2022 Economic Review

2022 was an eventful year.

Inflation and the central bank policy responses to combat it dominated business headlines. Stock and bond markets around the world experienced bear markets. The Omicron variant of Covid resulted in a U.S. slowdown to start 2022 and a tight zero-Covid policy from China throughout much of the year.

The combination of rising interest rates and the Omicron slowdown caused concerns over whether the U.S. was in a recession during H1. And the war in Ukraine exacerbated energy and food inflation, while continuing to bear an enormous toll on the citizens of Ukraine.

Rising inflation in the U.S. and the Federal Reserve’s response to it dominated U.S. financial markets. Inflation in the U.S. returned with a vengeance: fanned by the 2020 and 2021 fiscal stimulus packages and the Federal Reserve’s easy monetary policy through March of 2022. The war in Ukraine acted as lighter fluid on the fire – leading to a rapid spike in energy and food inflation, as Russian energy was embargoed and food from Ukraine became difficult to export.

U.S. Consumer inflation peaked at 9.1% in June. And the Federal Reserve issued a series of short-term interest rate hikes throughout the year: a small 0.25% increase in March, a 0.50% increase in May, and an accelerated pace of hikes in June with 4 consecutive 0.75% increases, before slowing to 0.50% at its last meeting in December. For perspective, it is important to note that the Federal Reserve raised the overnight federal funds rate from 0.25% to 4.50% in only 9 months.

Federal Reserve Chairman Jerome Powell has indicated that the Federal Reserve will aggressively pursue its mandate to fight inflation – raising short-term rates high enough and maintaining them for a sufficient duration – even at the risk of causing an economic slowdown. The Federal Reserve is trying to engineer a so-called “soft-landing”, i.e., a slowdown in growth without a recession; however, it is likely to err on the side of combating inflation at the expense of economic growth and employment, if necessary.

Public markets fell into a pattern in 2022: higher inflation reports led to increased interest rates and lower bond prices. The 10-year U.S. Treasury bond yield had already risen ~1% from Fall 2021 to 2.5% in March 2022 – at which point, the Fed first raised short-term rates (and they peaked in November at about 4.25%). This rapid rise in interest rates led to a sharp decline in bond prices and stock markets. Concerns over inflation, the interest rate outlook, and uncertainty surrounding whether the U.S. would enter a recession created volatility in the public markets.

Throughout the year, market participants were looking for a point at which the Fed would “pivot” or decelerate its rate increases, if not outright lower rates. Stock and bond markets rallied in the early summer and fall, following favorable inflation numbers (in hopes that the worst might have been behind us). Markets historically bottom out before the peak in short-term rates, so these anticipatory rallies are not unusual.

2022 Market Review

While it was a very tough year for stocks in the U.S. (with the S&P 500 down -18.1%), it was a uniquely bad year for the U.S. bond market, with the Bloomberg Aggregate down -13.0% – in response to the rapid rise in interest rates from a very low starting point. The S&P 500’s maximum drawdown of ~-24% was within the historical range of other bear markets; however, the peak selloff in the bond market of ~-17% was nearly twice as deep as 1980, during the country’s last period of stagflation. The below charts provide some context and historical perspective for the volatility that we have seen in the U.S. stock and bond markets over the past 40-45 years.

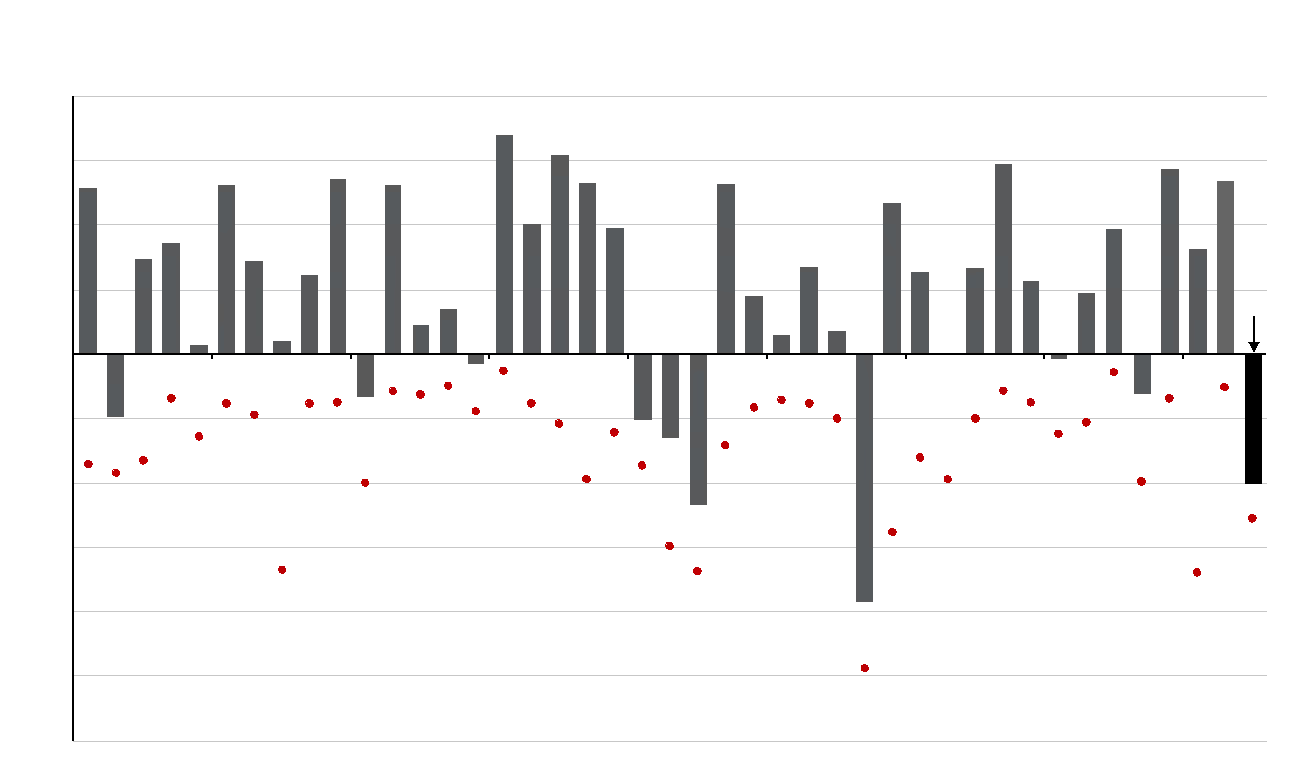

S&P 500 Intra-Year Declines vs. Calendar Year Returns

Despite 6 bear markets between 1980 and 2022, the average annual return was 9.4% on the S&P 500.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management

Returns are based on price index only and do not include dividends. Intra-year drops refers to the largest market drops from a peak to a trough during the year. For illustrative purposes only. Returns shown are calendar year returns from 1980 to 2021, over which time period the average annual return was 9.4%.

Guide to the Markets – U.S. Data are as of December 22, 2022

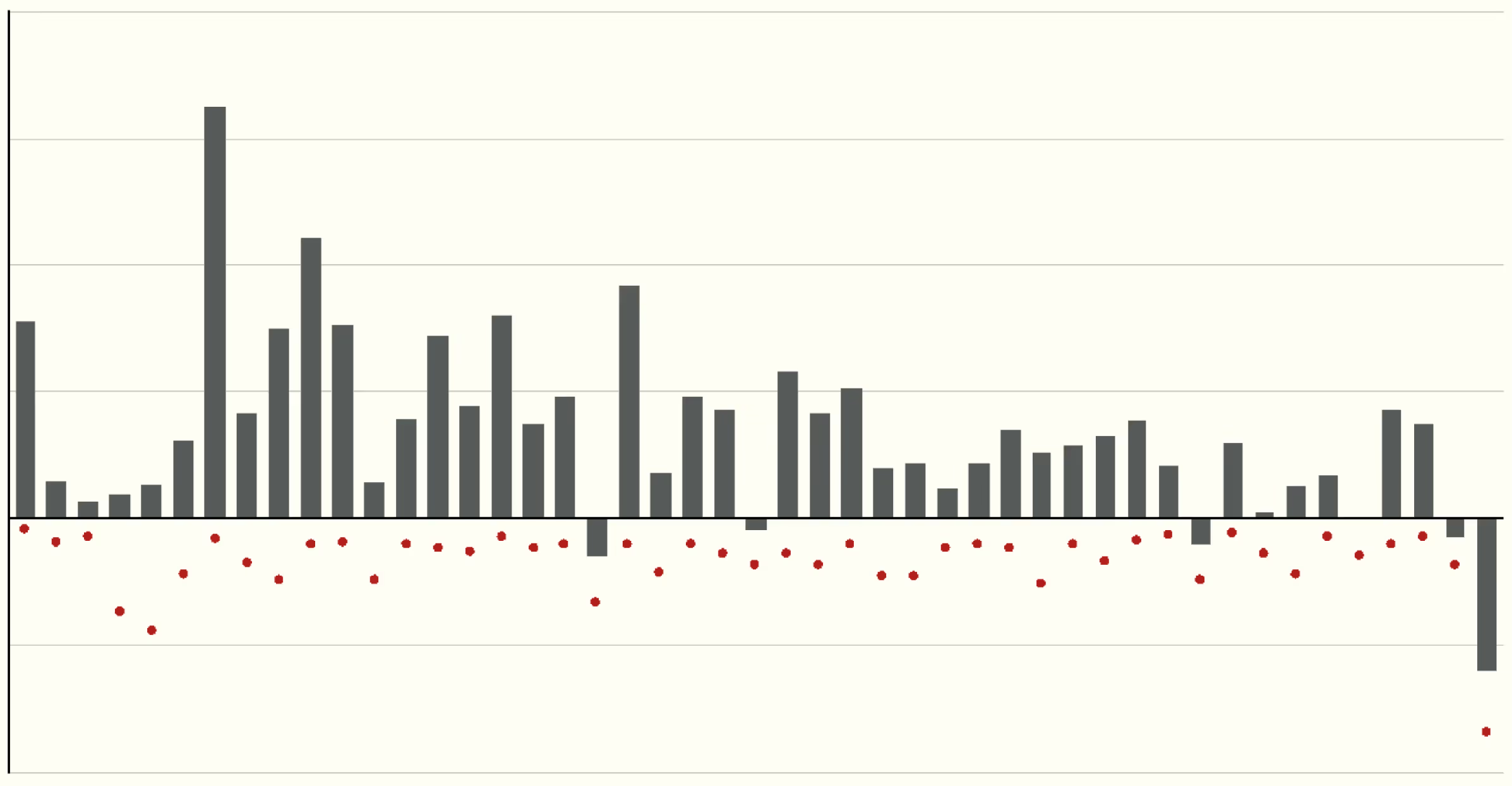

Bloomberg U.S. Aggregate Intra-Year Declines vs. Calendar Year Returns

Despite average intra-year drops of 3.1%, annual returns were positive in 42 of 46 years.

Source: Bloomberg, FactSet, J.P. Morgan Asset Management

Returns are based on total return. Intra-year drops refers to the largest market drops from a peak to a trough during the year. For illustrative purposes only. Returns shown are calendar year returns from 1976 to 2021, over which time period the average annual return was 7.1%. Returns from 1976 to 1989 are calculated on a monthly basis; daily data are used afterwards.

Guide to the Markets – U.S. Data are as of December 22, 2022

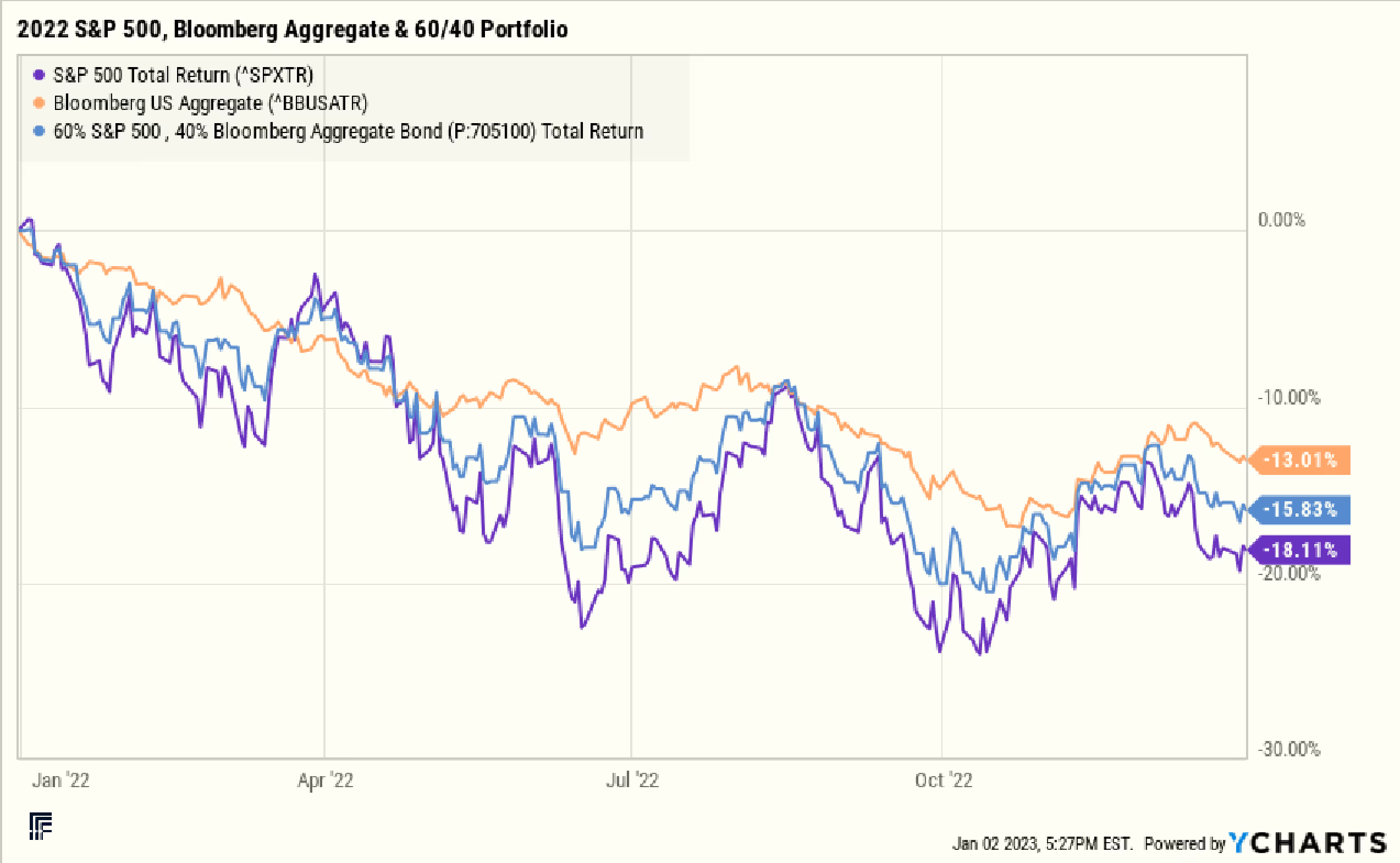

Traditional public market asset allocations did not work well for much of the year. For the majority of 2022: regardless of whether a portfolio was invested in bonds, stocks, or a traditional benchmark portfolio of 60% stocks/40% bonds, the returns were very similar. In prior bear markets, bonds had served the role of hedging equity portfolio returns. Through October 2022, though, stock and bond losses were highly correlated (as illustrated in the below chart); and the return lines converged during the year.

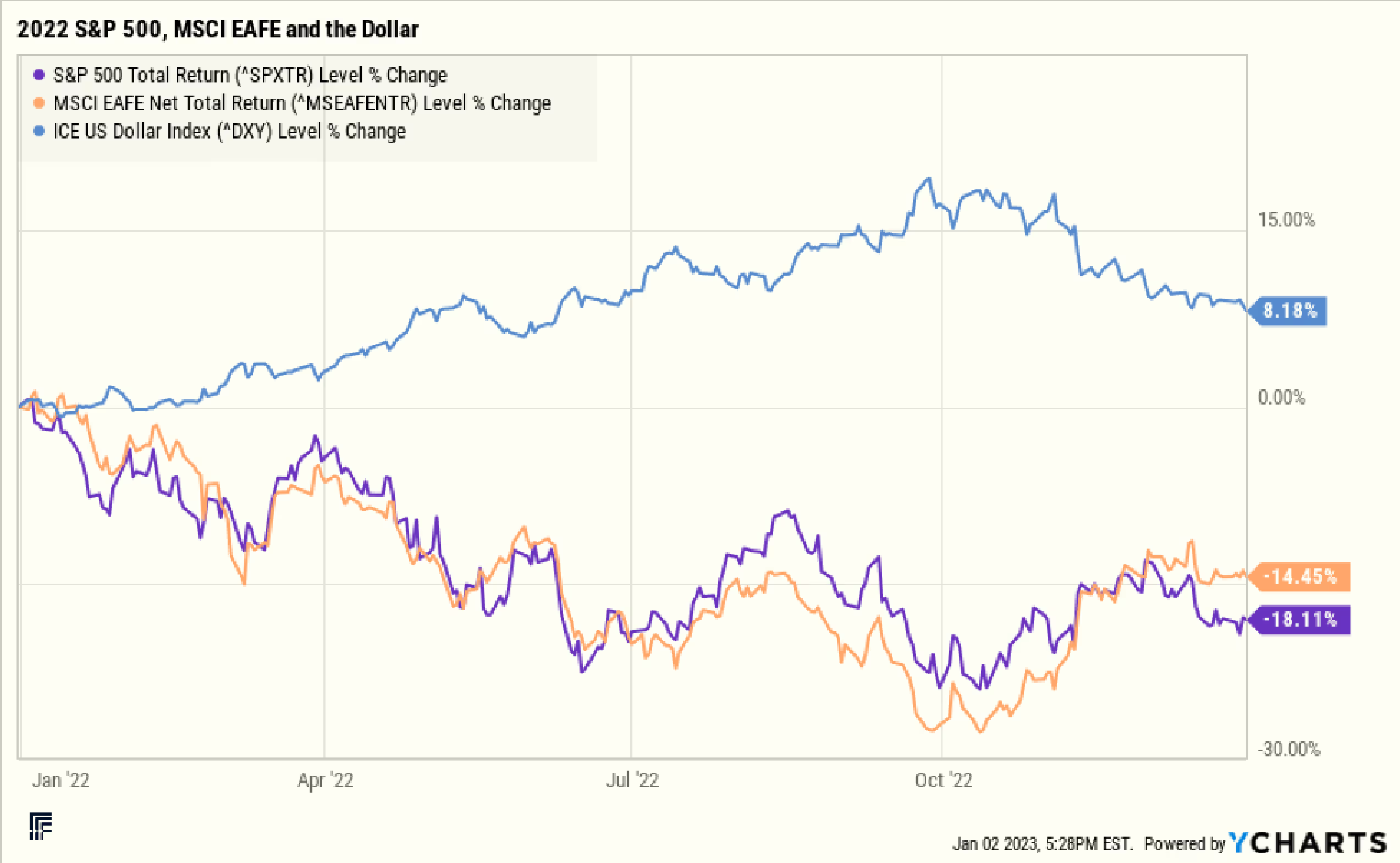

Notably, in November and December: as 10-year bond yields fell ~0.35% after November’s economic data, portfolio diversification began to work favorably for investors. Bonds rallied from their lows (as indicated in the above chart). The dollar, which had rallied almost 20% YTD through late September, gave up approximately half of its gains in November and December. The MSCI EAFE international stock index rallied from its lows of ~-27.6% to -14.5%, ultimately outperforming the S&P 500 for the year (as shown in the below chart).

What to Expect in 2023 and Beyond

We expect to see similar themes dominating the markets in 2023: inflation, the Federal Reserve’s responses to combat inflation, concerns over a possible recession or a soft-landing in the U.S., the continued war in Ukraine and its human and economic toll, and China reversing course from zero-COVID (and the possible effects that move may have on its citizens and economy). We would also place a high probability on an unexpected event taking place in the world.

It is important to note that following 2022’s substantial drawdown in both stocks and bonds, both major asset classes are priced more attractively looking forward – particularly when assessing the next five years. Yields on 10-year U.S. Treasuries rose from 1.5% to almost 3.9% between fall 2021 and the end of 2022. A bond investor’s yield at the time of purchase is a large component of the return on a go-forward basis (in fact, the return if held to maturity, without any default). We would view the likelihood of another 2%-point increase in long-term rates in 2023 as low. Even if we are incorrect, today’s higher starting yields would better soften the blow from bond prices falling again.

Earnings ratios on U.S. stocks fell from 22x forward earnings at the beginning of 2022 to 16.7x at the end of 2022. To put these figures into context: earnings were over 1 standard deviation more expensive than average at the start of 2022 and ended the year at their 25-year average multiple. All else being equal, buying stocks at a lower valuation increases the returns over the following five-year period. [Source: J.P. Morgan Asset Management]

It is important to acknowledge that if the U.S. enters a recession in 2023, earnings and the PE multiples that investors pay for them would likely fall (or at the very least, not expand to offset the expected earnings loss). In a recession, it is probable that the stock market could see losses during the year. If the U.S. enters a mild recession in 2023, however, we expect that the stock market would bottom before the low point in the economy. Traditionally, markets bottom when the economic data worsens at a slower pace than previously, not at the worst point in the economy.

Timing the markets is difficult. While we cannot definitively state that we have seen the peak in interest rates or the trough in the stock market, we do not believe that 2023 will see interest rates increase as dramatically as they did between late 2021 and the fall of 2022. With bonds more likely to fill their (more traditional) role of providing stability and a fixed rate of return in a portfolio, we would expect diversification to perform better for investors going forward. Stocks are beginning 2023 near their long-term average valuation and should provide a more attractive rate of return over the next 5 years. In fact, J.P. Morgan Asset Management recently raised their forward-looking expected returns for a diversified 60/40 portfolio to 7.2% per annum.

In addition, we believe that there are likely to be attractive opportunities in the private markets. Given the price dislocation in areas of the financial markets and the tightening of financing, it is likely that new investments in private equity, venture capital, real estate, and private credit are similarly likely to prove attractive over the coming years. We encourage you to speak with your advisor about the types (and proper sizes) of investments that would work best for your portfolio.

As always, we encourage investors to focus on time in the market, not timing the market. Rebalancing portfolios in both good and bad markets helps lead to the old adage of “buy low, sell high”. We recommend that clients connect with their advisors about their overarching financial plan, investment portfolio, and specific goals – and discuss whether your risk tolerance or circumstances may have changed during the last year. It is important to remember that investments are not the end goal; they are the means to the end of achieving one’s own goals in life.

---

David Darby

David serves as Chair of the Farther Investment Committee and also advises a select group of clients. With over 25 years of experience working with high-net-worth families, entrepreneurs, and executives, David brings particular expertise in managing multi-asset portfolios of public and private investments. He has spent his career helping clients successfully structure, execute, and implement complex planning strategies.

David was an advisor at Goldman Sachs for 21 years, prior to co-founding DG Wealth Partners, an independent RIA in 2017. DG Wealth Partners merged with Farther in 2022. David and his wife, Helen, live in Palm Beach Gardens, Florida, with their three children.