Deciding when to retire? The right timing depends on your financial readiness, health status, and personal goals.

Your birth year determines your full retirement age for Social Security benefits, directly affecting how much you'll receive.

This guide examines key factors to consider when choosing your retirement age, including financial security assessments, healthcare considerations, and personal readiness strategies to ensure your retirement timing aligns with both your financial needs and lifestyle aspirations.

Key Takeaways

- Your best retirement age depends on money, health, and personal dreams.

- Retiring early means more free time but requires a large savings account. Waiting to retire can grow your funds but might limit personal time.

- Health plays a huge role in deciding when to retire. Good health lets you work longer; bad health might force an early retirement.

- Personal goals impact when you retire. What makes you happy should guide your choice.

- Talking to a financial advisor helps make sense of your options for retirement planning.

Factors to Consider When Deciding Retirement Age

Deciding on the best retirement age involves considering your finances, health, and how you envision your life after work. These factors are crucial in making this significant choice.

Financial stability

Your financial situation plays a major role in determining the ideal retirement age. If you have a 401(k), savings, or another retirement plan, you might be well-positioned. It's important to know how much money will be needed each month.

Social Security benefits can start as early as age 62. Waiting longer to take these benefits increases the monthly amount you receive. However, it's crucial to understand that claiming these benefits at age 62 results in a permanent reduction of up to 30% compared to waiting until the full retirement age of 67, based on birth year. Conversely, delaying benefits past the full retirement age up to age 70 can increase your monthly payouts by approximately 8% for each year you delay. Health insurance costs and investment performance also play a role in this decision.

Health and wellness are also crucial factors to consider when picking a retirement age.

Health and wellness

Health plays a big role in deciding when to retire. Working longer may be feasible and enjoyable if you are in good health, but consider that health status can unexpectedly change, complicating planned retirement dates and potential healthcare costs, which tend to increase with age.

If someone has a serious condition, they might need to retire earlier than planned.

Wellness also involves mental health. People who work often get social interaction, which keeps their spirits up. Retiring early gives free time but may limit these interactions. Balancing time off with staying active is key for both physical and mental wellness.

Finding the right age to call it quits depends on staying healthy and happy at work or in retirement.

Personal goals and lifestyle preferences

Your personal goals play a big role in choosing your retirement age. Many people want to travel, spend time with family, or start new hobbies after they stop working. These desires can influence when you decide to retire.

Lifestyle choices matter too—some enjoy staying busy in their jobs while others prefer a more relaxed pace.

Think about what makes you happy and fulfilled. Engaging a Certified Financial Planner (CFP®) or a fiduciary financial advisor is advisable to ensure your retirement planning aligns with your personal goals and financial resources. If you aim for financial independence, it may make sense to save more now and retire later.

Finding balance is key before shifting gears into the next stage of life.

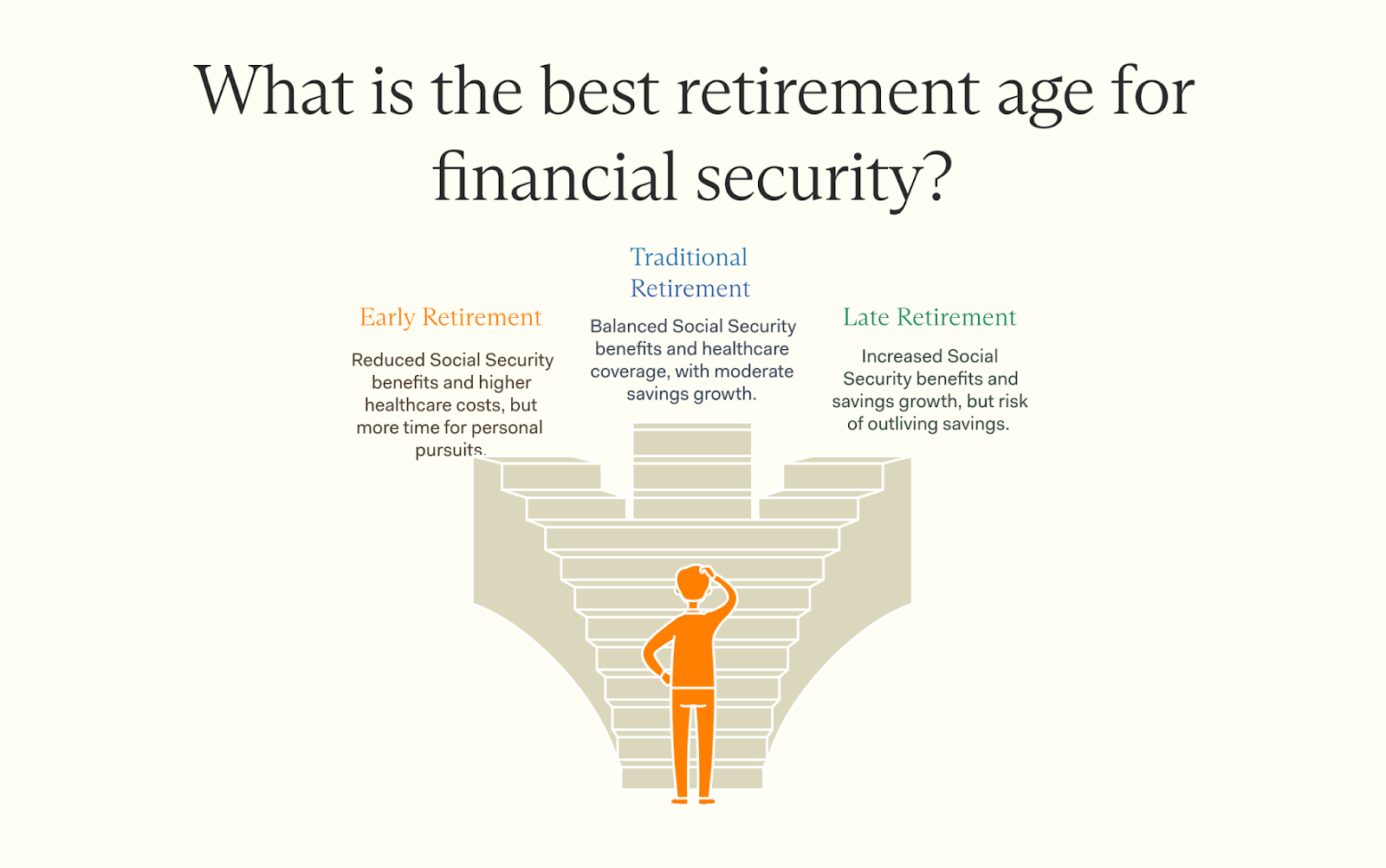

Pros and Cons of Early Retirement

Early retirement can feel like a dream come true. You get more free time, but it also comes with tough choices about money and health.

Advantages of retiring in your early 60s

Retiring in your early 60s comes with several benefits. You gain more time to enjoy life, but it's important to consider financial trade-offs such as the potential reduction in Social Security benefits and the need to have sufficient retirement savings to cover a potentially longer retirement period. Many people use this time for travel, hobbies, or family. It can lead to better health and happiness as you relax and focus on personal interests.

Financially, retiring early might allow you to manage your savings strategically. However, withdrawing from retirement accounts like a 401(k) before age 59½ could incur a 10% penalty unless exceptions apply, and tapping into these funds early can also reduce their longevity. Even though you might plan to draw from these accounts initially and start receiving Social Security benefits later, it's essential to consider how early withdrawals can impact your financial stability in the long term.

This way, your total income may rise over the years. Plus, retiring earlier allows for more mental stimulation through new experiences before age-related challenges arise.

Challenges of early retirement

Early retirement has its hurdles. First, you may face financial strain. Your retirement savings must last longer if you retire early. A longer period without work means you need a bigger nest egg to cover your expenses.

Health can also be an issue. Some people feel lost without the daily routine of work. Transitioning away from a job takes time and adjustment. Moreover, retiring early when you have fewer high-earning years could mean smaller monthly benefits from programs like Social Security, as benefits are calculated based on the highest 35 years of earnings, potentially lowering your average indexed monthly earnings and your benefit amount.

Lastly, many retirees miss social connections from work life, leading to feelings of loneliness once you retire early. The loss of workplace social interactions can be mitigated by engaging in community activities, volunteering, or joining social groups to help maintain social connections and support mental health.

Pros and Cons of Traditional Retirement

Retiring in your mid-60s can mean steady income and more time for fun. But it may also lead to boredom or a lack of purpose if you're not ready for that next chapter.

Benefits of retiring in your mid-60s

Retiring in your mid-60s offers many benefits. Most people have built a solid financial base by this age. This includes savings from a 401(k) or other retirement plans, which can provide a good benefit amount.

Many choose to stop working before they reach full Medicare eligibility, making the timing crucial.

Health is another factor to consider. People often feel healthier in their 60s than later on. They can enjoy life without work stress. Traveling and spending time with family become easier too.

Early retirement allows for more leisure activities that improve wellness and happiness.

Potential drawbacks of traditional retirement

Traditional retirement in the mid-60s comes with several challenges. One major downside is financial strain. Many rely on savings, like a 401(k), but those funds may not last long enough.

Some people find it hard to adjust to a fixed income after years of earning.

Health can also be a concern. Aging brings different health challenges that can lead to rising medical costs, which might affect finances even more. Delaying retirement can seem wise, yet it comes with its own stress—like a longer work life and less time for personal goals or hobbies.

Balancing all these factors is key for anyone making this big decision.

Pros and Cons of Late Retirement

Many people find benefits in retiring after 65. It can mean more savings and better health care options. But, staying longer at work can also be hard on your body and mind. Plus, you might miss out on time with family and friends.

Advantages of retiring after 65

Retiring after 65 offers several benefits. First, it gives you more time to grow your retirement savings. This means a larger 401(k) or other retirement accounts. More money can lead to greater financial stability later on.

Staying in the workforce longer may also improve your health and wellness. Many people find purpose in their jobs, which keeps them active and social. Working past 65 helps some avoid boredom or loneliness that can come with early retirement.

Insurance products may offer better deals for those who delay as well. In summary, waiting allows you to enjoy more advantages for future years ahead!

Challenges of delaying retirement

Delaying retirement has some hurdles. Many people rely on their 401(k) or other retirement investments for income. If you wait too long, those funds might lose value before you need them.

Health issues can also arise with age. Being unwell can make it hard to continue working.

Working longer may not always mean more money. Taxes can eat into your earnings, reducing what you take home. Some folks miss out on enjoying life while waiting to save more. Balancing these factors is key.

Hire a Financial Advisor

The ideal retirement age depends on your financial readiness, health, and lifestyle goals. While some aim for early retirement in their 50s, others wait until full Social Security benefits kick in at 67. Understanding your savings, expected expenses, and desired quality of life is key to making the right choice.

Thinking about retirement? Speak with a Farther financial advisor today to determine the best retirement age for you!

Conclusion

Choosing the right retirement age is a personal decision that shapes your future. Balancing finances, health, and lifestyle goals is key—early retirement offers freedom but may bring financial challenges, while waiting can provide greater security.

Take the time to plan wisely—your future self will thank you! If you need guidance, a financial advisor can help you navigate your options and build a strategy that fits your dreams. No matter where you are in the journey, it's never too late to start planning for a fulfilling, worry-free retirement!

FAQs

1. What factors should I consider to determine the best age to retire?

Many factors come into play when deciding the ideal retirement age. It includes your financial readiness, health status, and personal goals. Consulting with a registered investment advisor may help you make an informed decision.

2. Can delaying my retirement benefit me financially?

Yes, it can make sense to delay taking out from your 401(k) or other retirement savings as they continue to grow tax-deferred. Also, waiting might increase your Social Security benefits.

3. Is there any risk involved in investing for retirement?

Investing always carries some level of risk. While FDIC-insured deposits, such as savings accounts and certificates of deposit (CDs), are protected up to $250,000 per depositor, per insured bank, for each account ownership category and backed by the full faith and credit of the U.S. government, non-deposit investment products offered by FDIC-insured banks are not covered by FDIC insurance and can lose value due to market fluctuations.

4. How can financial advisors assist in planning my retirement?

Financial advisors, including those registered as investment advisers (RIAs) with the SEC or state regulators, or those associated with broker-dealers registered with the SEC and FINRA, offer expert advice on investing wisely for your business or personal needs during post-retirement years. It's important to verify the credentials and registrations of a financial advisor to ensure they meet your specific needs.

5. Do third-party insurance carriers have a role in my retirement planning?

Indeed! Third-party insurance carriers often provide annuities or life insurance products that could supplement income in retirement while offering potential death benefits. However, it's crucial to understand that these products are not FDIC-insured, carry their own risks and fees, and require a thorough review of the terms, conditions, and financial stability of the issuing insurance company before incorporation into your retirement plan.