Many of our clients welcome the holiday season as a time of generosity to support their favorite charities and causes close to their hearts. One element of our work as advisors includes collaborating with our clients to help determine their philanthropic goals and the most appropriate strategy to execute those goals, in conjunction with their overarching financial plan and investment portfolio.

As we approach the end of the year, we would like to take the opportunity to outline a few ways to be strategic with your giving, so that both the charitable impact and associated tax benefit are maximized.

This piece outlines 5 gifting strategies and highlights the best time to employ each one:

- Gifting cash

- Gifting securities and appreciated assets

- Using a Donor-Advised Fund

- Using Charitable Remainder Trusts

- Using IRA RMDs to gift to charity (tax-free)

Strategy 1: Gifting cash

Writing a check or using Venmo to support a friend’s fundraiser is often the quickest and simplest way to make a charitable donation.

When to apply this strategy:

- You are looking to make smaller donations that have an immediate impact.

For larger gifts, the following strategies are often better for maximizing the donors’ charitable impact and tax-efficiency.

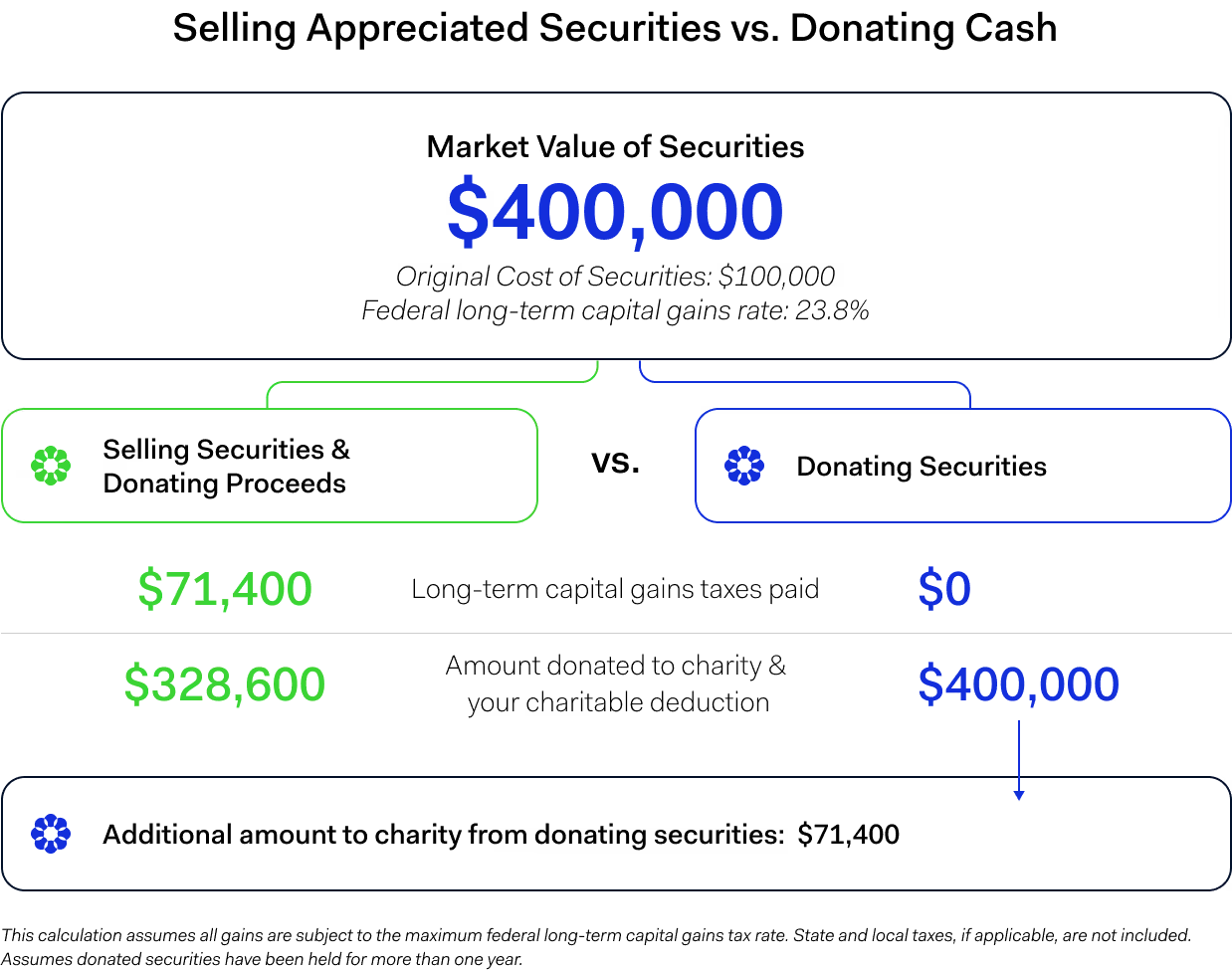

Strategy 2: Direct donation of appreciated assets

When you donate an appreciated asset like stock (rather than cash), the recipient receives the full benefit of the increased value of the gift. Donors receive a charitable deduction for both the full value of their gift and avoid capital gains tax on the appreciated assets.

When to apply this strategy:

- You have appreciated stock positions with large unrealized taxable gains. Other appreciated assets like real estate can be gifted, as well.

- For larger charitable gifts.

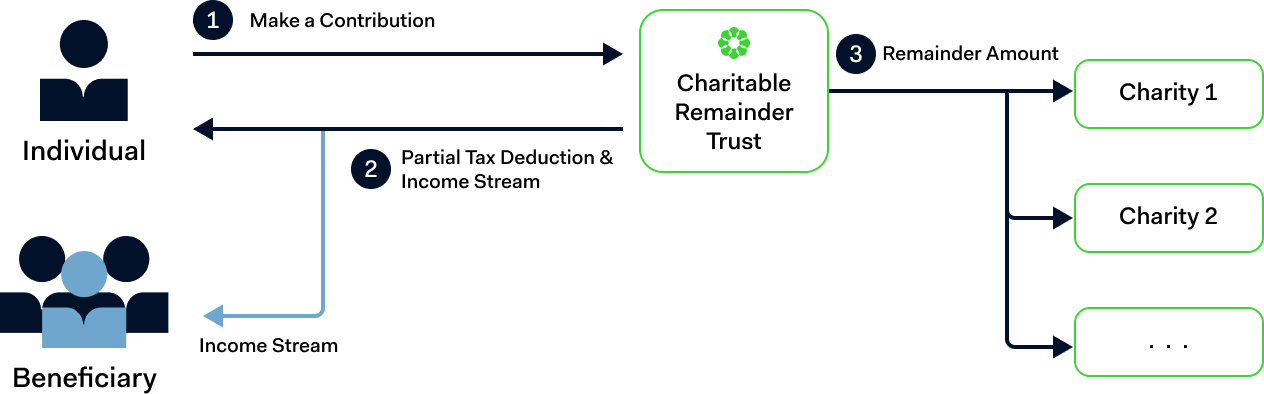

Strategy 3: Donation to a Donor-Advised Fund

A Donor-Advised Fund (DAF) is a giving account set up with a public charity. It enables donors to make a charitable contribution of cash or appreciated assets and receive a tax deduction in the year of the gift, while retaining the ability to make grants to their desired charities from their fund account over time. Donors can also manage how the fund account is invested.

Grants can be made over time to multiple organizations. In many ways, a DAF serves the role of a private foundation, but without the administrative expenses and burdens.

When to apply this strategy:

- For the donation of appreciated assets in one year, in order to offset a large taxable event.

- For the creation of an annual giving plan of appreciated securities. You can donate your desired charitable amounts each year from your most appreciated securities in your investment portfolio, and then make grants to your desired charities in the following year(s).

Donor Advised Funds can also be used creatively to engage the entire family in philanthropy on an annual basis. Each family member can select a charity and an amount to support each year to install charitable giving toward important causes in their lives.

Strategy 4: Use of a Charitable Remainder Trust

A Charitable Remainder Trust (CRT) is a special type of trust designed to provide an income stream to the donor or beneficiaries, with the remaining assets going to a charity or charities. The donor receives a partial charitable donation in the year that the trust is funded, based on the value of the assets given adjusted for the value of the income payments to the donor.

A key difference to note between a CRT and a Donor Advised Fund (DAF): with a DAF, you can donate the assets at any point in time; under the terms of a CRT, however, any named charity(ies) only receive assets at the end of the trust term (20+ years or your lifetime).

When to apply this strategy:

- You have appreciated assets that you would like to donate at a future date, but would benefit from a large tax deduction now.

- You have a large appreciated stock position in a single security. Donating it to the charitable trust allows you to sell and diversify the investments without paying tax on the gains, and benefitting from the income stream over your lifetime.

Strategy 5: Using IRA RMDs to give to charities in retirement

IRA owners must begin taking a Required Minimum Distribution (RMD) at age 73. These distributions are taxable as income, and individuals may not want to take them if they have sufficient other sources of income – or if taking the distribution would put them in a higher tax bracket, impacting Social Security and Medicare benefits.

Fortunately, a Qualified Charitable Distribution (QCD) allows anyone 70 ½ and older to give up to $100,000 per year of their IRA required distribution to one or more charities.

When to apply this strategy:

- You have sufficient income in retirement from non-IRA sources.

- The benefit of reducing your taxable income is greater than the tax benefit of making a charitable donation from non-IRA assets.

There are several ways to give to charities and maximize your tax benefit while doing so. A thoughtful ongoing conversation with your advisor about philanthropic planning can improve both your overall financial situation – and more importantly, your impact on the causes most important to you.

David Darby, CFA contributed to this piece.