First Half Recap: Motion Without Progress

The first half of 2025 delivered no shortage of drama. The quarter began with Liberation Day’s shocking tariff announcements and ended with the TACO (Trump Always Chickens Out) trade. We experienced plenty of motion with a 20% correction driven by tariff fears, followed by a 25% rebound, only to end +5% YTD on the S&P 500. In fact, nearly +3% of that return came after June 23 alone – underscoring how quickly markets can reverse.

After Two Strong Years, 2025 Looks Tame – But It's Still a Win

After back-to-back years of 25%+ gains in 2023 and 2024, a +5% return for the S&P 500 in the first half of 2025 may feel underwhelming. But context matters.1

Following a sharp 20% correction in the spring, many investors are more than happy to be back in positive territory. It’s a reminder that staying invested through volatility often leads to better outcomes than trying to time the market.

Chart 1: VIX and Probability of a Recession YTD

Volatility (VIX) spiked from 20 to 60 before retreating to historical norm level of 16, while the probability of a recession remains elevated:2

- Treasury yields drifted higher despite an elevated probability of a recession.3

- International outperformed the US markets with the MSCI ACWI ex-US returning 17.9% versus the S&P returning 6.2%.

- Gold and Bitcoin climbed, signaling defensive positioning.

- Oil (WTI) remained choppy, reflecting geopolitical noise in the Middle East despite OPEC continuing to increase sidelined capacity.4

Key Takeaway: Investors who stuck with their plan – rather than reacting to April’s turbulence – likely saw stronger outcomes.

Second Half Outlook: Cautious Confidence

Markets have calmed, but uncertainty lingers. Here is what we are watching:

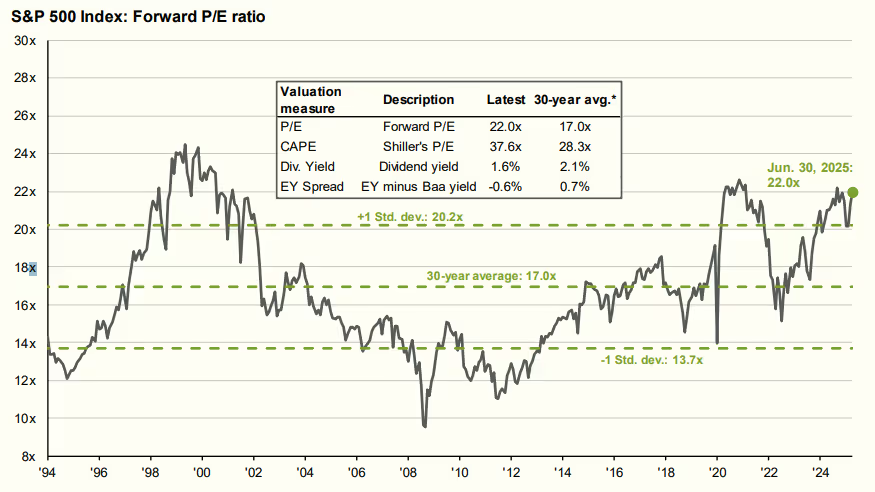

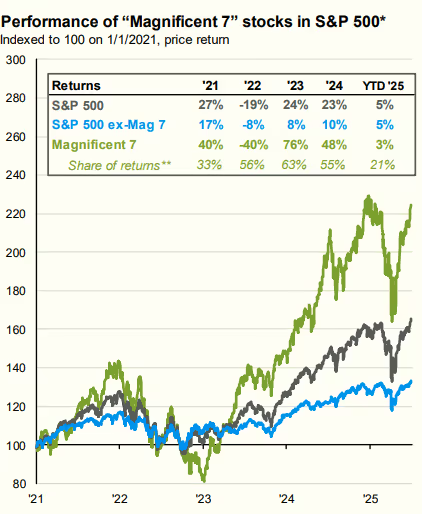

- Valuations remain elevated, especially among the “MAG-7” tech giants, while broader participation has diminished.

- The equity risk premium (the extra return expected from stocks over bonds) is at historic lows – offering little cushion for error.6

- Recession risk remains elevated, even if headline inflation is cooling.

- Macro headwinds persist:

- Tariff policy is creating uncertainty.

- The Federal Reserve remains passive, despite improving inflation data.

- Fiscal overhang and limited government flexibility restrict stimulus potential.7

Major macro and political debates shaping the second half:

- What’s the right multiple for today's market? Higher-quality companies may justify richer valuations.

- Does U.S. exceptionalism continue, or will global equities narrow the valuation discount?

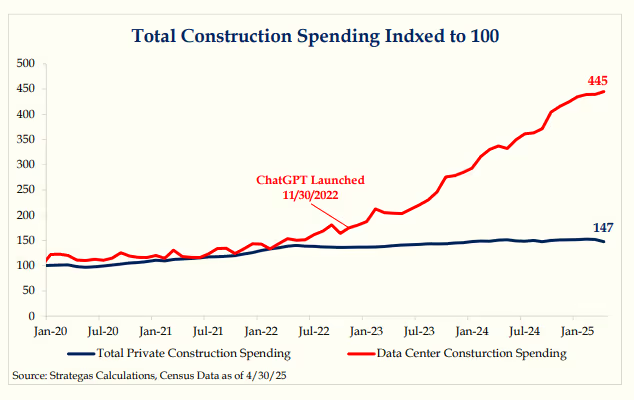

Chart 5: Data Center CapEx Driving Economic Activity

- How real is the AI-driven growth story? Its impact spans far beyond tech.8

- Will the weaker dollar become a tailwind on multinational earnings?9

Expect the Unexpected: Positioning for What’s Next

As we enter the second half of 2025, we expect headlines to be dominated by the 3 T’s: Trump, Tariffs, and Treasuries.

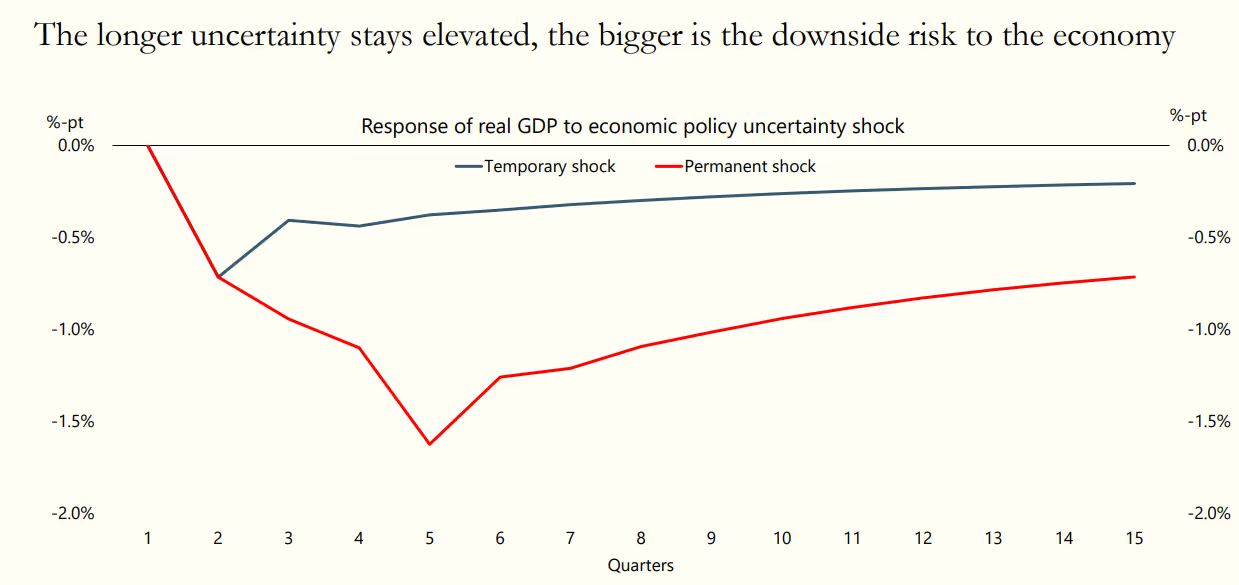

Chart 6: Economic Uncertainty Creates and Overhang on the Economy

Source: Apollo 06/21/2025

We expect continued volatility as markets react to ongoing policy uncertainty, with key areas of focus including the future of U.S. tariff policy and the proposed “Big Beautiful Bill”. While such fiscal measures may provide near-term economic stimulus, the bond market has responded unfavorably, given the bill’s implications for already deteriorating federal finances. Rising interest costs and a lack of fiscal discipline continue to constrain long-term flexibility.

Despite these overhangs, we believe that tactical market pullbacks may present attractive entry points. Markets are beginning to price in the prospect of more accommodative monetary policy – particularly as economic data softens and the path toward a potential change in Federal Reserve leadership in 2026 becomes clearer.10

“Be fearful when others are greedy and greedy when others are fearful.”

– Warren Buffett11

Our Approach: Stay Focused, Stay Invested

At Farther, we believe long-term performance is built on consistency, not reaction. Here’s how we’re managing through the noise:

- Customized asset allocation: Portfolios are aligned to your goals and adjusted for market dynamics.

- Tax-aware investing: We prioritize after-tax returns and optimize across taxable and tax-deferred accounts.

- High-touch, high-trust: You have direct access to an experienced team that understands complex financial lives.

Bottom Line

Even in a market that has largely “run in place”, disciplined investors continue to see meaningful progress. The second half of the year will undoubtedly bring new questions and complexities – but our commitment to delivering personalized, objective advice remains unwavering.

If you would like to discuss your portfolio or the broader outlook in greater detail, we welcome the conversation.

Sources

- Bloomberg, FactSet

- Bloomberg

- Bloomberg

- Bloomberg, CME Group, CoinDesk

- JP Morgan Guide to the Markets

- JP Morgan Guide to the Markets, Morgan Stanley Asset Management

- Congressional Budget Office (CBO

- McKinsey Global Institute, Strategas

- ICE U.S. Dollar Index (DXY)

- Federal Reserve FOMC Meeting Minutes, Chair Jerome Powell Speeches, WSJ FedWatch

- Berkshire Hathaway Annual Shareholder Letter, 1986