Following extensive congressional deliberations, President Trump signed comprehensive tax and spending legislation into law on July 4. This sweeping budget encompasses multiple components, including permanent provisions from the Tax Cuts and Jobs Act, enhanced state and local tax deduction limits, extended estate tax thresholds, and additional measures. The legislation seeks to balance these expansions through targeted spending reductions, particularly in Medicaid funding.

The significance of this legislation extends beyond trade policy discussions that have dominated recent months, addressing the prolonged uncertainty surrounding Washington's tax and spending framework. Despite political divisions regarding the budget's direction, it eliminates the looming "tax cliff" scenario where expiring provisions could have triggered substantial policy shifts at year-end.

Individual taxpayers face direct consequences through various financial planning elements, as specific legislative provisions create immediate household finance implications. From an investment standpoint, concerns persist regarding government expenditure levels, expanding national debt, and related factors that have influenced market performance over recent decades.

The recently enacted budget presents multiple perspectives for analysis. What essential information should investors understand regarding their personal financial strategies and long-term market implications?

Tax Cuts and Jobs Act provisions receive permanent status

The administration's "One Big Beautiful Bill" permanently establishes and broadens various 2017 Tax Cuts and Jobs Act (TCJA) elements previously scheduled for expiration. Additional taxpayer benefits are introduced, with spending cuts in select areas providing partial offsetting measures. Several major household-affecting provisions include:

- TCJA tax rates and brackets receive permanent designation, eliminating their original 2025 expiration date.

- Standard deduction amounts increase to $15,750 for individual filers and $31,500 for married couples filing jointly in 2025.

- Qualifying seniors receive an additional $6,000 deduction (termed a "senior bonus") with phaseouts beginning at $75,000 gross income. This provision expires in 2028.

- Alternative minimum tax exemption becomes permanent with phaseout thresholds rising to $500,000 for single filers, subject to future inflation indexing.

- Child tax credit expands from $2,000 to $2,200 per child, with inflation-indexed adjustments preserving purchasing power over time.

- State and local tax (SALT) deduction cap rises to $40,000 from the previous $10,000 limit, with 1% annual increases through 2029 before reverting to $10,000 in 2030.

- Tip income deduction allows up to $25,000 annually for workers earning under $150,000, effective through 2028.

- Various green energy tax credits face repeal, including electric vehicle and residential energy efficiency incentives.

- Federal debt limit increases by $5 trillion, removing congressional debt ceiling debates for an extended period and reducing political uncertainty.

- Business tax breaks expand to promote domestic investment and employment creation.

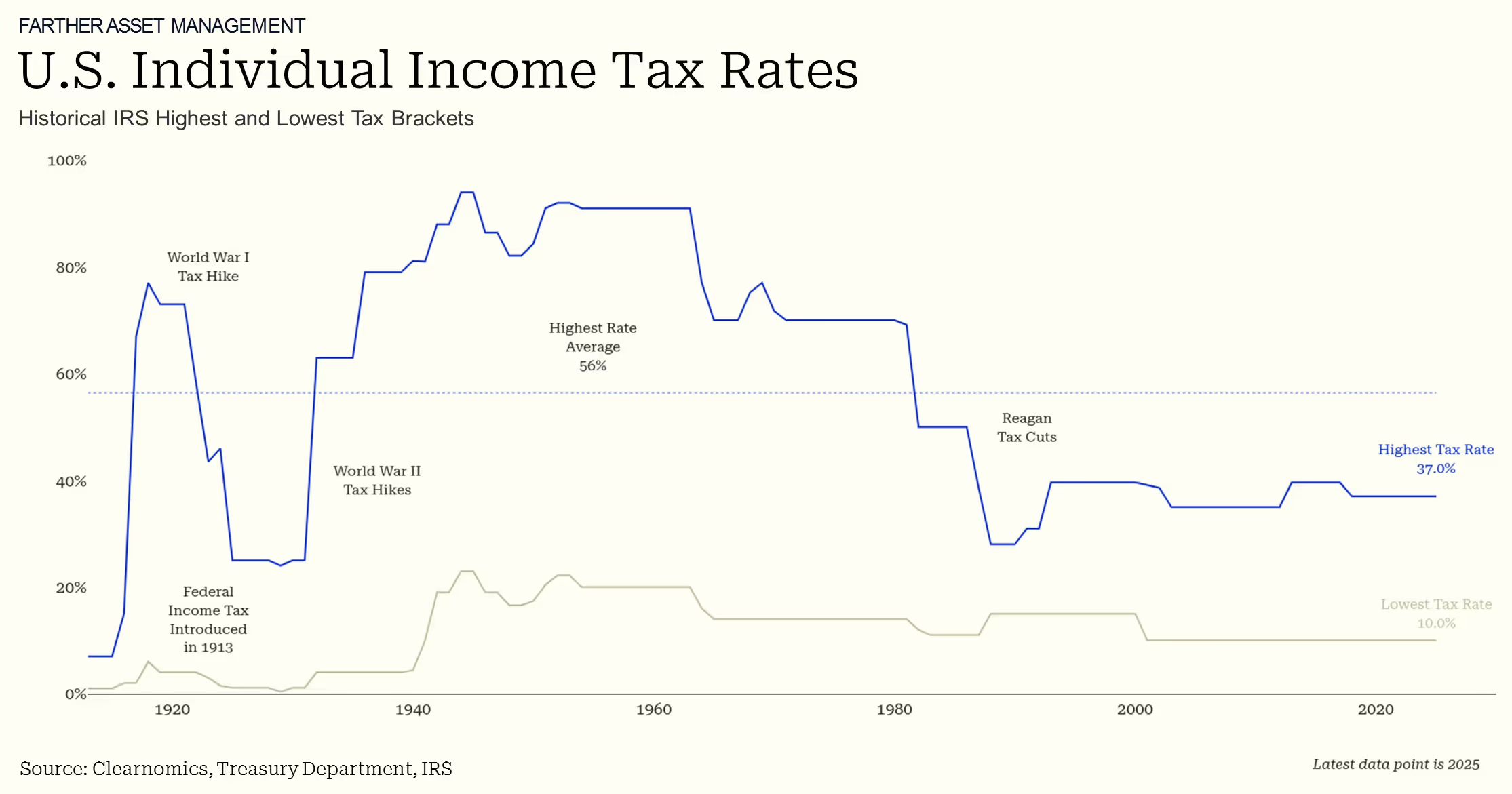

These modifications, among others, preserve the relatively favorable tax environment characterizing recent decades. The accompanying chart demonstrates current rates remain significantly below 20th century peaks, when top marginal rates exceeded 70% and occasionally surpassed 90% during wartime.

Mounting fiscal deficit concerns

Tax policy and government deficits represent interconnected issues, as revenue reductions from tax cuts require offsetting through reduced spending or increased borrowing. Most government expenditures support entitlement and defense programs that resist political modification. Treasury Department data shows 2025 spending allocations: Social Security (21%), Medicare (14%), National Defense (13%), and existing debt interest payments (14%).

Government borrowing has consequently increased consistently over the past century and will likely continue this trajectory. The Congressional Budget Office, a nonpartisan congressional support agency, projects this new legislation will add $3.4 trillion to national debt over ten years. This occurs against existing federal debt exceeding 120% of GDP, totaling $36.2 trillion, or approximately $106,000 per American.

Simple solutions remain elusive, particularly given the contentious political nature of fiscal policy. Tax reductions can stimulate economic growth, potentially offsetting revenue losses through increased economic activity. However, Washington's budget balancing record remains poor even during strong economic periods. The last balanced budgets occurred 25 years ago under President Clinton, and 56 years earlier during the Johnson administration.

The United States has not always maintained an income tax system. Modern income taxation began with the 16th Amendment in 1913, applying modest rates to relatively few Americans. The system expanded dramatically during the Great Depression and World War II, with top rates reaching 94% by 1944. Post-war reforms included President Reagan's 1986 Tax Reform Act, which simplified the tax code and reduced rates.

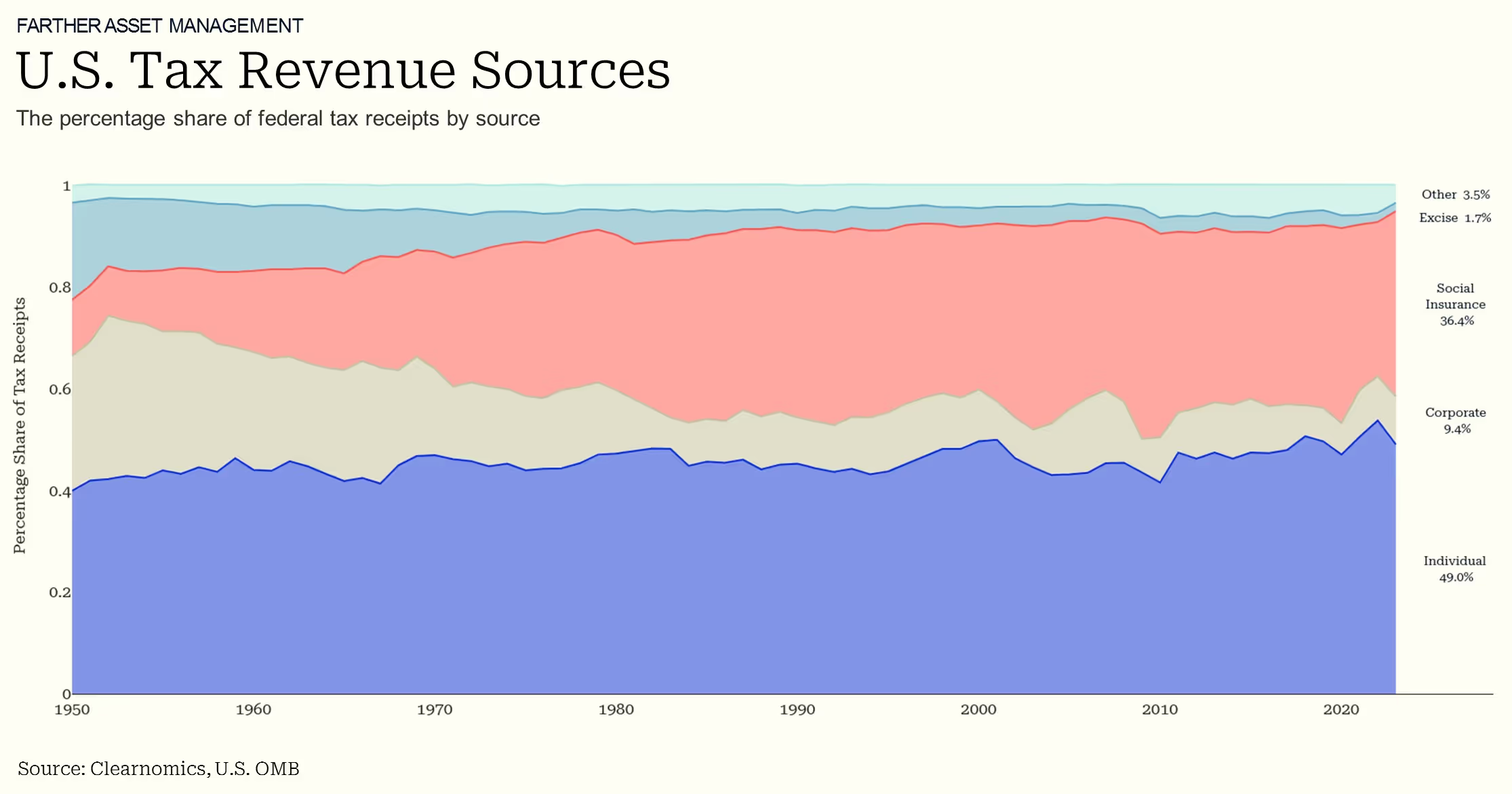

Current circumstances have evolved significantly since then. The accompanying chart illustrates individual income taxes now constitute the primary federal revenue source. Social insurance taxes, or payroll taxes, are deducted from wages to fund Social Security, Medicare, unemployment insurance, and related programs. Other revenue sources represent smaller proportions, including corporate taxes reduced by the TCJA and excise taxes like tariffs.

Tax policies directly impact investor financial plans and portfolios. From a macroeconomic perspective, fiscal implications have more limited effects. Over extended periods, elevated debt levels can influence interest rates and inflation expectations. While these factors have been relatively high recently, many worst-case scenarios have not materialized. Long-term investors should maintain diversified portfolios capable of performing across various fiscal and economic environments rather than reacting solely to policy changes.

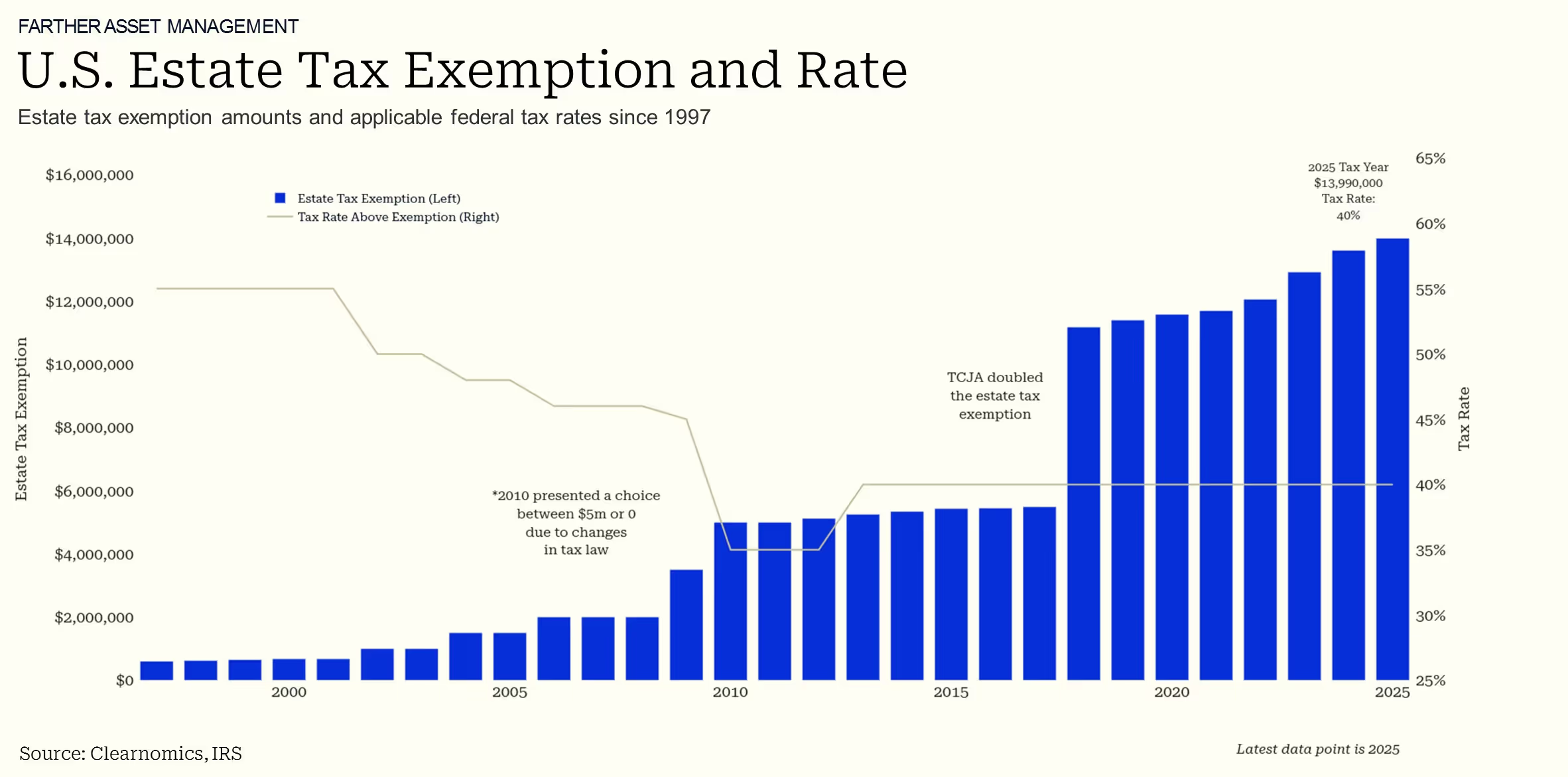

Legislation maintains elevated estate tax exemption thresholds

Estate tax exemption provisions would have been central to the tax cliff scenario. The TCJA doubled these limits, which were scheduled to revert to previous levels this year. The new tax bill's passage makes these higher exemptions permanent while further increasing thresholds to $15 million for individuals and $30 million for couples in 2026.

Although estate taxes may appear to affect only higher net worth households, all families must consider asset transfer strategies for future generations. This requires comprehensive approaches integrating estate planning, tax efficiency, philanthropy, and long-term family wealth preservation objectives. Individual states may also impose estate taxes with less favorable exemption thresholds than federal levels.

The bottom line? The new tax and spending legislation perpetuates and expands the current favorable tax environment. Investors should ensure their financial plans accommodate these tax provisions. Regarding expanding deficits and national debt, maintaining long-term perspective rather than portfolio reactions remains crucial.