- Markets Surged, but Volatility Returned Late in July

- Mega-Cap Growth Earnings Drove Gains

- Tariffs, Employment, and Fed in Focus

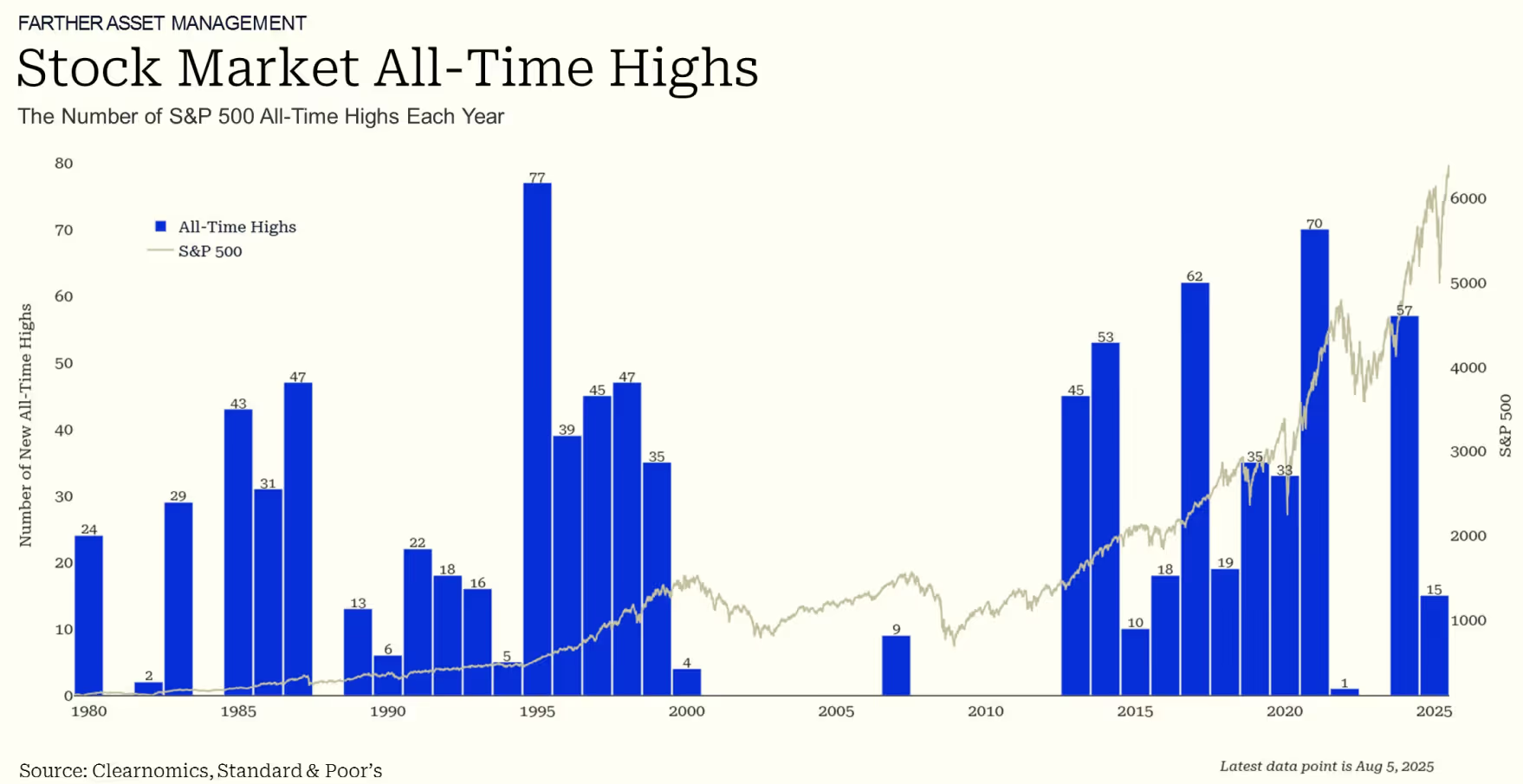

July delivered remarkable performance for equity markets, with the S&P 500 establishing ten fresh record highs throughout the month. Strong quarterly earnings reports, solid economic indicators, and successful trade negotiations before crucial tariff implementation dates drove this impressive rally. The index closed with six straight record finishes during the month's latter half, contributing to a robust 7.8% year-to-date advance for the S&P 500.

Yet market volatility and economic questions emerged as July concluded. President Trump's July 31 executive order announcing updated tariff schedules has sparked worries about potential consumer price increases. Furthermore, employment data from July indicated the job market had significantly deteriorated over the previous three months than initial reports suggested, resulting in a -2.34% retreat in the S&P 500 for the week of July 28th.

Given unfavorable seasonality, extremely optimistic sentiment, crowded positioning in growth stocks along with narrowing of the market participation, we anticipate increasing likelihood of market consolidation over the next few months. Recent months demonstrate how rapidly circumstances can shift within weeks, reinforcing why maintaining long-term investment focus remains the optimal approach for reaching financial objectives.

Market Performance and Economic Highlights1

- July returns showed the S&P 500 advancing 2.2%, while the Dow Jones Industrial Average posted a modest 0.1% gain and the Nasdaq climbed 3.7%.

- YTD, the S&P 500 has risen 7.8%, the Dow has gained 3.7%, and Nasdaq leads with a 9.4% increase.

- Fixed income markets saw the Bloomberg U.S. Aggregate Bond Index fall 0.3% during July. The benchmark 10-year Treasury yield edged higher, finishing the month at 4.38%.

- Global equity markets showed mixed results, with the MSCI EAFE developed markets index dropping 1.5% while the MSCI EM emerging markets index posted a 1.7% gain.

- Second quarter economic growth reached an annualized 3.0% pace, driven primarily by recovering business investment and import patterns influenced by tariff policies.

- The U.S. dollar index surprisingly recovered ground against bearish sentiment, climbing from 96.88 at June's close to 99.97 by July's end, though it remains notably lower for the year.

- Bitcoin achieved a new record peak of $120,198 mid-month before settling at $116,491 as July concluded.

- Gold prices maintained strength but remained below recent highs, closing the month at $3,293.

- Copper prices initially surged to record territory due to specific tariff measures, then plummeted 22% in the largest single-session decline as tariff measures were less than expected, as copper ore and copper concentrates were excluded.

- The Consumer Price Index increased 2.7% year-over-year in June, matching economic forecasts.

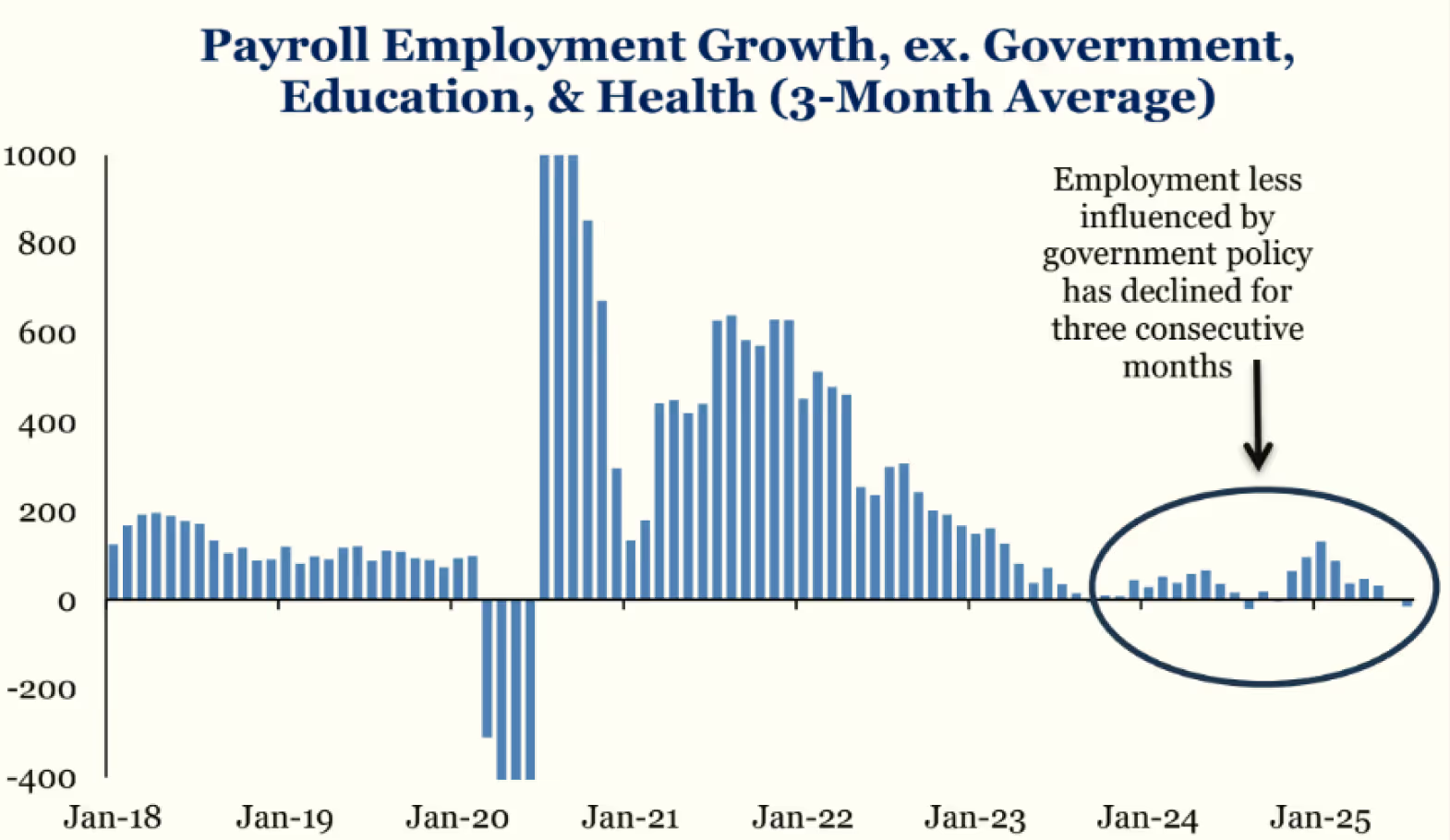

Employment growth slowed dramatically with just 73,000 jobs created in July. Major downward adjustments to May and June data of 258,000 revealed the labor market had been weaker than initially reported, though unemployment held steady at 4.2%. The three-month moving average now reflects only 35,000 new monthly positions, well below historical norms.2 The weak employment report resulted in the yield curve dropping approximately 20 basis points and the higher probability of a Fed rate cut in September.

Source: Strategas

Equity markets achieved multiple record levels

Second quarter earnings season, which began in July, continues to deliver positive surprises that have propelled markets to new heights. Although numerous companies have acknowledged some tariff-related impacts, these effects have not been uniformly detrimental. Among S&P 500 companies that have reported results, representing over one-third of the index, 80% exceeded earnings-per-share expectations. The combined earnings growth rate now stands at 6.4% annually, below recent quarters but surpassing Wall Street analyst projections.3

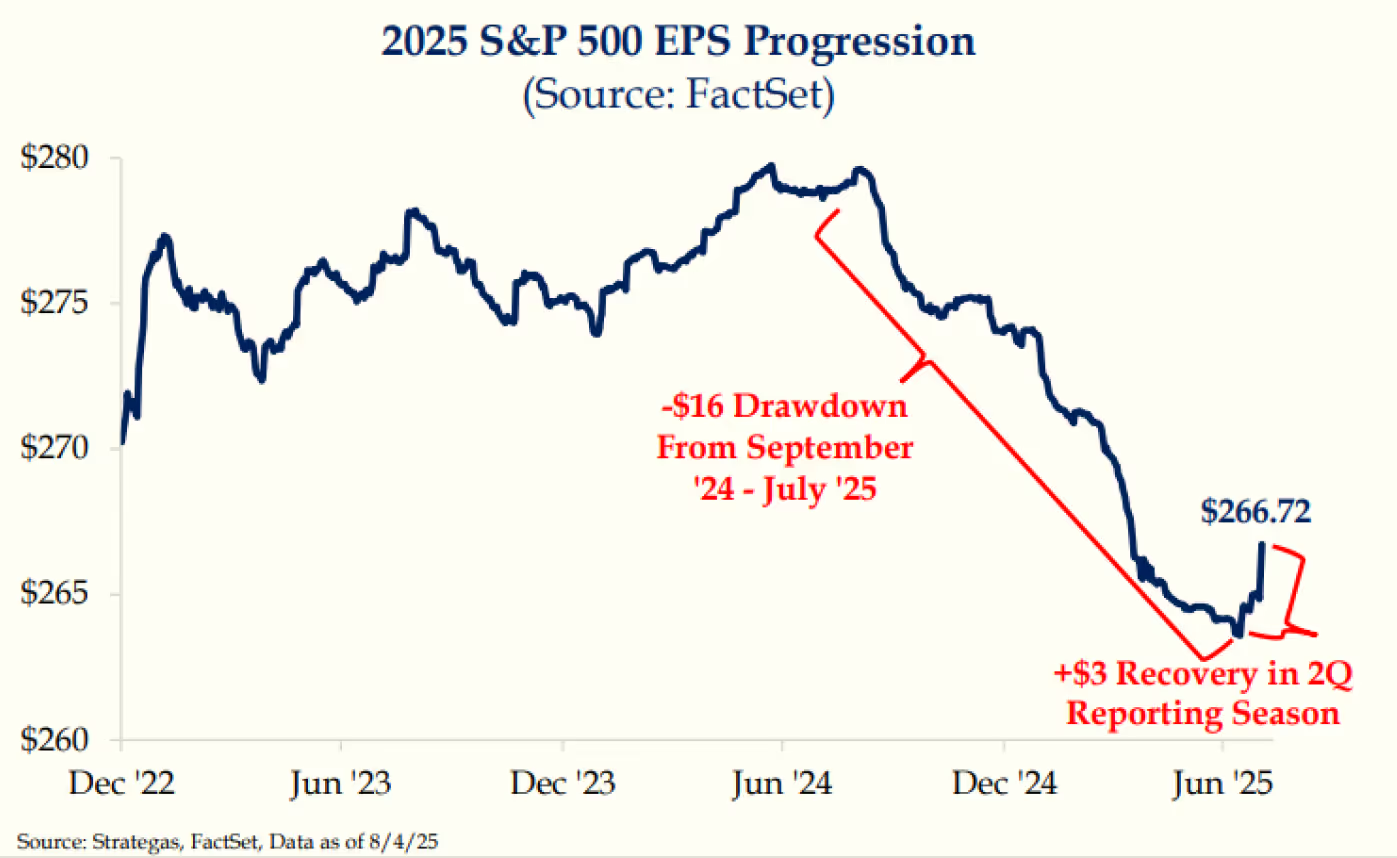

With 70% of S&P 500 companies having reported earnings, year-over-year blended sales growth is now 5.6% and earnings growth is 11.2%, up from 3.7% and 5.8%, respectively as of July 1st. Strong earnings have resulted in a $3 revision upward in CY25 Estimates to $267.4

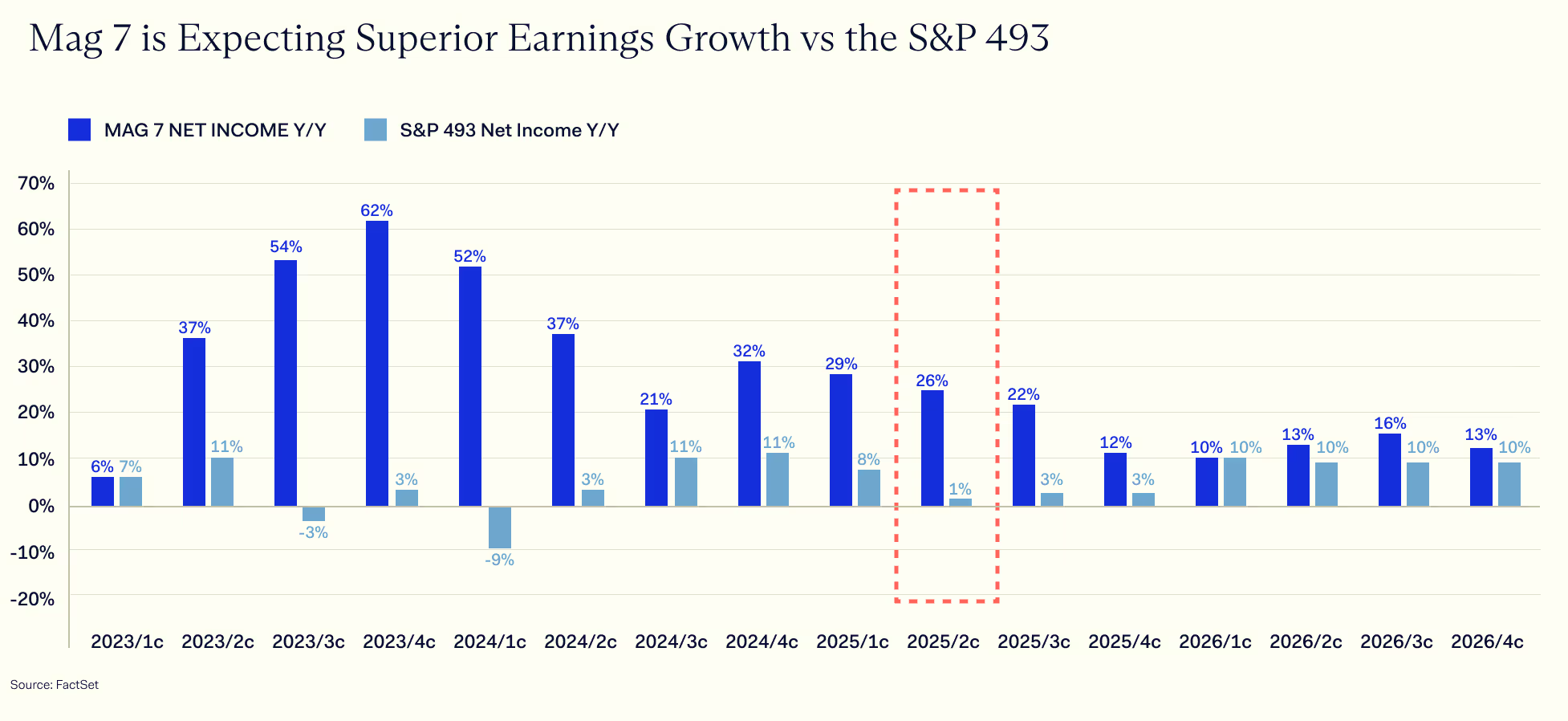

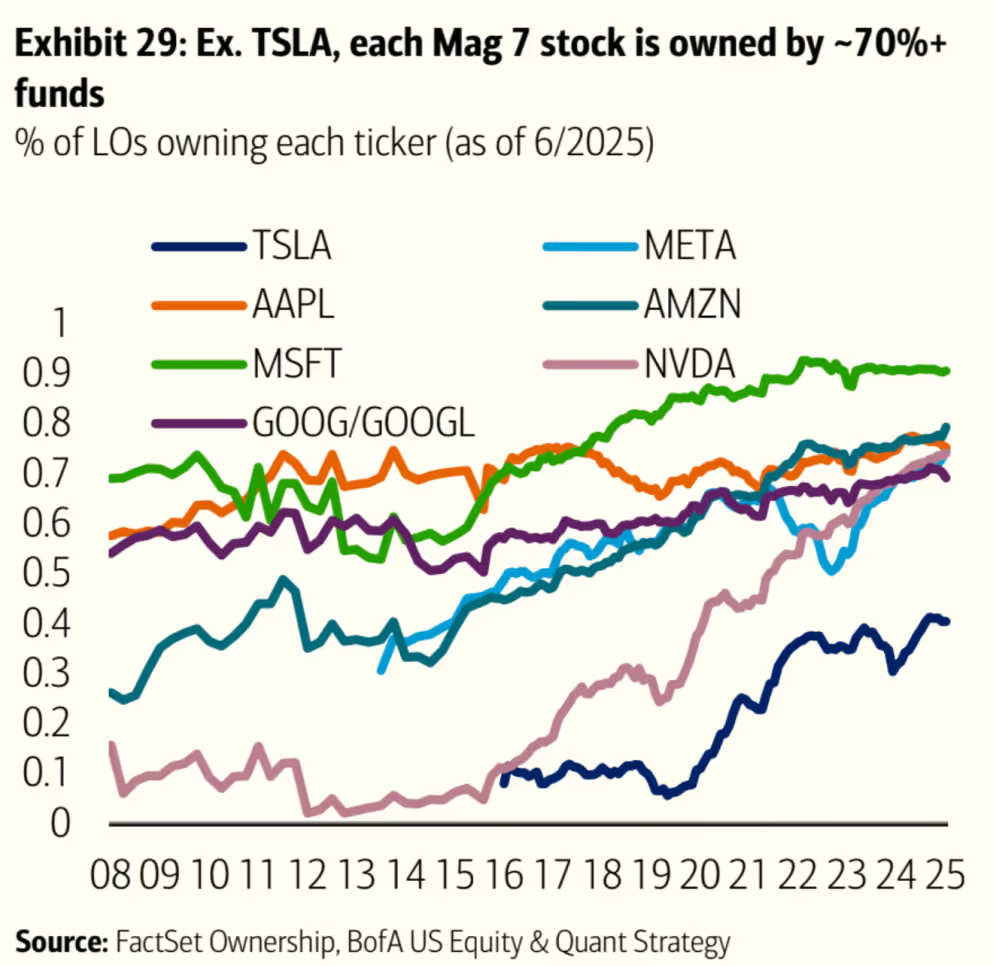

The Mag 7 has continued to lead earnings performance, due in part to artificial intelligence investments that have boosted operating results.5 Both Microsoft and Meta reported earnings that exceeded expectations, with AI playing a key role in improved performance; and Microsoft became the second company, alongside NVIDIA, to exceed a $4 trillion market valuation. In contrast, Tesla's disappointing second quarter results weighed on its share price.

While we maintain significant allocations to Mag-7 companies, we see two key risks to the sustainability of their outperformance:

- Exceptional financial results have led to narrowing of market participation, historically a signal of being in the later-stage of the market cycle

- The growing concentration of capital in Mag-7 stocks raises the question: who is the incremental buyer from here?6

Although technology stocks experienced significant volatility in 2025, the Information Technology sector has gained over 13% year-to-date, trailing only Industrials, which has delivered more than 15% returns.7 Meanwhile, Health Care and Consumer Discretionary sectors underperformed and posted negative returns.

Markets Monitor Trade Negotiations and Tariff Developments

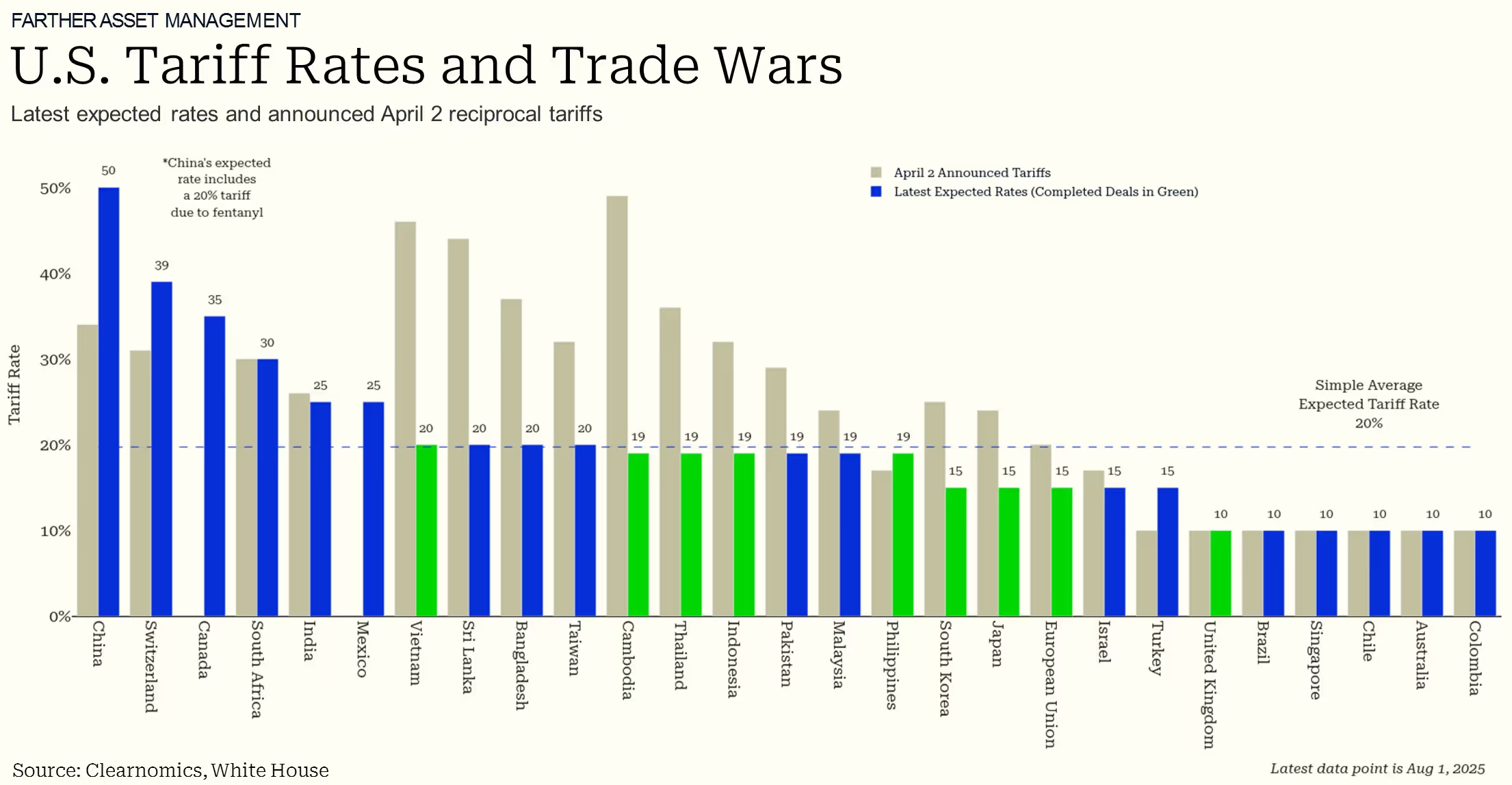

Throughout July, the administration announced multiple trade agreements, including arrangements with the European Union, Japan, and South Korea. Negotiations with China remain ongoing. While these agreements prevented the most severe scenarios many investors anticipated in April, numerous other countries still face potentially elevated rates as negotiation deadlines approach. President Trump's July 31st executive order established updated tariff schedules for various trading partners, effective August 7th (extending from the previous August 1st deadline), as illustrated in the above chart.

With the tariff negotiations nearing an end, positive trade announcements represent less of a driving force in future market upside. Risks remain in negotiated trading deals falling apart and consummation of final trade details.

According to the Yale Budget Lab estimates: as of July 23rd, consumers now face an overall effective tariff rate of 20.2%, representing the highest level since 1911. Thus far, companies appear to have absorbed much of this additional cost rather than transferring it to consumers. Whether this pattern continues depends on final tariff levels and companies' adaptive capabilities.

Trump Visits the Federal Reserve

In a moment that felt plucked from an episode of The Office, President Trump became only the second U.S. president in the past 50 years to visit the Federal Reserve — hard hat in hand. Ostensibly there to discuss cost overruns on the Fed’s building renovation, the visit’s true purpose was clear: to exert additional pressure on Chair Jerome Powell to cut interest rates. Traditionally, presidential visits signal support for the Fed Chair; this one did the opposite.

At the July 30th meeting, Powell maintained his stance that tariffs are inflationary and kept the federal funds rate at 4.25%, despite two dissenting votes. However, the latest employment report appears to contradict his recent press conference comments. We will be closely observing the Federal Reserve’s annual Jackson Hole Symposium from August 21st to 23rd — a forum where policy shifts are often signaled.

Source: NBC News

Congress Enacted Significant Tax and Cryptocurrency Measures

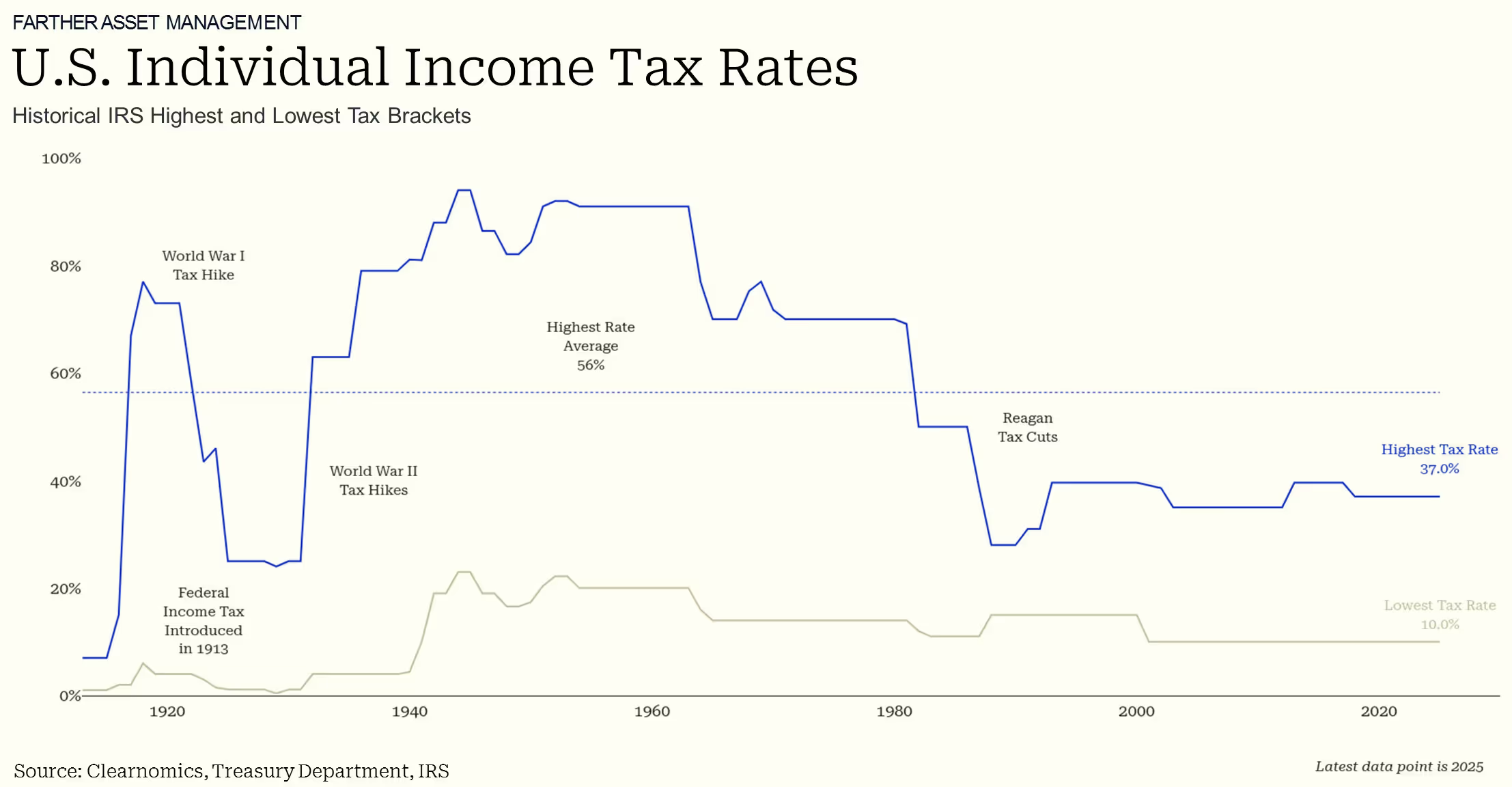

Bitcoin established new peaks in July as lawmakers deliberated cryptocurrency regulation legislation. The administration's perceived supportive stance toward broader cryptocurrency adoption has contributed to Bitcoin's 2025 gains. Additionally, the recently enacted GENIUS Act addresses stablecoin regulation, focusing on digital currencies typically linked to the U.S. dollar.President Trump signed comprehensive tax and spending legislation on July 4th, making numerous Tax Cuts and Jobs Act provisions permanent, including existing tax rates and income brackets. This legislation provides investors with greater certainty by preserving the current low-tax framework, though it raises questions about the expanding national debt's long-term sustainability.

The Congressional Budget Office projects the legislation will increase the national debt by over $3 trillion during the next decade. Although the bill included spending reductions for major programs, these cuts were exceeded by tax revenue decreases.

Making these tax provisions permanent eliminates uncertainty that had influenced long-term financial planning, as many TCJA components were set to expire this year. This stability could encourage business investment and consumer spending in the immediate future.

The Bottom Line

Markets established numerous records during a turbulent month featuring tariff volatility, new tax legislation, and earnings reports. However, the strength of the economy, a Federal Reserve late to action, and an end to the business cycle came into focus with the July employment report. Trade developments and corporate earnings will continue capturing investor attention in August until the Federal Reserve Symposium in Jackson Hole at the end of the month.

Sources

- Bloomberg

- Strategas, August 4

- https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_072525.pdf

- Strategas, August 4

- Morgan Stanley, August 4

- BofA Securities, August 1

- Bloomberg