Markets demonstrated remarkable resilience in May 2025, with the S&P 500 erasing its year-to-date losses despite significant headwinds. Prospects of an impending economic recession were relieved due to continuing strength in U.S. hard data, a rebound in soft data, and trade war détente. The month unfolded against a complex backdrop of trade developments, economic uncertainty, and questions about America's fiscal trajectory. For those with long-term investment horizons, May illustrated how markets can navigate challenging environments even when policy uncertainty looms large.

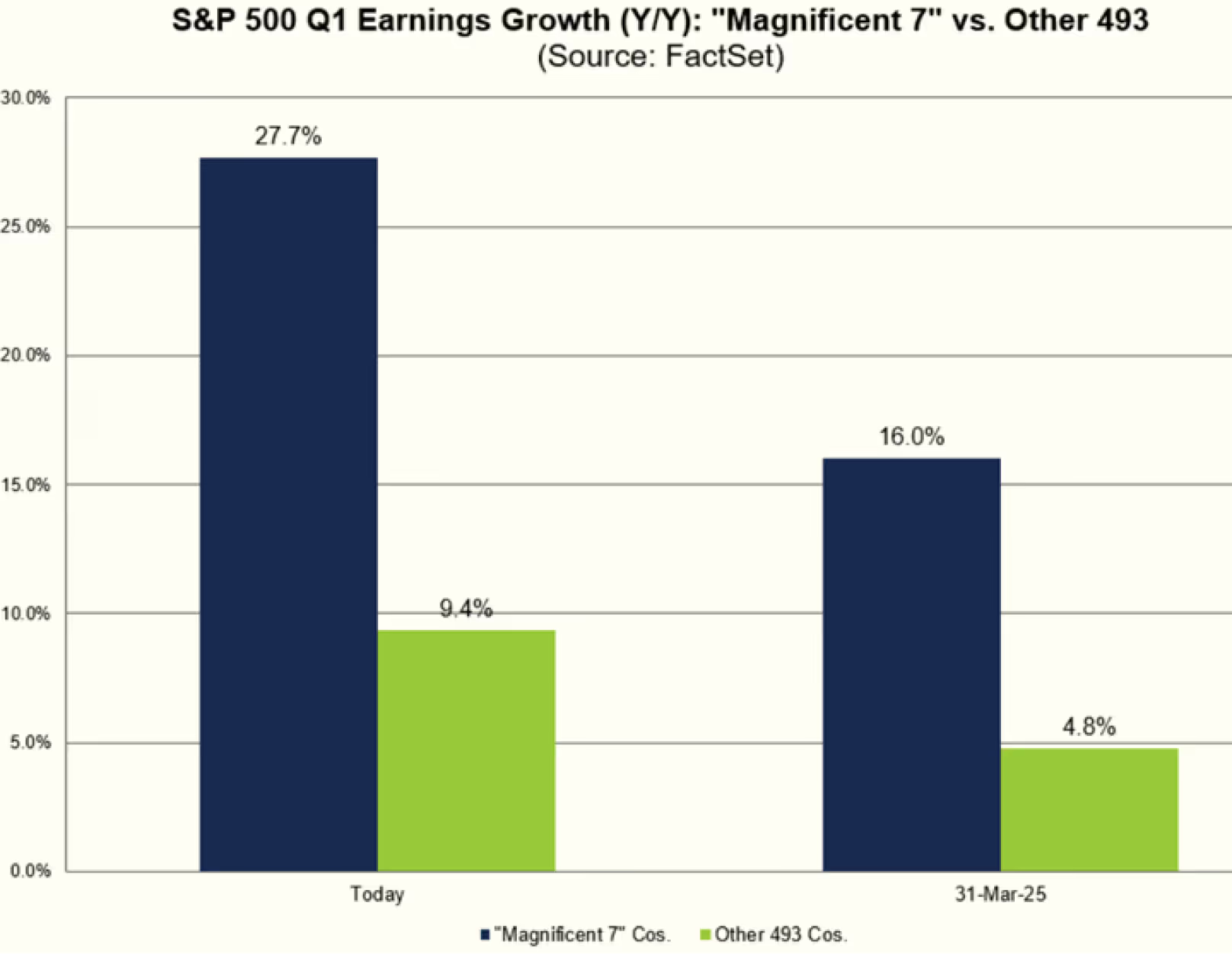

We saw the resumption of the AI trade, as Technology (+10.3%) and Communications (+9.6%) outpaced the S&P 500. Fears of an AI Infrastructure overbuild were alleviated as Mag-7 earnings growth accelerated relative to the other 493 companies. Traditional defensive sectors such as Staples (+1.66%) and Healthcare (-5.72%) were notable laggards. The negative performance in Healthcare was driven by the lower than expected profitability by United Healthcare, the largest Managed Care Company and third largest company in the Healthcare Sector.

May also coined the term “TACO” (Trump Always Chickens Out) Trade, as fears of worst-case tariff scenarios were eased when weekend trade war truces with both China and the European Union lifted animal spirits. Easing trade war rhetoric posed a significant risk for short sellers over the past month.

Bond yields experienced volatility, as investors grappled with federal spending concerns and debt sustainability. Of note is the move in long-term rates as the 10-year yields increased by 24 basis points from 4.18% to 4.42%. More notably, the 30-year Treasury closed above 5% on May 21, 2025 for the first time since October 2023. U.S. debt service has surpassed defense spending as the 3rd largest expenditure for the U.S. government, with potentially limited relief in sight due to Trump’s “Big Beautiful Bill”.

Key Market and Economic Drivers1

- The S&P 500 surged 6.2% in May, marking its strongest monthly performance since 2023, while the Dow Jones Industrial Average advanced 3.9% and the Nasdaq climbed 9.6%. For the year, the S&P 500 stands at +0.5%, the Dow at -0.6%, and the Nasdaq at -1.0%.

- The Bloomberg U.S. Aggregate Bond index dropped 0.7% in May, yet maintains a 2.4% year-to-date gain. The 10-year Treasury yield was at 4.4% at the conclusion of May.

- Global equities also showed strength, with both the MSCI EAFE developed markets index and MSCI EM emerging markets index rising 4.0%.

- The U.S. dollar index continued its descent, finishing May at 99.3, approaching three-year lows.

- Bitcoin reached a fresh all-time high of $111,092 before settling at $104,834 by month's end.

- Gold similarly achieved a new record peak at $3,422 before closing May at $3,288, representing a 24% year-to-date increase. Strength in gold can be attributed to both a flight to safety trade and Central Banks diversifying away from U.S. Dollar assets.

- Oil remained relatively flat +1.2% despite OPEC continuing to unwind voluntary curbs and increasing capacity by 411,000 barrels per day for May with further increases announced for June and July.

- The May Consumer Price Index data revealed that consumer prices increased 2.3% year-over-year, marking the smallest 12-month gain since February 2021. These readings bring inflation closer to the Fed’s 2% target and support the narrative that policymakers may be behind the curve on rate cuts.

- Employment data showed 177,000 new jobs added in April, with the unemployment rate holding steady at 4.2%.

- Volatility was the worst performing asset class, with the VIX -24.8% for the month of May

Market resilience emerged, despite fresh challenges

The May rally reinforces the value of maintaining investment discipline during volatile periods. Following April's difficulties, markets showed their adaptive capacity by recouping most losses and moving back into positive territory during May – demonstrating how rapidly investor sentiment can pivot when circumstances begin to improve, a dynamic that has characterized market behavior throughout recent years. The strength of May’s rebound illustrates the difficulty in market timing and the importance of maintaining a systematic investment plan.

Source: Fidelity Investments

Credit rating agency delivers U.S. downgrade

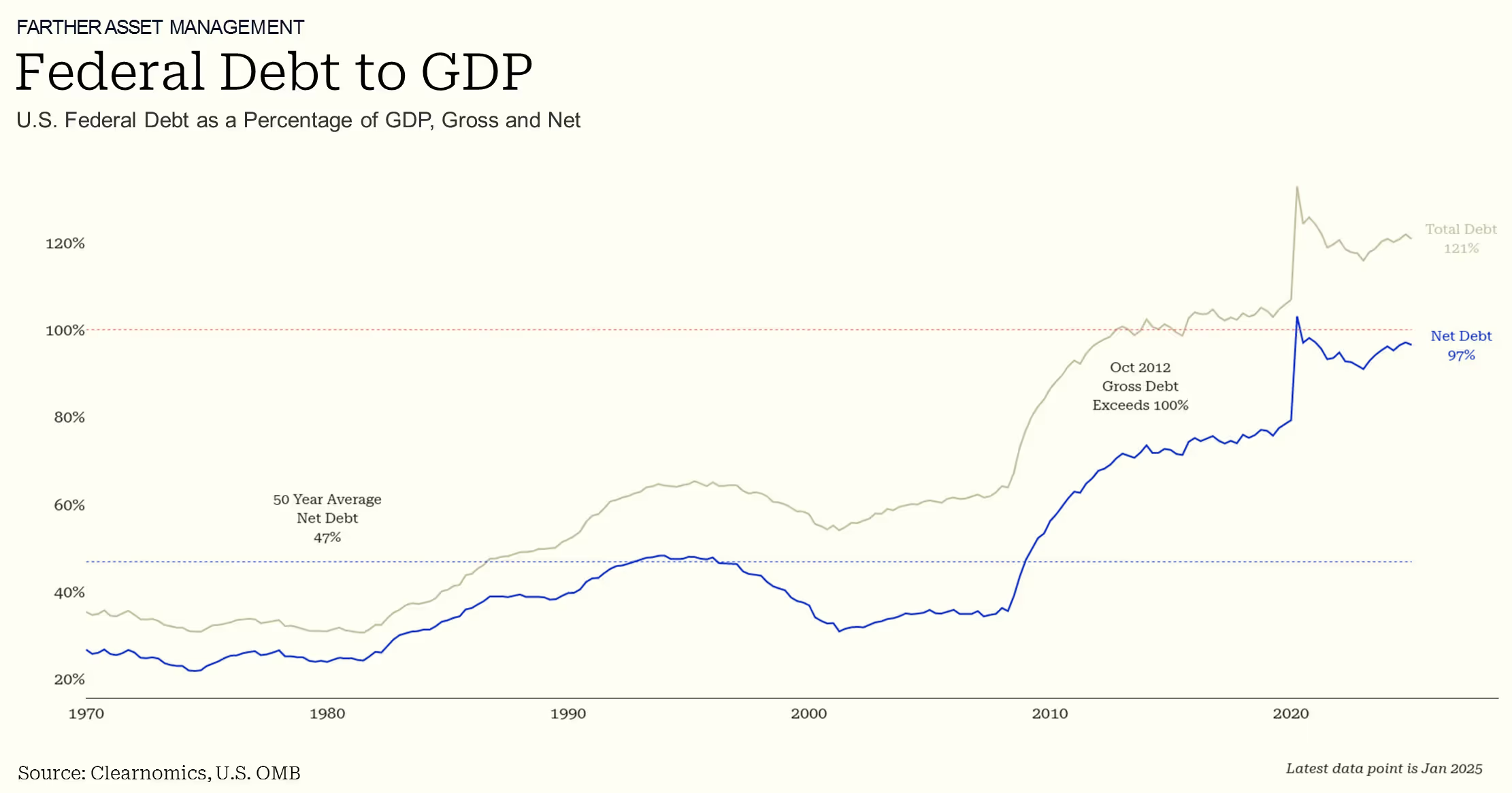

Another significant May development was Moody's decision to lower the U.S. credit rating from Aaa to Aa1. This action joined earlier downgrades from Fitch in 2023 and Standard & Poor's in 2011, all stemming from concerns regarding escalating debt levels and government expenditures. The above chart demonstrates that total U.S. debt reached 122% of GDP in 2024. Net debt, excluding intragovernmental holdings, has climbed to 97%.

Markets displayed minimal reaction to this historic credit downgrade, primarily because the assessment largely reflects existing conditions that investors already understand. The subdued response also draws from experience with the 2011 Standard & Poor's downgrade, when Treasury securities maintained their status as preferred safe haven investments.The timing may not have been coincidental, as the House of Representatives was simultaneously advancing comprehensive tax and spending legislation. The approved measure would extend individual tax provisions from the Tax Cuts and Jobs Act, including the 37% top rate, child tax credits, expanded State and Local Tax deduction limits, and exemptions for tips and overtime compensation, among other provisions. The Penn Wharton Budget Model estimates this legislation could expand deficits by $2.8 trillion over the coming decade.2 The measure now moves to the Senate for consideration and potential modification.While these fiscal challenges clearly demand long-term attention, the U.S. dollar's status as the global reserve currency ensures continued Treasury demand in the foreseeable future.

Trade discussions yield encouraging developments

May brought meaningful advancement in trade discussions, effectively removing several worst-case outcomes from consideration. The administration secured agreements with both the U.K. and China, while maintaining ongoing negotiations with other key trading partners. The U.S.-China arrangement established a 90-day window of reduced American tariffs on Chinese products.

Trade uncertainty will likely persist, despite these achievements. Recent developments have seen both China and the U.S. claiming violations of the trade agreement, while the administration pursues elevated tariffs on steel and aluminum products. Simultaneously, European Union negotiations generated optimism when the White House postponed its planned 50% EU tariff following constructive dialogue – indicating that diplomatic solutions remain viable, even when initial stances seem irreconcilable.

Legal challenges to tariff implementation also emerged in May. The U.S. Court of International Trade invalidated numerous recently imposed tariffs, determining they surpass presidential authority under the International Economic Emergency Powers Act. Although a federal appeals court suspended this ruling, maintaining current tariffs temporarily, this legal complexity introduces additional uncertainty to trade policy.

Trade policy development typically spans months and years, rather than days or weeks. May's market recovery demonstrates that investors should avoid overreacting to trade-related news, particularly given the reduced likelihood of extreme scenarios.

Corporate earnings provide market foundation

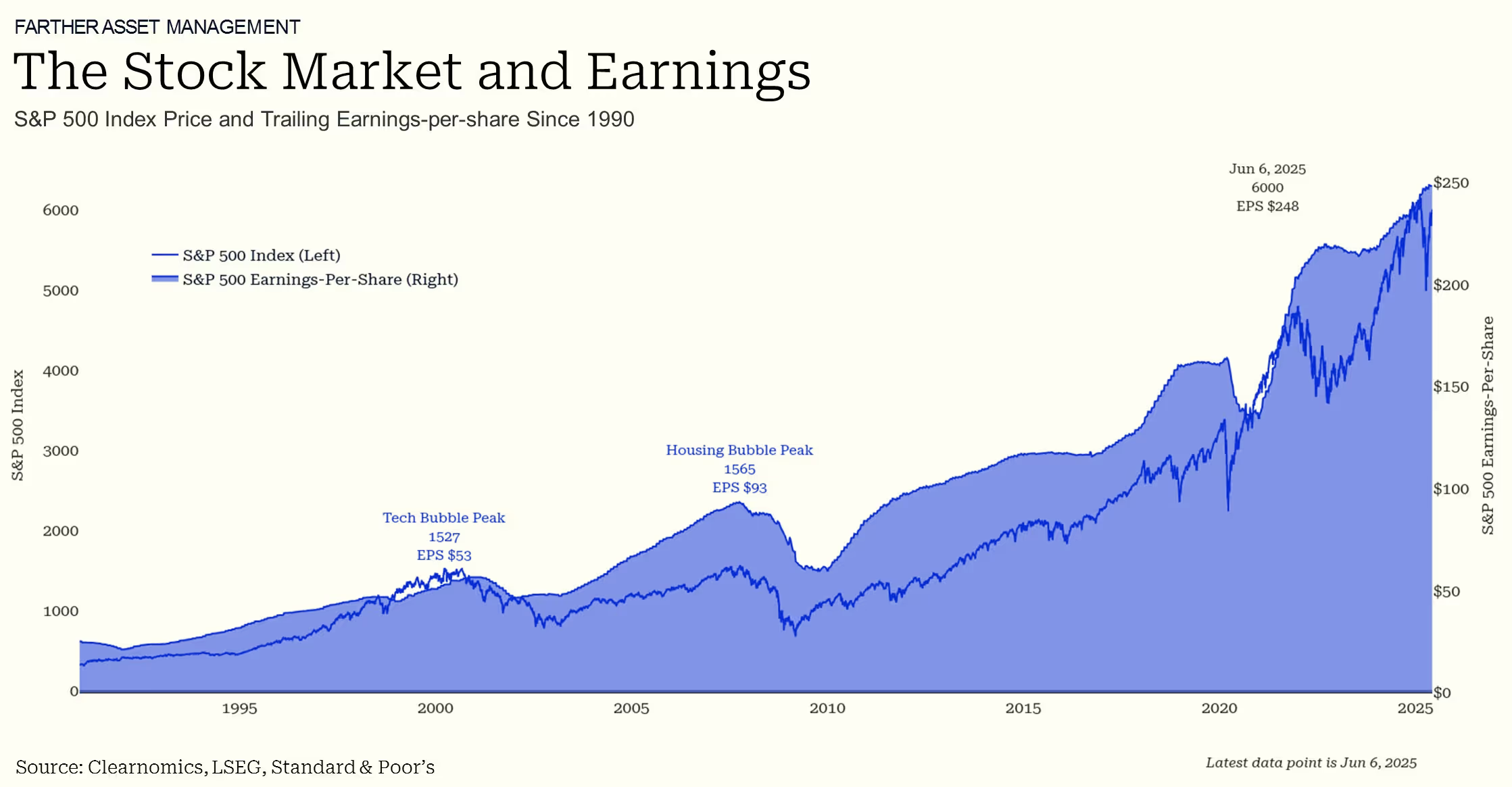

First quarter earnings results offered additional grounds for optimism. S&P 500 companies exceeded earnings per share expectations, with 64% reporting revenue beats, according to FactSet data.3

This robust earnings performance underscored the fundamental strength of corporate profitability, with technology sector companies demonstrating particular resilience amid trade policy uncertainty.

Consumer sentiment has remained subdued this year due to tariff and inflation concerns. However, recent sentiment measures began indicating improvement that better aligns with positive earnings and economic data. The University of Michigan's latest May survey revealed slightly declining inflation expectations and stabilizing sentiment. While single-month data should be interpreted cautiously, this improvement represents a promising trend. Strong economic fundamentals combined with improving sentiment could provide continued market support.

As we approach the second half of 2025, we find two underlying debates facing the stock market:

- Are the lows in for the year?

Historically, 20% corrections are followed by a low volume retest, with the recent exceptions being 2018 & 2020. While no two market cycles are identical, a key determinant this time will be whether the U.S. economy can avoid slipping into a recession. An additional factor to watch is the potential for an earlier-than-expected resolution to the ongoing trade dispute. Emerging legal challenges to the validity of certain tariffs may create pressure – and incentives – for a more expedited settlement.

- Will the remainder of the year bring a return to U.S. exceptionalism trade?

The beginning of 2025 was led by international markets, which stands in sharp contrast to the 2023-24 period where U.S. technology led global markets. The 2025 international outperformance contrast was driven by two key factors: 1) An aversion to the AI trade due to concerns of ROI and overcapacity, and 2) U.S. Dollar weakness boosting foreign market returns. While U.S. equities remain expensive, relative to international markets and their own historical valuations, accelerating earnings growth from the technology sector may potentially lead to U.S. market outperformance in the months ahead.

The bottom line? May delivered positive results for investors, despite significant challenges. Although the U.S. credit downgrade and fiscal concerns introduced new uncertainties, trade agreement progress helped lift markets. For long-term investors, these events highlight the importance of maintaining perspective and focusing on fundamental trends, rather than short-term policy developments.

---

- Standard & Poor's, Nasdaq, Bloomberg. All month-end figures are as of May 30, 2025.

- https://budgetmodel.wharton.upenn.edu/issues/2025/5/23/house-reconciliation-bill-budget-economic-and-distributional-effects-may-22-2025

- FactSet Earnings Insight (May 30, 2025)