Executive summary

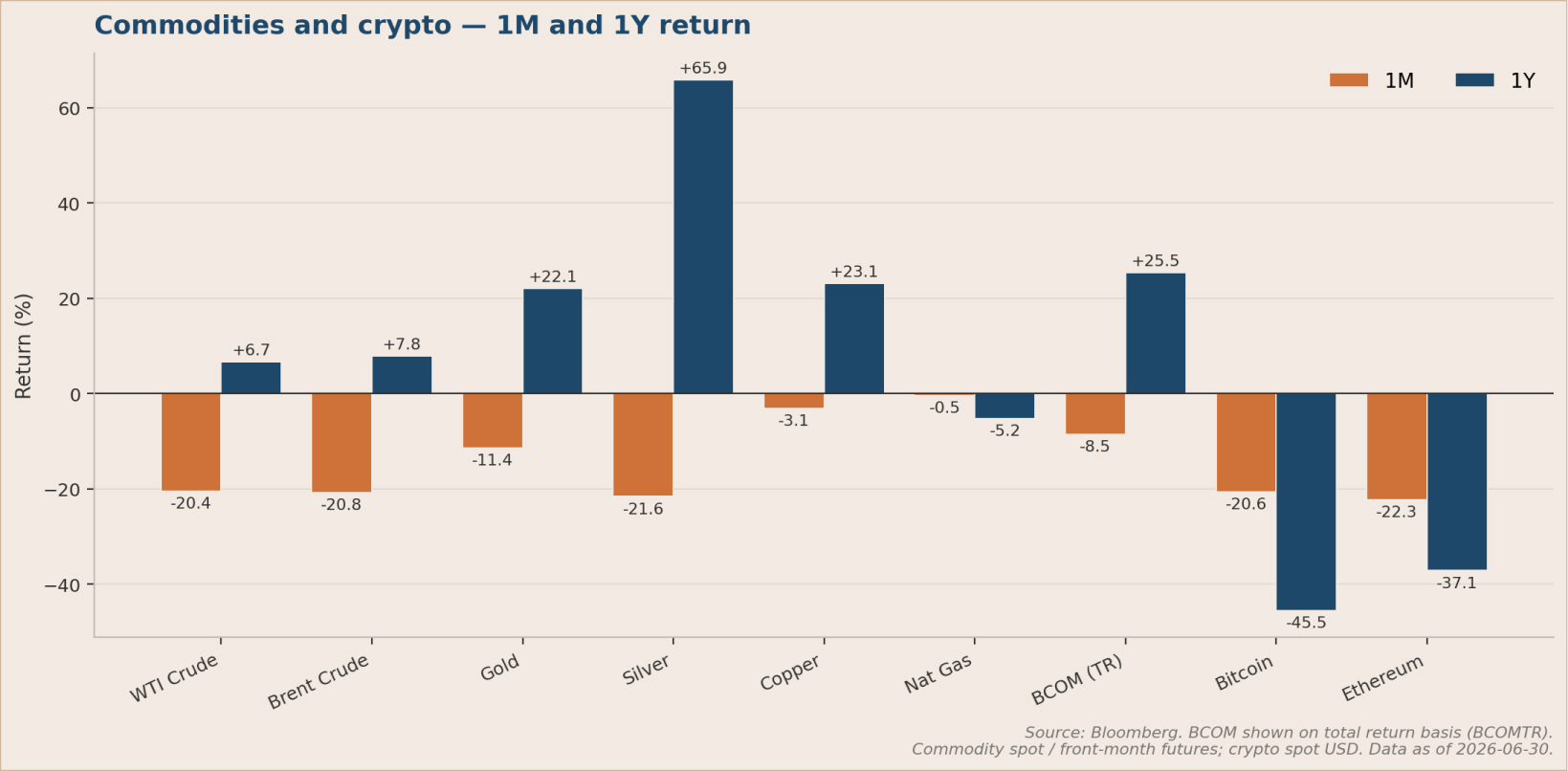

June 2026 proved to be a significant turning point for markets. A ceasefire in the Middle East and the reopening of the Strait of Hormuz (a critical shipping lane for global oil impacted by the war with Iran) [1] removed a major source of uncertainty that had been driving commodity prices higher: oil fell 20.4% and gold dropped 11.4% for the month [2][3].

At the same time, newly appointed Federal Reserve Chair Kevin Warsh signaled at his first policy meeting on June 17 that interest rates would stay higher for longer than markets had been expecting. The Fed's projected rate for 2026 moved up from 3.4% to 3.8%, the anticipated rate cut later this year was removed entirely, and markets are now pricing in the possibility of a rate increase in October [4][5]. Economic growth and the job market remain healthy, but key inflation measures re-accelerated: core inflation (which strips out volatile food and energy prices) rose to 3.41% and overall consumer prices climbed to 4.17% year-over-year [6][7], putting an end, for now, to hopes that inflation was steadily returning to the Fed's 2% target.

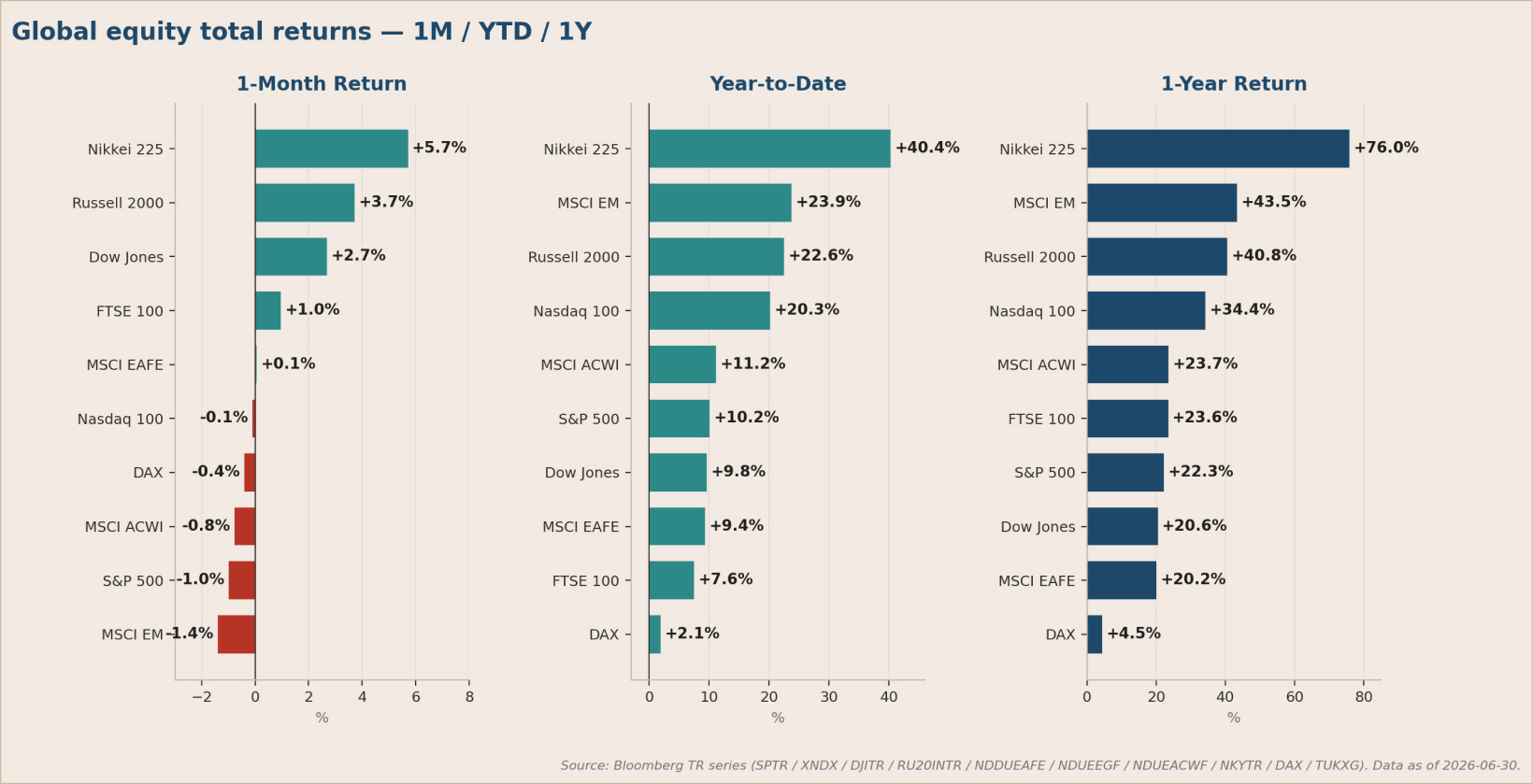

The stock market saw a massive rotation in June, out of many high-flying artificial intelligence (AI) and mega-cap technology names into more defensive, cyclical, and value-oriented sectors. Beneath a headline S&P 500 Index that fell 1.0% for the month [8], the breadth of the overall stock market's performance improved significantly: the industrials (+7.2%), health care (+6.5%), and financials (+4.2%) sectors led in June. Smaller companies outpaced larger ones by approximately 4.7 percentage points (the Russell 2000 small-cap index rose 3.7%), and value stocks, typically lower-priced, more established companies, beat faster-growing stocks by 5.0 percentage points [9]. Stocks in other developed economies such as Europe and Japan were roughly flat, while emerging markets lagged as the U.S. dollar strengthened (-1.4%).

Our investment approach is unchanged. We continue to focus on generating income, maintaining true diversification, and taking risk in a disciplined way. June rewarded investors who held a broad mix of assets and was difficult for those concentrated in a small number of positions, particularly large-cap technology stocks or commodity-linked holdings. That is exactly the pattern our portfolio positioning is designed to benefit from.

- Markets: The S&P 500 fell 1.0% in June, closing at 7,499 and leaving it up 10.2% for the year. The technology-heavy Nasdaq 100 was essentially flat (-0.1%), while small-cap stocks bucked the trend and rose 3.7%. Emerging market stocks fell 1.4%. The notable story was breadth: smaller, more value-oriented companies led the market while the largest technology names lagged [9].

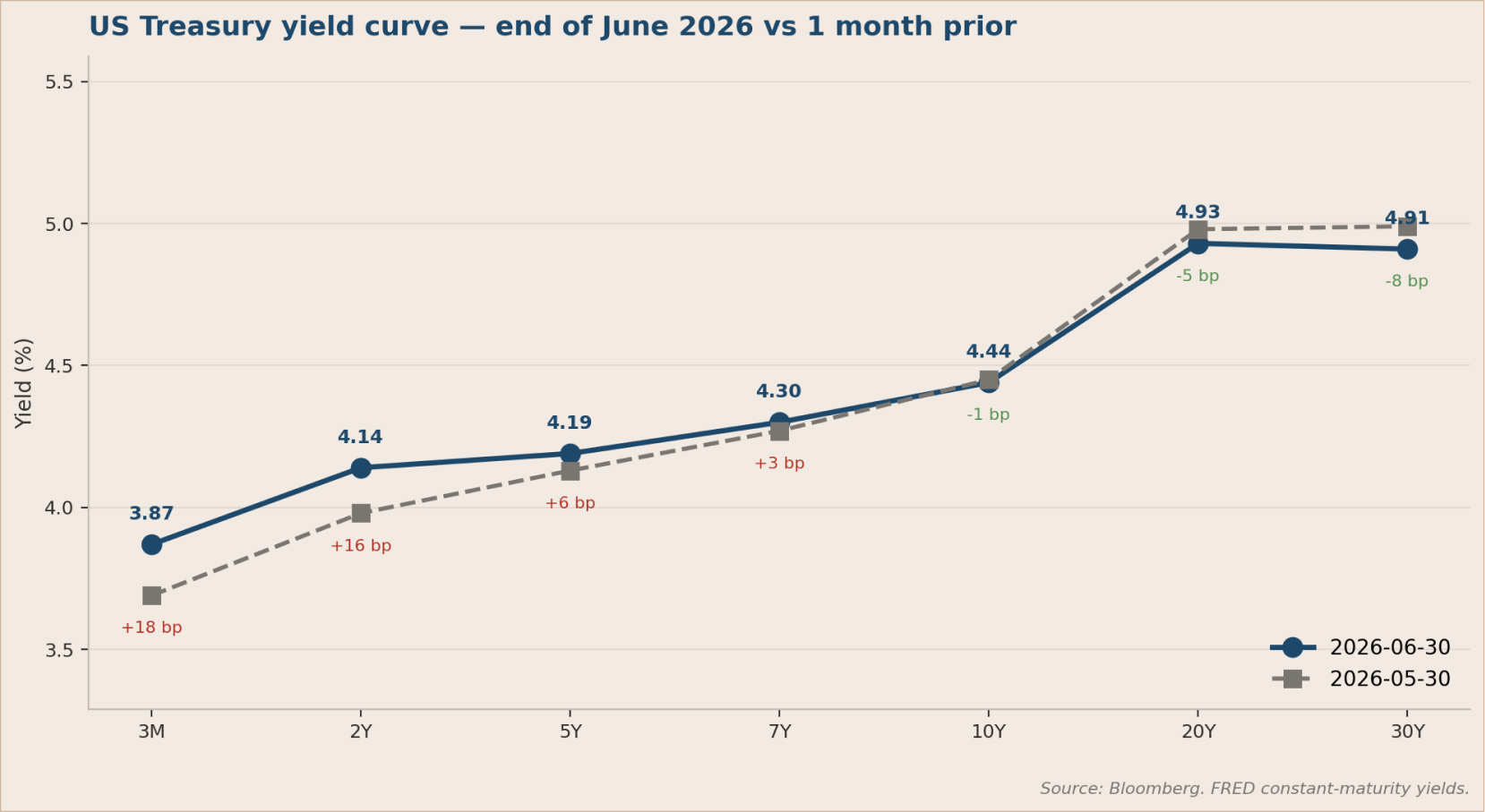

- Interest rates: The 10-year Treasury yield ended the month at 4.44%. Longer-term bonds now yield more than shorter-term ones, a normal relationship that had been absent for most of the past two years. Short-term government bonds are particularly attractive right now: 3-month Treasuries yield 3.87% and bonds maturing within the next year yield 3.8% to 4.1%, offering returns above inflation without the price volatility that comes with longer-term bonds [10].

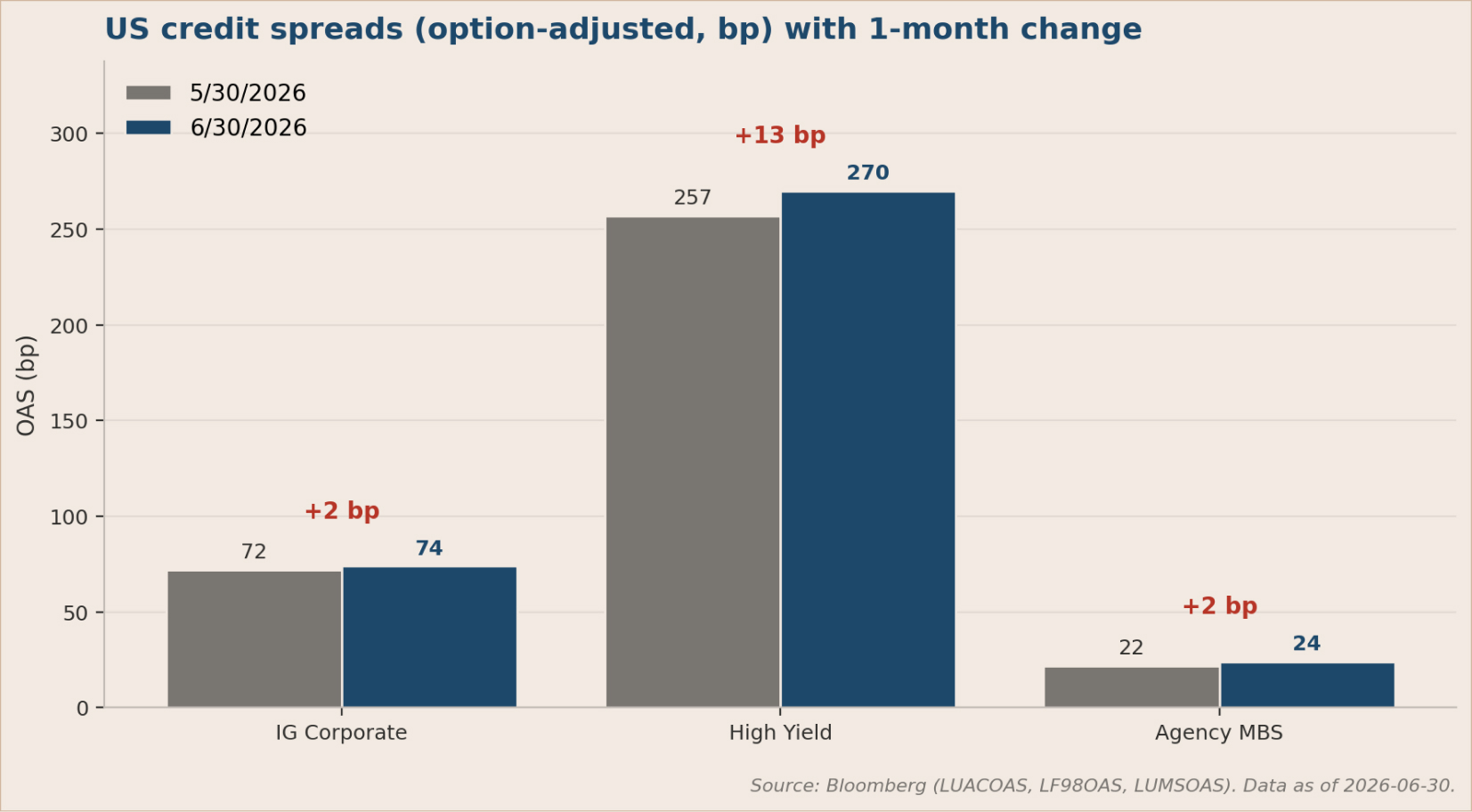

- Corporate bonds: Both investment-grade and high-yield corporate bonds are offering investors close to minimal income over government bonds, at or close to 52-week lows. In our view, the market is not adequately rewarding investors for the risk of lending to corporations at this point in the cycle [11]. We favor higher-quality bonds for any new fixed-income allocations.

- How we are currently positioned:

- Overweight: Small-cap stocks (with a preference for value-oriented names), stocks in developed international markets such as Europe and Japan, short-term government bonds, investment-grade corporate bonds, and cash.

- Neutral: Large-cap U.S. stocks (with a modest preference for value), mid-cap U.S. stocks, intermediate government bonds, TIPS, agency MBS, municipal bonds, international bonds, real estate, broad commodities, and gold.

- Underweight: Long term treasuries, high-yield corporate bonds, and alternative credit.

Our overall positioning reflects the view that we are in a late stage of the economic cycle. Small-cap value stocks look attractively priced relative to history. Higher-quality corporate bonds still offer reasonable returns relative to their risk. Conversely, the largest growth stocks, lower-quality corporate bonds, REITs, and convertible bonds all look expensive or carry risks we do not think the market is fully pricing in. We are positioned defensively, with an emphasis on shorter maturities in our bond holdings.

Strategic asset allocation: Positioning summary

The table below summarizes the Farther Investment Strategy Team’s active stance by asset class relative to a strategic-neutral policy allocation, with a conviction rating indicating how confident we are in the current stance. The narrative rationales that follow address the reasoning behind each major overweight and underweight.

The big picture

June delivered two major surprises to markets at the same time, and both moved against widely-held expectations.

The first was the sudden drop in commodity prices. A ceasefire in the Middle East and the reopening of the Strait of Hormuz removed much of the geopolitical anxiety that had been pushing oil, gold, and other assets higher. Oil fell 20.4%, gold dropped 11.4%, silver fell 21.6%, and Bitcoin declined 20.6% [2][13]. Investors who had positioned themselves for an ongoing crisis saw those so-called “risk-off” bets unwind sharply.

The second surprise came from the Federal Reserve. On June 17, new Fed Chair Warsh signaled that the Fed was no longer planning to cut interest rates in 2026 and raised the possibility of an increase in October [14]. That was more aggressive than markets had anticipated.

What didn't happen is just as notable. Long-term government bonds, which many investors treat as a safe haven, barely moved despite the commodity selloff, with the 10-year Treasury yield essentially unchanged (down 0.01 percentage points). And rather than falling broadly, the stock market actually broadened. The areas that rose weren't the traditional "safe" assets, but a wide range of sectors that had previously been overshadowed by large technology companies.

June was a reminder that genuine diversification means owning assets that tend to behave differently from one another, not simply owning assets with a reputation for being safe.

The rally beneath the surface was notable. Industrials led at 7.2%, health care rose 6.5%, financials gained 4.2%, and utilities added 2.4% (materials were essentially flat, -0.1%): the first clear month in over a year where technology stocks gave up market leadership to other sectors [15]. Smaller companies (Russell 2000 small-cap index, +3.7%) outpaced large companies (S&P 500 index) by approximately 4.7 percentage points. Value stocks (typically more established, lower-priced companies) beat growth-oriented stocks by approximately 5.0 percentage points, an unusually wide gap for a single month [9]. This kind of broadening, where more of the market is participating in gains rather than just a handful of large names, is generally considered a healthy sign and looks to us more like a maturing bull market than one beginning to break down.

The underlying economy remains on solid footing. The Atlanta Federal Reserve's real-time growth estimate puts second-quarter GDP growth at approximately 2.4% [16]. Employers added 129,000 jobs in May [17] and the unemployment rate held steady at 4.3% [18]. A closely watched recession indicator known as the Sahm Rule, which has historically signaled recessions when unemployment rises sharply from recent lows, currently reads well below its alert threshold, suggesting no near-term recession risk [19].

The challenge is inflation. Both major inflation measures re-accelerated in May: the Fed's preferred measure, core PCE (which excludes food and energy prices), rose to 3.41%, and the broader Consumer Price Index came in at 4.17% year-over-year [6][7]. The Fed's response was to remove its previously planned rate cut from its projections for the second half of the year. The current picture is one of an economy that is still growing, but with inflation that remains stubbornly above the Fed's 2% target — meaning interest rates are likely to stay higher for longer than many investors had hoped.

SpaceX IPO: A glimpse into the future of IPOs?

SpaceX completed one of the most anticipated initial public offerings (IPOs) in recent memory, reigniting enthusiasm for growth companies and innovation. The company's successful public debut reflected investors' continued appetite for businesses with transformational potential and strong long term growth narratives.

There is little question that Elon Musk has built some of the world's most innovative companies while disrupting multiple industries. SpaceX has fundamentally changed the economics of space launch and continues to expand its ambitions across satellite communications, defense, and space exploration.

The investment debate, however, is less about the quality of the business and more about the valuation investors are willing to pay. Many bullish forecasts assume extraordinary revenue growth over the next fifteen years, supported by exceptionally high profit margins. Those projections require SpaceX to become one of the largest and most profitable companies ever created.

History has shown that revolutionary companies can justify premium valuations, but investors should recognize that lofty expectations leave little room for disappointment. Even exceptional businesses can produce disappointing investment returns if expectations become too optimistic.

A broader concern is developing within the IPO market itself. Many of today's largest technology companies are remaining private far longer than previous generations, allowing private investors to capture much of the value creation before public investors have an opportunity to participate. By the time these companies reach the public markets, valuations often already reflect years of anticipated growth. With several large technology IPOs expected over the coming years, maintaining investor confidence in the IPO market will remain important for both companies and investors.

A new direction at the Federal Reserve

While the SpaceX IPO captured most of the financial headlines in June, we believe the Federal Reserve’s meeting may ultimately prove to be the more important event for markets.

The Fed left its policy rate unchanged at 3.50 percent to 3.75 percent. More notable than the decision itself was the shift in communication under new Fed Chair Kevin Warsh.

The post meeting statement was noticeably shorter, the traditional emphasis on forward guidance was reduced, and the Fed signaled a greater willingness to let incoming economic data drive future policy decisions rather than relying heavily on preannounced policy paths. Chair Warsh also announced several internal reviews covering Fed communications, the balance sheet, economic data, productivity, employment, and the inflation framework.

Markets initially interpreted the meeting as somewhat hawkish. We view it differently.

With the Fed reviewing many aspects of its policy framework, we believe officials are likely to move cautiously over the coming months. At the same time, easing energy prices following reduced geopolitical tensions have helped moderate inflation pressures. If those trends continue, inflation may have already reached its high point for 2026.

At a glance: The state of the economy

- Economic growth: The U.S. economy is estimated to be growing at roughly 2.4% annually in the second quarter of 2026, according to the Atlanta Federal Reserve's real-time tracking model [16]. That is a healthy pace, though somewhat slower than the stronger growth seen earlier in this cycle.

- Jobs: Employers added 129,000 jobs in May [17], and the average over the past three months has been approximately 110,000 per month — a steady, solid pace. The unemployment rate held at 4.3% [18]. The number of open, unfilled jobs across the economy has been declining but remains above the levels typical before the pandemic, suggesting employers are still actively hiring.

- Consumers: Retail spending rose 0.4% in May compared to April, and overall consumer spending continues to grow, though more slowly than before. Americans are still spending, but with more caution.

- Consumer confidence: The University of Michigan’s widely-followed consumer sentiment survey came in at 44.8, a reading that is at the low end of its historical range and consistent with a stressed consumer. The primary driver of that pessimism is frustration with the continued high cost of living.

- Inflation: Consumer prices rose 4.17% over the 12 months through May 2026, up from 3.78% the prior month [7]. Stripping out volatile food and energy costs, so-called “core” inflation ran at 2.8% by one measure and 3.41% by the Federal Reserve's preferred measure [6], both moving in the wrong direction. Part of the May increase reflected higher energy prices before oil's sharp drop late in the month, but prices for services and housing also picked up, which is a more persistent concern.

- What this means for interest rates: With inflation running well above the Fed's 2% target and still moving higher, the case for cutting interest rates in the near term has effectively disappeared, and the Fed made that explicit at its June 17 meeting. For borrowers, the practical consequence is visible in the average 30-year fixed mortgage rate, which ended the month at 6.49% [20].

Equities: A broadening bull market, not a failing one

Which sectors led and which lagged

Industrials led at 7.2%, health care gained 6.5%, financials rose 4.2%, and utilities added 2.4% (materials were essentially flat, -0.1%). Technology fell 3.3% and energy dropped 5.1%, making June the first month in over a year where technology stocks meaningfully underperformed the broader market [15].The reasons behind two of the biggest winners are worth unpacking. Financial stocks, particularly banks, benefited from the current shape of the interest rate environment. When longer-term rates sit meaningfully above short-term rates, as they do now, banks can borrow cheaply and lend at higher rates, widening their profit margins. Health care gains were driven by two forces: investors rotating toward more defensive, recession-resistant companies, and better-than-expected cost data from Medicare Advantage insurance plans in the first quarter.

How different sizes and styles of stocks performed

June illustrated a clear divide between large and small cap companies. Large-cap stocks (S&P 500) fell 1.0% while small-cap stocks (Russell 2000) rose 3.7%, with mid-sized companies landing in between. Among investment styles, growth stocks, typically younger and faster-expanding companies whose value is tied to future earnings, fell 2.7%, while value stocks, generally more established companies trading at lower prices relative to their current earnings, rose 2.3%.The technology-heavy Nasdaq 100 index was essentially flat for the month (-0.1%) as the largest technology companies paused after a strong run. Its longer-term gains remain intact, though: up 20.3% for the year and 34.4% over the past 12 months.

International markets

Stocks in other developed economies such as Europe and Japan were roughly flat for the month, though they remain solidly positive for the year (+9.4%) and over the past 12 months (+20.2%). Emerging markets, covering developing economies such as China, India, and Brazil, fell 1.4% for the month. India rose 1.5% while Brazil fell 2.9%, both restrained by a strengthening U.S. dollar, which makes dollar-denominated assets more expensive for foreign investors and reduces the value of overseas returns when converted back to dollars [9][21][22][23].

Despite the monthly setback, emerging markets have been the strongest-performing category over the past year, up 43.5%.

Fixed income: Favoring shorter maturities and higher-quality

Government bond yields across different maturities ended June as follows: 3-month Treasuries at 3.87%, 2-year at 4.14%, 5-year at 4.19%, 10-year at 4.44%, and 30-year at 4.91% [10]. The fact that longer-term bonds now yield more than shorter-term ones is worth pausing on. For much of the past two years the reverse was true, with short-term rates sitting above long-term rates in what is known as an inverted yield curve. That unusual condition, which often signals economic stress, has now normalized. Rates now rise steadily as you move further out along the maturity spectrum, and that gap has been slowly widening.

One notable development in June was that 10-year Treasury yields barely moved, essentially unchanged (down 0.01 percentage points) despite the Federal Reserve's more aggressive tone at its June 17 meeting. The reason is that the sharp drop in oil prices simultaneously removed some of the inflation anxiety that had previously been built into long-term bond yields. Those two forces largely cancelled each other out [10].

Corporate bonds are currently offering investors very little extra compensation for taking on credit risk. The additional yield that investment-grade corporate bonds pay over equivalent government bonds sits near its lowest point in the past year. The same is true for high-yield bonds, commonly known as junk bonds, and for mortgage-backed securities [11]. In plain terms, the bond market is behaving as though there is almost no chance that companies will struggle to repay their debts. That level of confidence is historically unusual and, in our view, unwarranted at this stage of the economic cycle.

Adding to that concern, the asset management firm PIMCO warned in June that losses are beginning to surface in riskier corners of the lending market, particularly in leveraged loans and privately arranged corporate debt [24]. Those losses have not yet shown up in publicly traded bond prices, but we think the warning is credible and worth acting on before the broader market catches up.

Our response is to prioritize quality in any new fixed income allocations. Within corporate bonds, we prefer higher-quality issuers rated just below or at the border of investment grade, rather than reaching further down into the riskiest, lowest-rated debt. For investors who want exposure to mortgage-related bonds, we favor government-backed mortgage securities over corporate bonds, as they tend to hold their value more reliably when interest rates move. For higher-income investors in the top federal tax brackets, top-rated municipal bonds currently yield 2.90%, which works out to the equivalent of a 4.6% taxable yield [11].

The interest rate backdrop

The 30-year Treasury bond now yields 4.91%, and long-term interest rates are being held at elevated levels by three separate forces that are each pushing in the same direction. The first is inflation. Price increases have re-accelerated in recent months rather than continuing their expected decline, giving the Federal Reserve less room to consider cutting rates.

The second is the federal government's fiscal position. The U.S. is running large budget deficits and issuing substantial amounts of new Treasury debt to fund them. When the supply of bonds increases, prices tend to fall and yields tend to rise.

The third is Federal Reserve policy itself. The Fed's shift toward keeping rates higher for longer has removed the expectation of near-term rate cuts that had previously been helping to hold long-term yields down.

For investors willing to buy and hold bonds through maturity, the current environment does offer something that has been largely absent for most of the past decade: a genuine return above inflation.

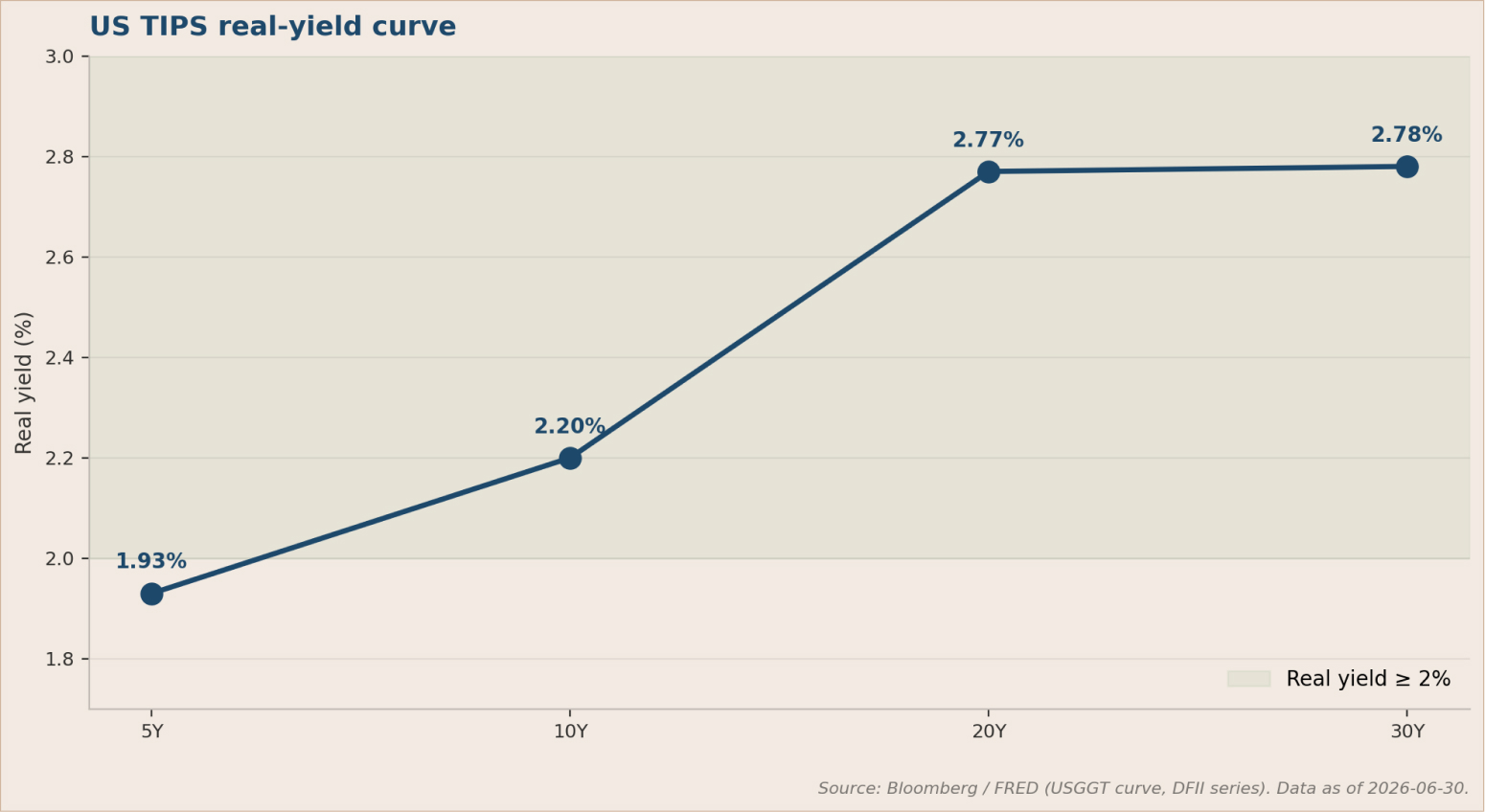

The 10-year Treasury Inflation-Protected Security (TIPS), a government bond whose value adjusts with inflation, currently yields 2.20% above whatever inflation turns out to be over the next decade. The bond market's implied inflation forecast for that same period sits at 2.24% annually. Together those figures suggest that patient investors in longer-term government bonds are being paid a real return for the first time in years.

One reassuring note is that bond market volatility is currently low, suggesting that traders are not bracing for any sudden or disruptive shift in Federal Reserve policy in the near term [25].

Treasury Inflation-Protected Securities (TIPS) & inflation expectations

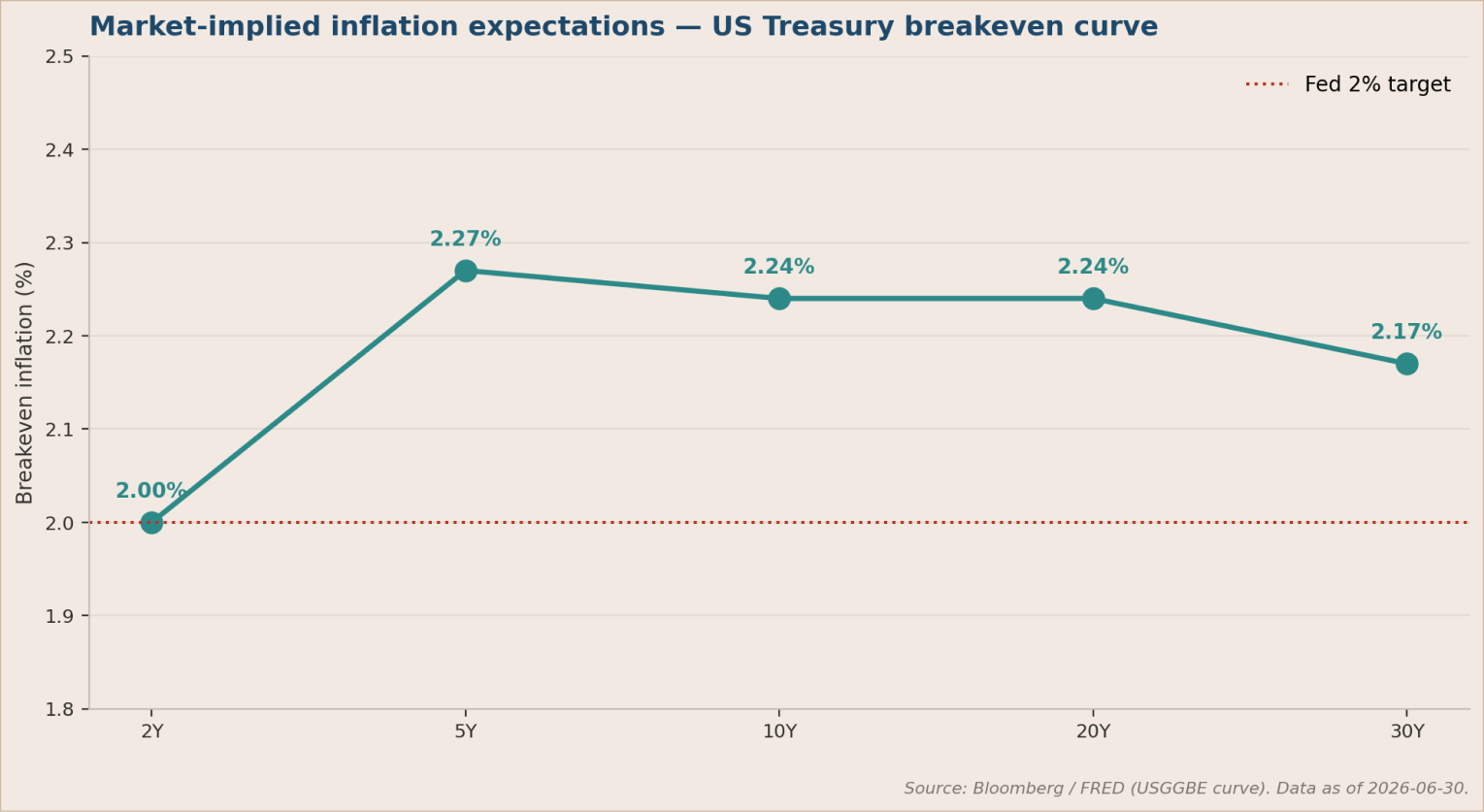

The bond market is telling a consistent story about inflation: it expects prices to keep rising at a rate above the Federal Reserve's 2% target, and that expectation has not been coming down.

One way to read inflation expectations from financial markets is to compare the yields on regular government bonds against those on inflation-protected bonds of the same maturity. The gap between them reflects what bond investors collectively expect inflation to average over that period. Currently, those implied forecasts range from 2.01% over the next two years to 2.26% over the next five and twenty years [26]. Every single one of those figures sits above the Fed's 2% target.

A separate measure, which the Federal Reserve pays particular attention to because it filters out short-term swings in energy prices, looks at where markets expect inflation to run during the five-year period that begins five years from now. That figure currently stands at 2.22% [27]. A further measure, derived from inflation swap contracts that institutional investors use to hedge against rising prices, puts the ten-year inflation outlook at 2.38% [28].

Taken together, these figures point in the same direction. Earlier this year, markets had been pricing in a fairly optimistic scenario in which inflation would steadily return to the Fed's 2% target. That story has lost credibility. The bond market is no longer willing to bet that inflation is durably heading back to 2%, and the Fed's rate decisions in the months ahead are likely to reflect that reality.

The return above inflation that TIPS currently offer is historically high. Across maturities ranging from two to thirty years, those returns run from roughly 1.93% to 2.76% above inflation [29]. The ten-year TIPS, at 2.20% above inflation, is at a level that has not been sustained since before the 2008 financial crisis.

That matters because it changes the calculus for long-term investors, particularly those holding bonds in retirement accounts and other tax-sheltered structures. To put the numbers in concrete terms: an investor in the 24% federal income tax bracket who buys a ten-year TIPS today would earn a return of approximately 1.19% above inflation after tax if inflation registers 2% over the remaining life of the bond. That is still higher than the long-run after-fee return that cash has historically delivered, and it compares favorably with the long-run premium that global stocks have historically earned over safe assets, once fees are accounted for.

There is one meaningful complication, however. TIPS adjust with the Consumer Price Index, which includes energy prices. The sharp drop in oil prices during June will, if sustained, drag reported inflation lower in the months ahead, which in turn reduces the inflation adjustment that TIPS investors receive. That headwind is the primary reason we are holding a neutral rather than overweight position in TIPS for now, despite the otherwise attractive yields on offer.

Additional market-implied inflation gauges: 10Y inflation swap 2.38%; 30Y inflation swap 2.31%; 5Y5Y forward breakeven 2.22%. All three sit 20-40 bp above the Fed's 2% target, suggesting the market is not pricing durable disinflation.

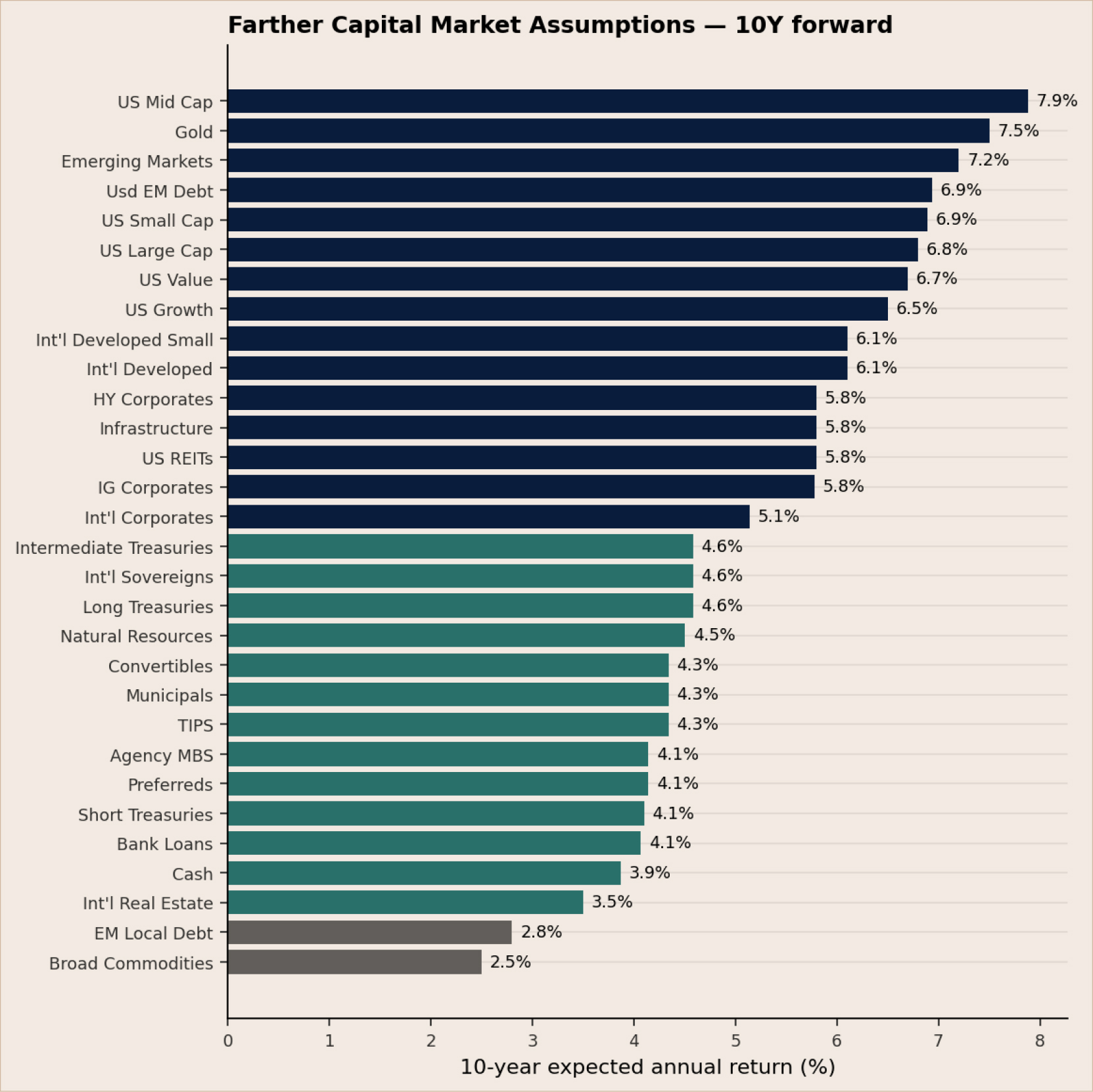

Capital market assumptions: 10-year forward

The chart below shows our best estimates for how different categories of investments are likely to perform over the next decade, ranked from highest to lowest expected annual return [30].

These estimates are not simple guesses. They are built by combining three different analytical approaches: long-run historical return data, adjustments for where we currently are in the economic cycle, and forward-looking signals implied by current market prices. The weight given to each approach varies depending on the asset class being assessed, since some categories of investment are better suited to one method than another.

No forecast of this kind should be treated as a guarantee. Markets are unpredictable over short periods, and actual returns will inevitably differ from these estimates. What this framework provides is a disciplined, consistent basis for comparing the long-term return potential of different investments against one another, which in turn informs how we allocate across asset classes in our model portfolios.

Commodities, currencies & alternatives

Oil prices fell sharply in June, with U.S. crude dropping 20.4% to $69.50 per barrel and the international benchmark declining similarly to $72.92. Gold fell 11.4% to $4,038.50 per ounce, though it remains 22.1% higher than a year ago. Silver dropped 21.6% for the month but is still up 65.9% over the past year. Bitcoin fell 20.6% to $58,642 and is now 45.5% below where it stood twelve months ago. A broad index tracking commodity prices across energy, metals, and agriculture fell significantly for the month as well [30].

It is worth being clear about what drove these declines. The selloff in oil, gold, and related assets was not caused by a weakening global economy or falling demand for raw materials. It was caused by the resolution of the Middle East conflict, which removed the geopolitical anxiety that had been pushing those prices higher in the first place. That is an important distinction: falling oil prices in this context reflect a reduction in fear rather than a deterioration in economic conditions.

On currencies, the U.S. dollar strengthened 2.1% against a basket of major currencies during June. The euro fell 2.1% against the dollar and the British pound also weakened. The Japanese yen weakened about 2% against the dollar [32], moving in line with the broader dollar rally. Despite Japan’s central bank gradually raising its own interest rates, carry-trade dynamics and yield differentials continue to favor dollar-denominated assets.

Where major markets stand

About this commentary

The Farther Investment Strategy team

The Farther Investment Strategy (IS) team serves as a specialized support arm for Farther Advisors, providing institutional-grade portfolio analysis, investment due diligence, and actionable market intelligence. The team operates independently of individual advisor practices. This structural independence ensures that the views expressed in this commentary reflect a consistent, firm-wide perspective grounded in objective, rigorous research rather than any single business development objective.

As part of our commitment to delivering client-ready investment insights, this monthly market commentary is designed to help advisors articulate a compelling, data-driven investment narrative. Produced on a monthly cadence, each issue is rigorously reviewed to ensure alignment with Farther's overarching capital market outlook and to provide actionable assessments of how current economic and policy trends impact portfolio positioning.

How to use this commentary

This commentary is written to be accessible to informed investors who want to understand the forces shaping their portfolio. Clients do not need a finance background to engage with it. Each section includes a plain-language summary of the key takeaway, and the document is structured to be read in full or by section depending on the reader’s interest.

Clients reading this commentary should keep a few things in mind:

- It reflects firm-level views, not your individual plan: The positioning described here represents Farther’s broad strategic stance. How it applies to your specific portfolio depends on your goals, time horizon, and risk profile. Your advisor is the right person to connect these views to your personal financial plan.

- It is a snapshot, not a prediction: Markets change, and so does our positioning. This commentary captures our best thinking as of the publication date. We update it monthly and will communicate material changes as they occur.

- The ‘In plain terms’ callouts are written for you: Throughout the document, tan-shaded callout boxes summarize the most important takeaway from each section in plain language. If you read nothing else, read those.

- Questions are welcome: If something in this commentary raises a question about your portfolio or our investment approach, reach out to your Farther advisor. These conversations are exactly what this document is designed to support.