A 529 is one of the most powerful tools available for funding your child’s education. Here’s how to use it to its full potential, including the rule changes most families haven’t heard about yet.

Most parents know a 529 exists. Fewer know how much flexibility it now offers. Since 2019, Congress has expanded what 529 funds can cover. Since 2024, unused balances can roll into a Roth IRA. And the FAFSA Simplification Act quietly removed one of the biggest drawbacks of grandparent-owned accounts.

If you opened a 529 and set a monthly contribution, that’s a strong start. This guide is about making sure every decision after that one is just as intentional.

What a 529 plan covers today

A 529 is a tax-advantaged investment account. Contributions grow tax-deferred, and withdrawals are completely tax-free when used for qualified education expenses. That category is broader than most people realize:

College and university costs

Tuition, fees, books, equipment, and computers. For students enrolled at least half-time, housing and food costs also qualify. This applies to any accredited college in the U.S. or abroad recognized by the U.S. Department of Education.

K-12 tuition

Up to $20,000 per beneficiary can be used annually on pre-college education expenses.

Apprenticeship programs

Fees, books, and equipment for programs registered with the U.S. Department of Labor are now covered, making for an important expansion for families whose children may pursue a trade or vocational path.

Student loan repayment

Up to $10,000 (lifetime limit per individual beneficiary) in federal or private student loans can be repaid using 529 funds, for the account beneficiary or a sibling.

What happens if you save more than you need

This is the question that holds many families back from contributing aggressively. The concern is reasonable: what if your child receives a scholarship, chooses a more affordable school, or takes a different path altogether?

The rules have changed enough that overfunding is far less of a constraint than it once was. Here are your options:

Change the beneficiary

You can transfer the account to any qualifying family member — a sibling, cousin, or even yourself — with no tax consequences. Unused funds from one child’s account can move seamlessly to another.

Repay student loans

If the beneficiary carries federal or private student loans, up to $10,000 in 529 funds can be applied tax-free. Siblings are also eligible for up to $10,000 each.

Roll unused funds into a Roth IRA

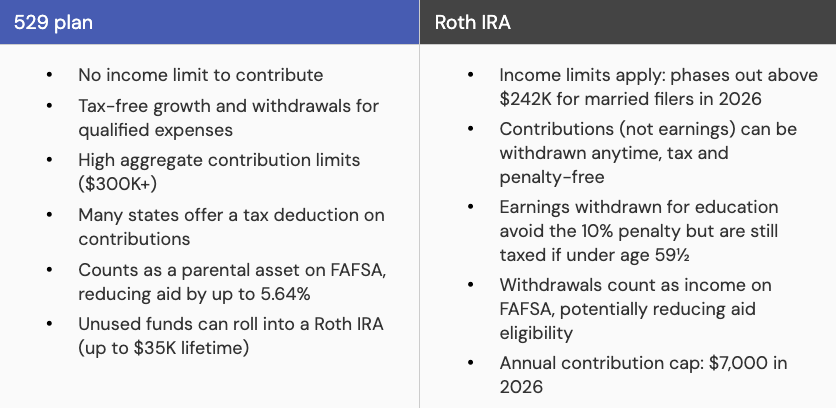

As of 20245, up to $35,000 in unused 529 funds can be rolled into a Roth IRA for the same beneficiary, tax and penalty free. Two conditions apply: the 529 must have been open for at least 15 years, and contributions made within the five years prior to the rollover date are ineligible. Rollovers are also subject to annual Roth IRA contribution limits ($7,000 in 2026), so the $35,000 transfers over multiple years rather than all at once.

The practical implication: a 529 opened at birth could be eligible for Roth rollover by the time your child is 15. Starting early doesn’t just give the account more time to grow. It opens up options that simply aren’t available to accounts opened later.

529 plans and Roth IRAs: how they work together

A common question is whether to use a 529 or a Roth IRA for education savings. For most families, this is less a competition and more a sequencing question.

The 529 is purpose-built for education. It offers higher effective contribution capacity and doesn’t compete with your retirement savings the way a Roth does. For families at or above the Roth IRA income phase-out threshold ($242,000 for married couples filing jointly in 2026), direct Roth contributions may not be available at all, making the 529 the primary tax-advantaged vehicle for education savings.

The stronger approach: use the 529 for education, protect the Roth for retirement, and know that if the two need to connect down the line, the rollover bridge now exists.

How grandparents can contribute to a 529 plan

If grandparents want to contribute to a grandchild’s education, a 529 is one of the most efficient vehicles available, and it doubles as an estate planning tool.

Grandparents can make a lump-sum contribution of up to five times the annual gift tax exclusion and elect to spread it over five years for gift tax purposes. In 2026, that means two grandparents could contribute up to $190,000 to a grandchild’s 529 ($19,000 x 5 years x 2 grandparents) without triggering gift tax. Those funds leave the grandparents’ estate immediately, yet if the grandparent is also the account owner, they retain full control and can access the funds if a health or financial need arises.

One important update: grandparent-owned 529 distributions used to count as student income on the FAFSA, which could significantly reduce aid eligibility. That changed with the FAFSA Simplification Act. As of the 2024-25 aid year, grandparent-owned 529 distributions no longer appear on the FAFSA at all, removing what was previously a meaningful strategic drawback.

How much to save for college

The College Board estimates the average all-in annual cost of a four-year private college at roughly $60,000 today. Projected forward at a 5 to 6 percent annual increase in education costs, a child born today could face $350,000 to $400,000 in total college costs by the time they enroll.

That figure becomes more manageable with a planning framework. A useful starting point: aim to cover approximately one-third of projected costs through the 529, one-third through income at the time of enrollment, and one-third through scholarships, grants, or aid. This isn’t a rigid formula. It’s a way of sizing the goal without needing to predict the future precisely.

Three things worth doing today

If you do not have a 529 open yet, open one. The 15-year clock for the Roth rollover provision starts from the date the account is opened, not the date you start contributing meaningfully. Starting early preserves options.

If you have a 529 but have not reviewed it recently, check your investment allocation. Age-based portfolios de-risk automatically as college approaches, but a static allocation chosen years ago may no longer reflect your timeline or goals.

If you are on track and want to go further, talk to your Advisor about superfunding, grandparent gifting strategy, or how 529 contributions fit alongside your broader tax and estate plan. These are the conversations where a well-built financial plan compounds its value.

Talk to a Farther Advisor

Education planning works best as part of a larger financial picture. A Farther Advisor can help you model how a 529 fits alongside your retirement, tax, and estate strategy, so every dollar is working as efficiently as possible.