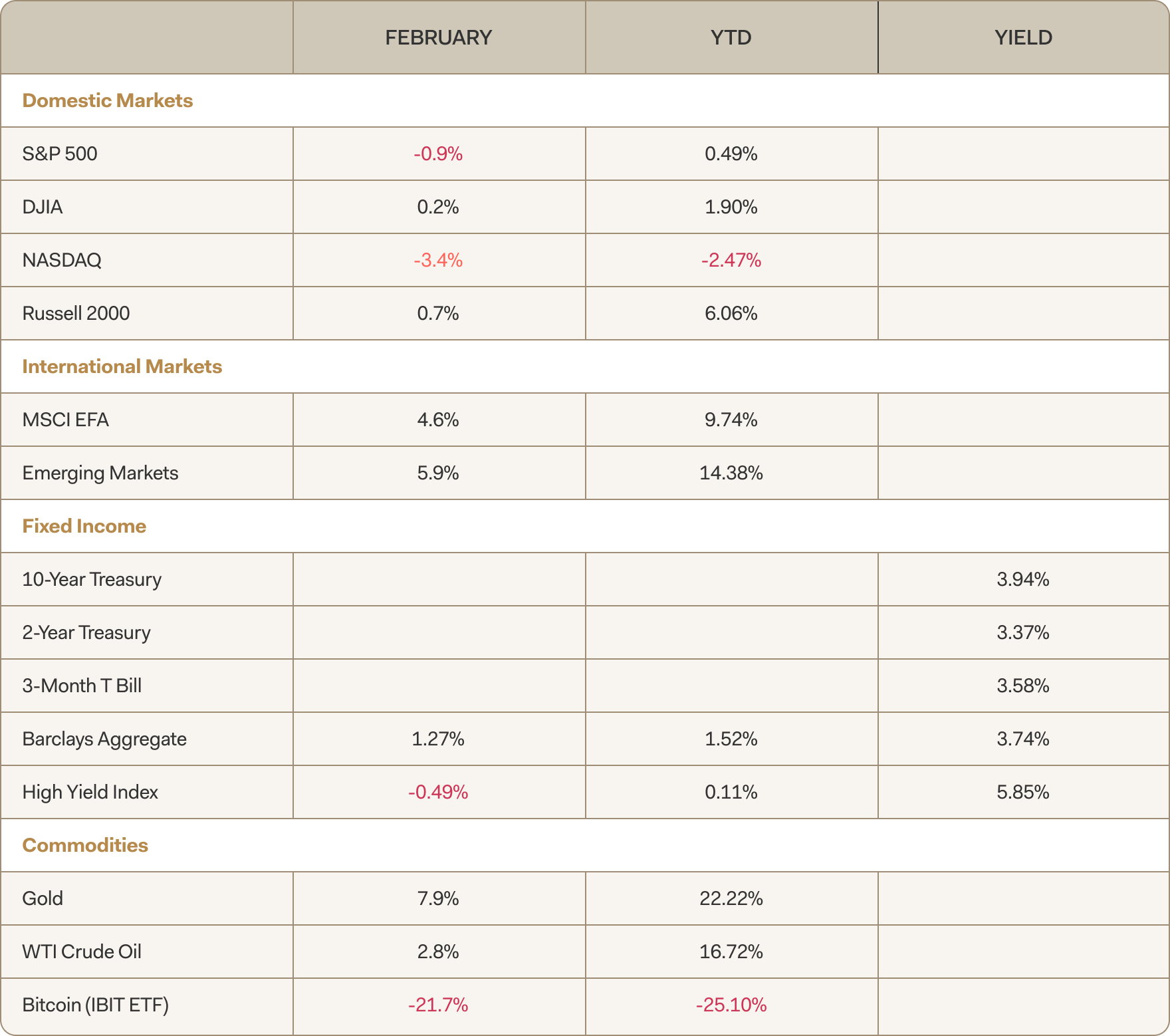

Farther Market Summary

All Performance Data is sourced from Bloomberg

All Performance Data included dividends

References

- Gamaan.org, August 20, 2025

- JP Morgan, March 2, 2026

- Goldman Sachs, March 6, 2025

- US Energy Information Administration (EIA)

- Jefferies analyst Jeffrey Favuzza coined phrase

- Boyar Research, February 12, 2026

- Strategas, February 25, 2026

- Goldman Sachs, February 6, 2026

- JP Morgan, February 17, 2026

- Morgan Stanley, February 17, 2026