Background

If you contributed to a Traditional IRA over the span of your working years, you probably did so with the expectation of enjoying the income it would provide during retirement. In fact, the primary benefit of a Traditional IRA is its tax-advantaged status: the IRS permits you to defer taxes on both contributions and earnings in the account until you start to make withdrawals.

Under current IRS rules, you are required to take annual withdrawals – called Required Minimum Distributions, or RMDs – from your Traditional IRA once you reach age 73. (In December 2022, Congress passed legislation that raised the age at which you have to start taking RMDs, from 72 to 73.) In any given year, the RMD is subject to taxation as ordinary income. Beware: failure to take the RMD each year can result in a significant penalty!

Oddly enough, for some people, the taxable income generated from an RMD can create a problem: the additional income may push them into a higher marginal tax bracket. This, in turn, could have an adverse impact on Social Security payments, Medicare benefits, or both.

Qualified Charitable Distributions

Fortunately, there is a tax-smart solution available to those who are charitably inclined. Under IRS rules, a donor can direct the custodian of a Traditional IRA to transfer all or part of the annual RMD – up to $100,000 for an individual and up to $200,000 for a married couple filing jointly – to a qualified public charity1. By making this type of gift – a Qualified Charitable Distribution (QCD) – the donor will not owe any income tax on the amount of the QCD.

Organizations that qualify for public charity status include homeless shelters, animal welfare agencies, churches, schools, hospitals, medical research organizations and most publicly supported organizations. The IRS site has a Tax-Exempt Organization Search (TEOS) tool that may be helpful in identifying appropriate charities and nonprofits (www.irs.gov/charities-and-nonprofits).

(Please note: private foundations, donor-advised funds and supporting organizations are not considered to be qualified public charities and therefore do not qualify as recipients of QCDs.).

For most people, making a QCD from a Traditional IRA is a win-win strategy. Because the QCD goes directly to a qualified charity, the donor does not have to report the QCD as taxable income. And because the QCD is excluded from taxable income, adjusted gross income (AGI) is reduced – which reduces your tax liability and may in turn reduce the portion of Social Security benefits received that are taxable. Also noteworthy: you can enjoy the benefits of a QCD whether or not you itemize deductions on your tax return.

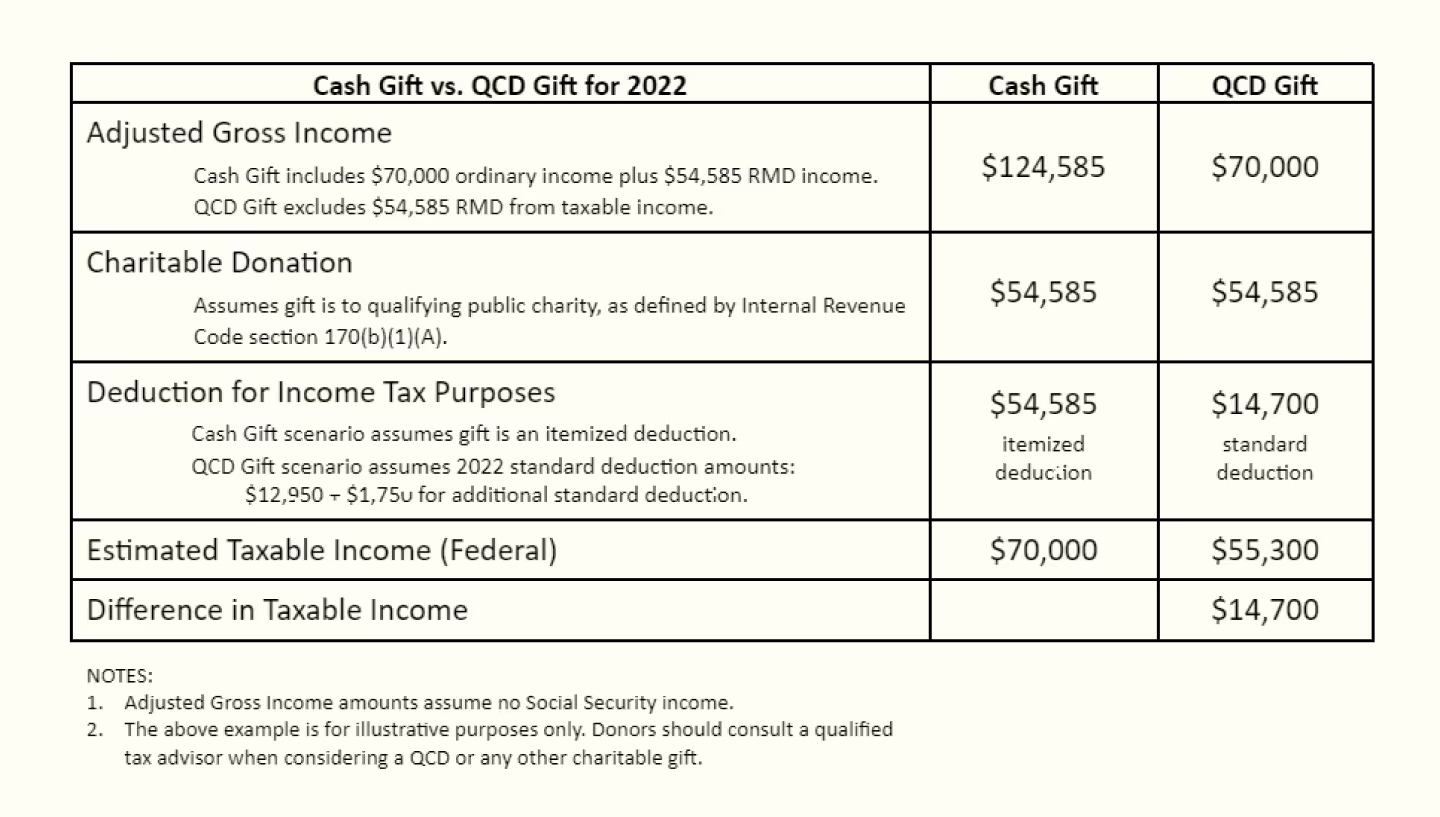

The following example illustrates the income tax benefit of making a QCD gift versus a cash gift.

Qualified Charitable Distribution: Example

In 2022, Sheila (age 77 and a widow) had ordinary income of $70,000; her filing status is “single” for income tax purposes. The estimated RMD in 2022 from her Traditional IRA, valued at $1.25 million, is $54,585 (1,250,000 divided by the IRS “distribution period” of 22.9 years). The table below compares the income tax effect of making a QCD gift of $54,585 versus a cash gift of $54,585.

At Farther, we strive to enhance after-tax returns for our clients by implementing a variety of tax-smart and tax-efficient strategies.

I would be delighted to discuss this strategy, as well as other strategies that could fit your unique needs. Please feel free to schedule time with me here.

-

1A qualified public charity is defined under Internal Revenue Code section 170(b)(1)(A).