The combination of both positive and negative economic developments in July and early August caused a mixed financial market response. As we approach Labor Day and enter the fall season, we anticipate that additional events may influence the markets.

Positive Developments

- Q2 corporate earnings generally outperformed expectations. Large-cap technology companies had both outperformers (Alphabet, Amazon, and Meta) and underperformers (Apple and Microsoft).

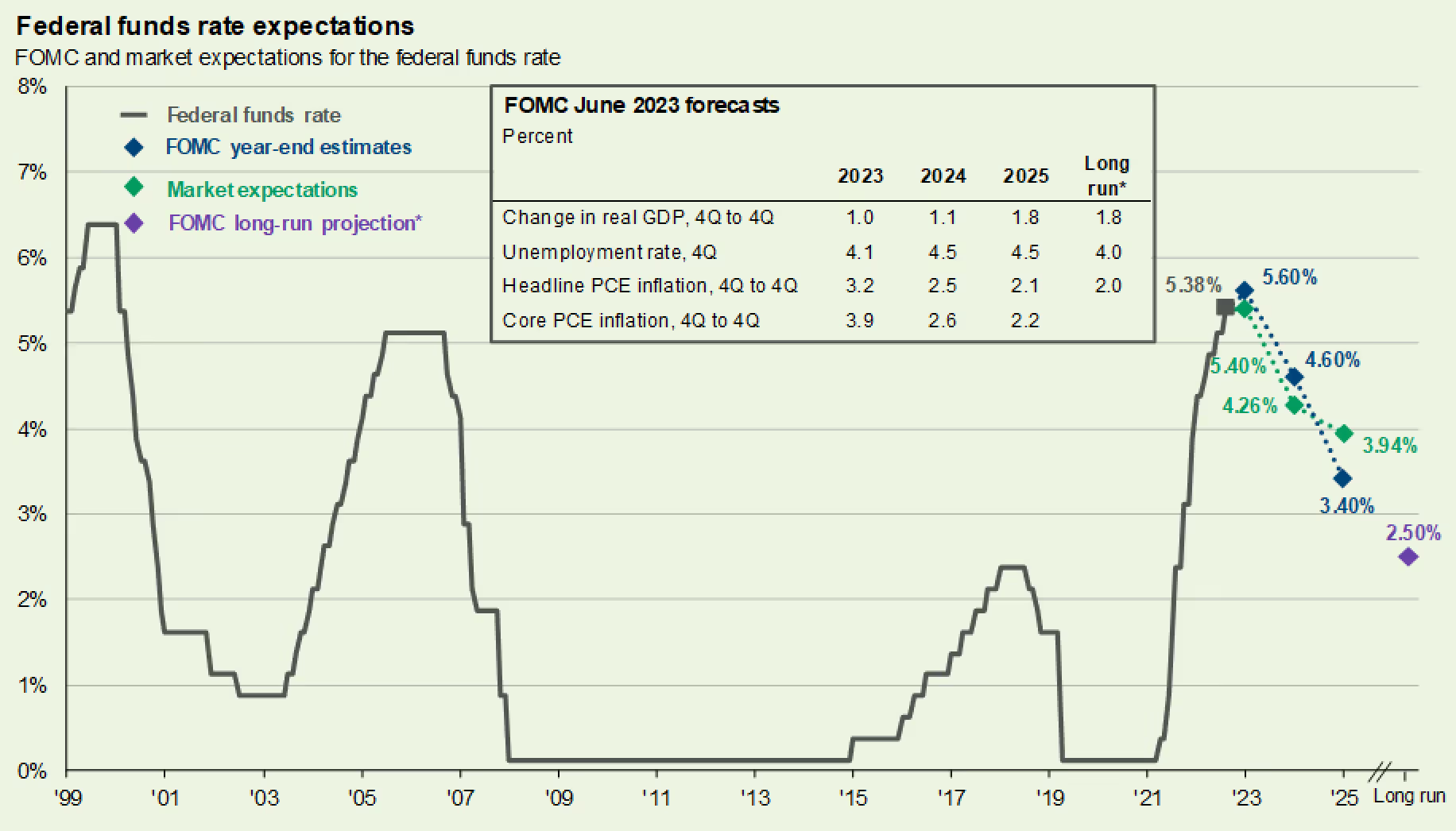

- The Federal Reserve raised the target Federal Funds 0.25% to 5.50% on July 27th, as expected, after a pause in hikes in June. Federal Reserve officials have indicated that there may be one more 0.25% increase this year.

- The U.S. CPI inflation rate moderated to 3.0% year-over-year through June and 3.1% through July, as reported on August 10th. While still above the Federal Reserve’s 2% inflation target, these latest figures show notable progress from the 9.1% peak in June 2022.

Negative Developments

- August 1: Fitch Ratings downgraded the U.S. debt to a credit rating of AA+ from AAA – citing issues including governance, rising deficits, and a debt-to-GDP ratio.

- August 7: Moody’s downgraded the credit ratings of 10 regional banks and placed another 6 banks’ ratings on watch, citing reasons that I have previously expanded upon: the pressure on profitability from high short-term and long-term interest rates, and their concentration in commercial real estate lending, relative to the country’s largest banks.

Financial Market Response

- Stock markets peaked for the year at the end of July. Markets then sold off in August after the Fitch downgrade, Apple’s disappointing earnings, and Moody’s bank downgrade.

- Despite the August selloff, however, the S&P 500 was still up 0.5% since the end of June and 17.4% for the year through August 11th. Volatility as measured by the VIX index has increased from a low of approximately 13 in late July to 17 in early August (following the Fitch downgrade), prior to settling in at approximately 15 on August 11th (still notably below the 20+ volatility levels seen in 2022). The 10-year U.S. Treasury Note’s yield rose to 4.16% on August 11th from 3.82% on June 30th.

Upcoming Events

- The NVIDIA earnings report on August 23rd may reignite the generative AI boom that fueled the rally in many of the mega-cap tech stocks this year.

- The Kansas City Federal Reserve Bank’s Jackson Hole Economic Policy Symposium will be hosted on August 24th-26th. Last year’s short, eight-minute speech by Federal Reserve Chairman Jerome Powell left no doubt regarding the Federal Reserve’s intent to raise short-term interest rates to aggressively fight inflation. Given the steep increase in interest rates over the last 17 months and the falling inflation rate, this year’s speech is likely to be less dramatic. It should, however, offer a clear view of the Federal Reserve's perspective on monetary policy and future rate increases.

- The next U.S. jobs report will be released on September 1st, followed by the CPI inflation rate on September 13th.

- The Federal Reserve’s next FOMC meeting concludes on September 20th.

A Final Thought on Fixed Income

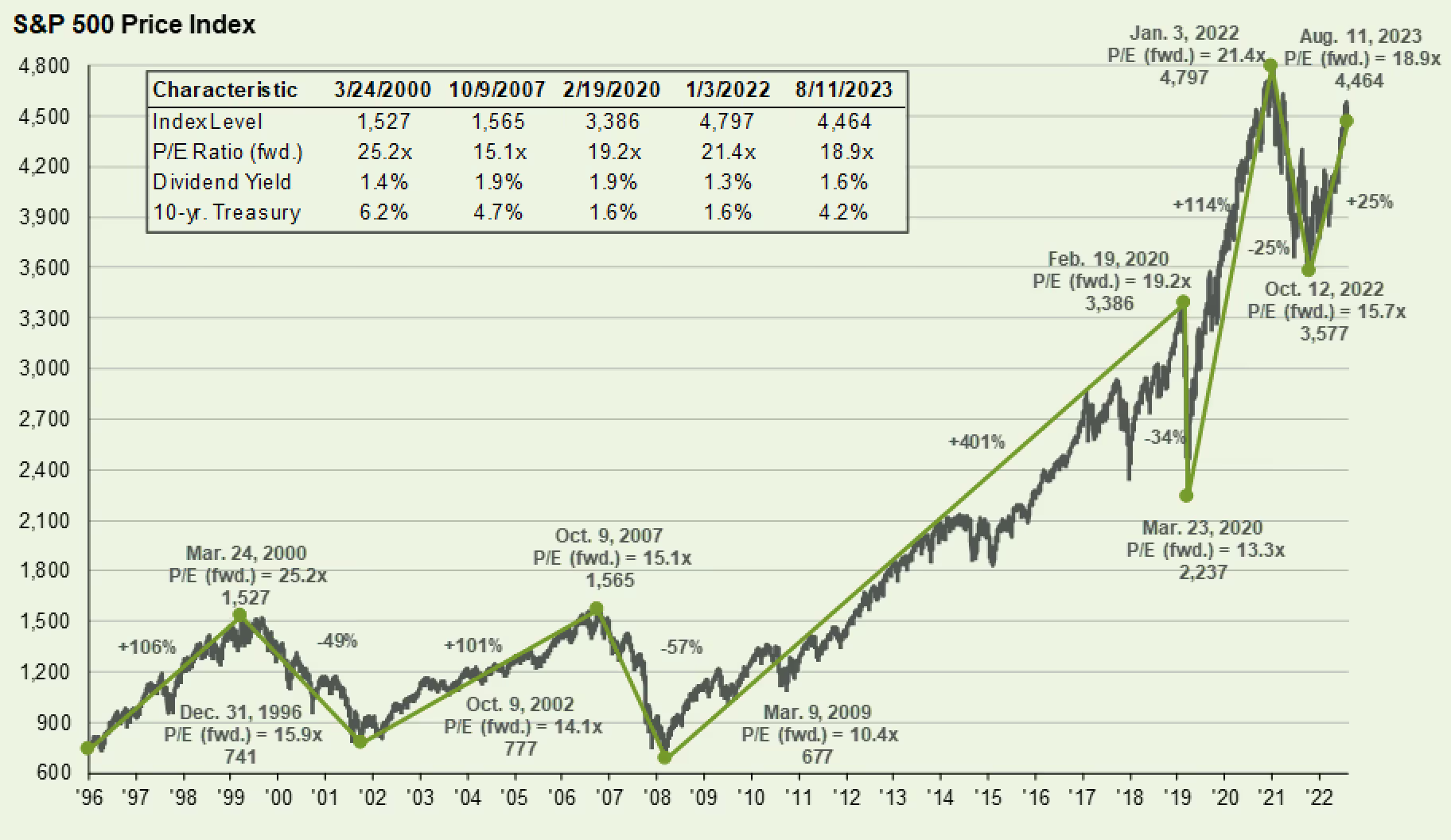

Source: Compustat, FactSet, Federal Reserve, Refinitiv Datastream, Standard & Poor’s, J.P. Morgan Asset Management. Dividend yield is calculated as consensus estimates of dividends for the next 12 months, divided by most recent price, as provided by Compustat. Forward price-to-earnings ratio is a bottom-up calculation based on IBES estimates and FactSet estimates since January 2022. Returns are cumulative and based on S&P 500 Index price movement only, and do not include the reinvestment of dividends. Past performance is not indicative of future returns.

I wanted to conclude this piece with some observations about fixed income, particularly relative to stocks. As the above chart illustrates: the S&P 500 has rallied 25%, since the S&P 500 low on October 12, 2022, through August 11, 2023. The forward P/E ratio on the S&P 500 rose from 15.7 to 18.9. Stated differently, the earnings yield (the inverse of the P/E ratio) on stocks fell from 6.4% to 5.3%. At the same time, 10-year US Treasury Notes yields rose slightly from 3.9% to 4.16%.

In the long term, stocks will almost certainly prove to be a better compounder of wealth. Nonetheless, the relative attractiveness of fixed income is compelling. Many investors have invested in short-dated U.S. T-Bills, whose yields have risen along with the Federal Funds rate. The risk of investing solely in short-dated US T-Bills is that interest rates may change when the bills mature, and you reinvest at lower yields (also known as reinvestment risk).

Source: Bloomberg, FactSet, Federal Reserve, J.P. Morgan Asset Management. Market expectations are based off of the respective Federal Funds Futures contracts for December expiry. *Long-run projections are the rates of growth, unemployment and inflation to which a policymaker expects the economy to converge over the next five to six years in absence of further shocks and under appropriate monetary policy. Forecasts are not a reliable indicator of future performance. Forecasts, projections, and other forward-looking statements are based upon current beliefs and expectations. They are for illustrative purposes only and serve as an indication of what may occur. Given the inherent uncertainties and risks associated with forecasts, projections, or other forward-looking statements: actual events, results, or performance may differ materially from those reflected or contemplated.

Both market participants and the Federal Reserve expect lower short-term interest rates in 2024 and 2025, as indicated in the above chart. While the precise timing of falling rates is difficult to predict, the fixed income markets are likely to respond positively. By extending maturities from T-Bills, you can lock in attractive yields for multiple years.

For example, as of August 11th: 2-year U.S. Treasury Notes are yielding ~4.9%, 3-year U.S. Treasury Notes are yielding ~4.6%, and 5-Year U.S. Treasury Notes are yielding ~4.3%.

Please speak to your advisor, if you would like to learn more about extending the duration of a portfolio that is heavily invested in short-term cash or fixed income.

Lauren Moone, CFA, contributed to this piece.