Stocks and bonds both experienced double-digit declines in 2022. And while we have seen continued volatility in 2023, there are signs pointing to an eventual recovery. We recommend making some tactical adjustments to portfolios now, in order to be poised to participate when markets start to trend back upward.

As a reminder, our overall investment approach is to set long-term portfolio allocations for each client; assess current market conditions quarterly; and make adjustments to optimize returns, while mitigating investment risk.

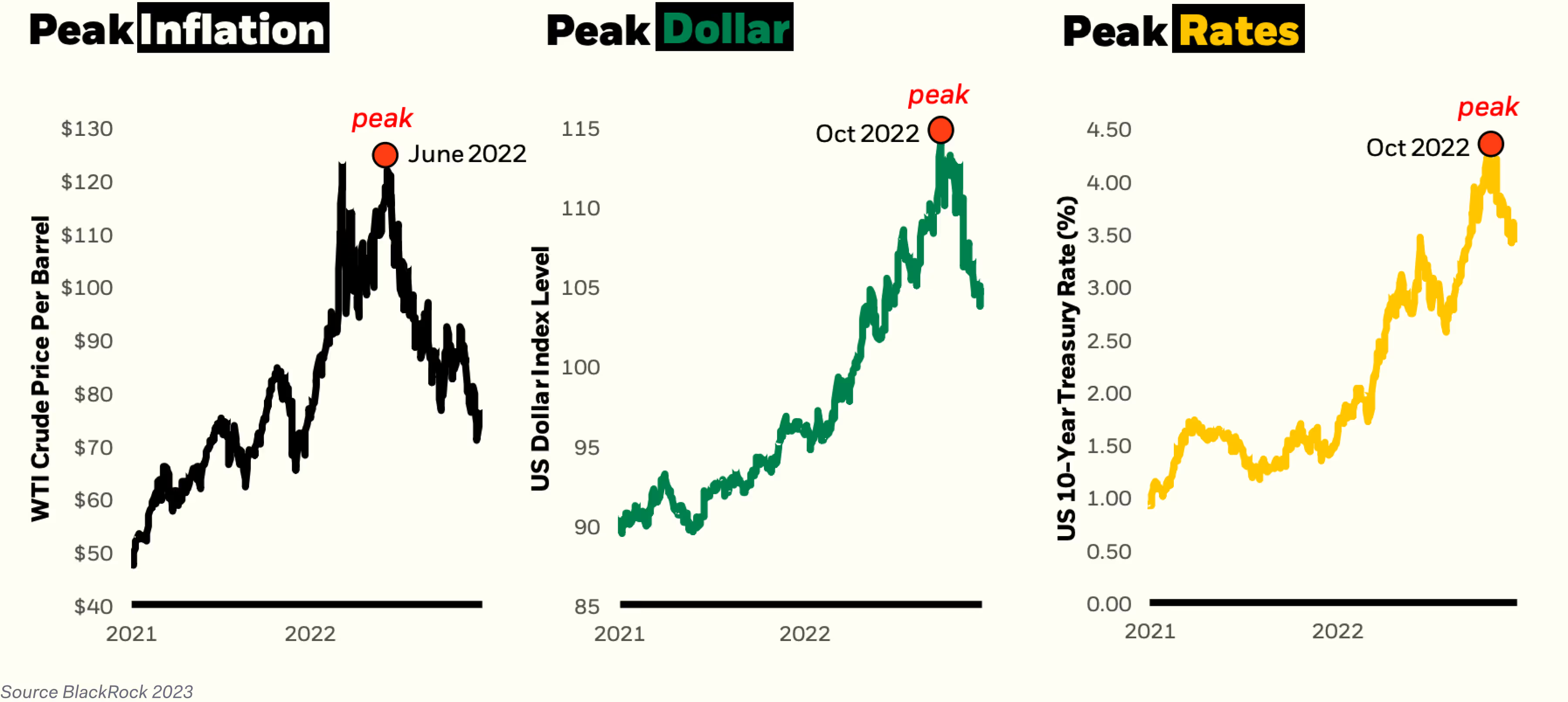

For Q1, we recommend the recalibration of portfolios for a potential environment that has passed peak inflation, a peak U.S. dollar, and peak long-term treasury bond interest rates. If this trend continues: there is the possibility that the Fed will halt additional rate hikes, while real economic growth is still positive in the U.S.

Consequently, we begin targeted efforts to gently shift the risk in our portfolios across both stocks and bonds. The confidence to make these moves stems from our belief that inflation has peaked – and will likely decelerate at a sufficient pace over the coming months, convincing the Fed to eventually pause its rate-hiking campaign. Softening U.S. inflation and less Fed hawkishness may also mean a peak in the strength of the U.S. dollar – which could make overseas assets particularly attractive on a tactical basis.

Inflation, the Dollar, and Treasuries Peaked Last Year

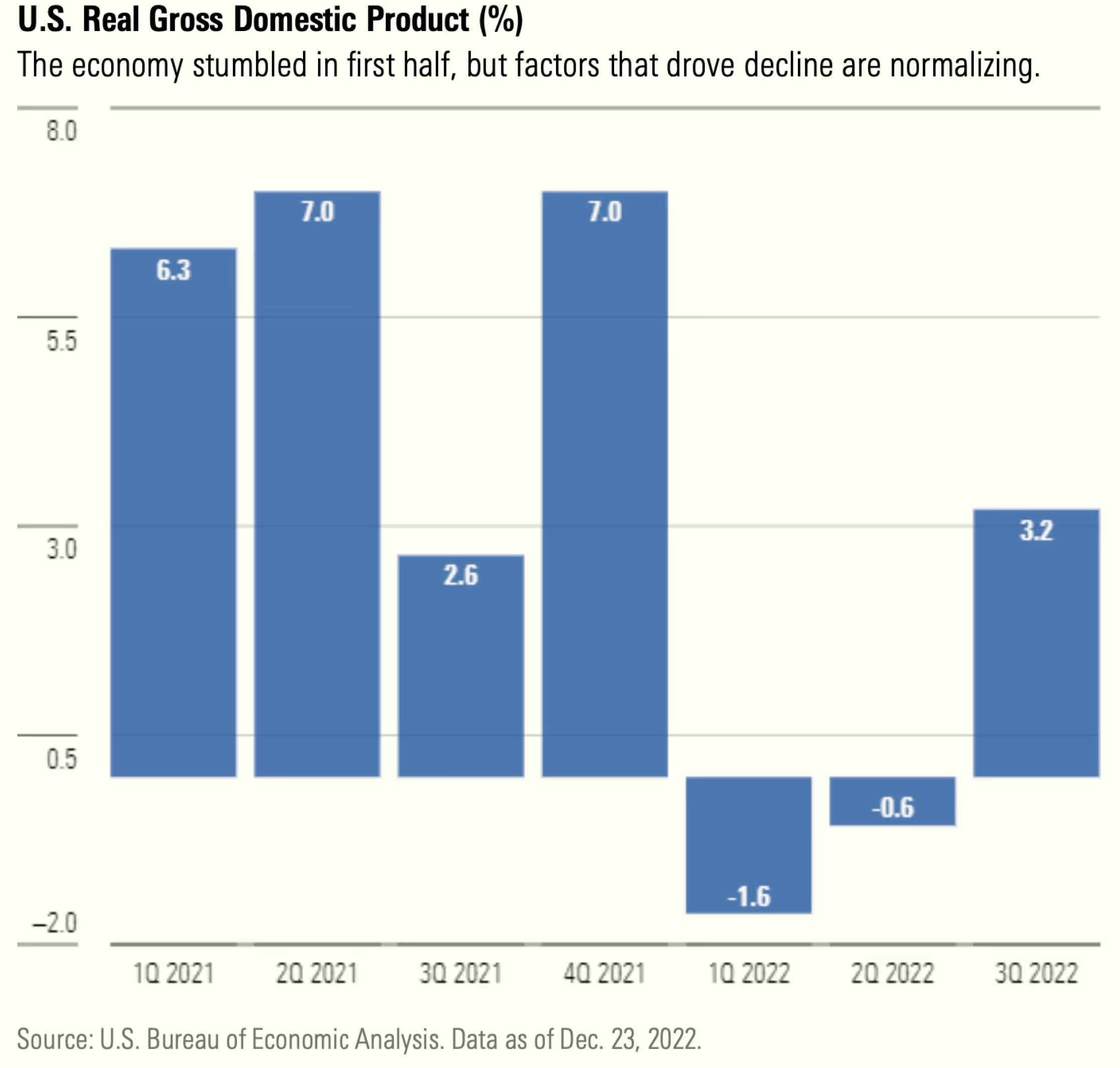

While the risks of slowing growth or an outright contraction are still substantial, we do not feel that a recession is necessarily a foregone conclusion (in contrast to the consensus expectation of professional economists). If a recession does not materialize, we will see near-term upside. And in the event of a mild recession, we believe that there may be limited potential for a substantial, further decline in prices for more risky assets (given the 2022 sell-off).

U.S. corporations and consumers continue to hold high cash balances and moderate debt burdens (conditions that do not historically precede severe downturns), indicating that the avoidance of a recession may not be as improbable as many believe.

The asymmetric risk of these bull and bear outcomes, along with our expectations of a less-antagonistic Fed that adjusts its policy in the face of cooling inflation, grant us the conviction that equities could potentially deliver high single-digit returns in 2023. Thus, for Q1: we increase our allocation to equities (vs bonds) slightly.

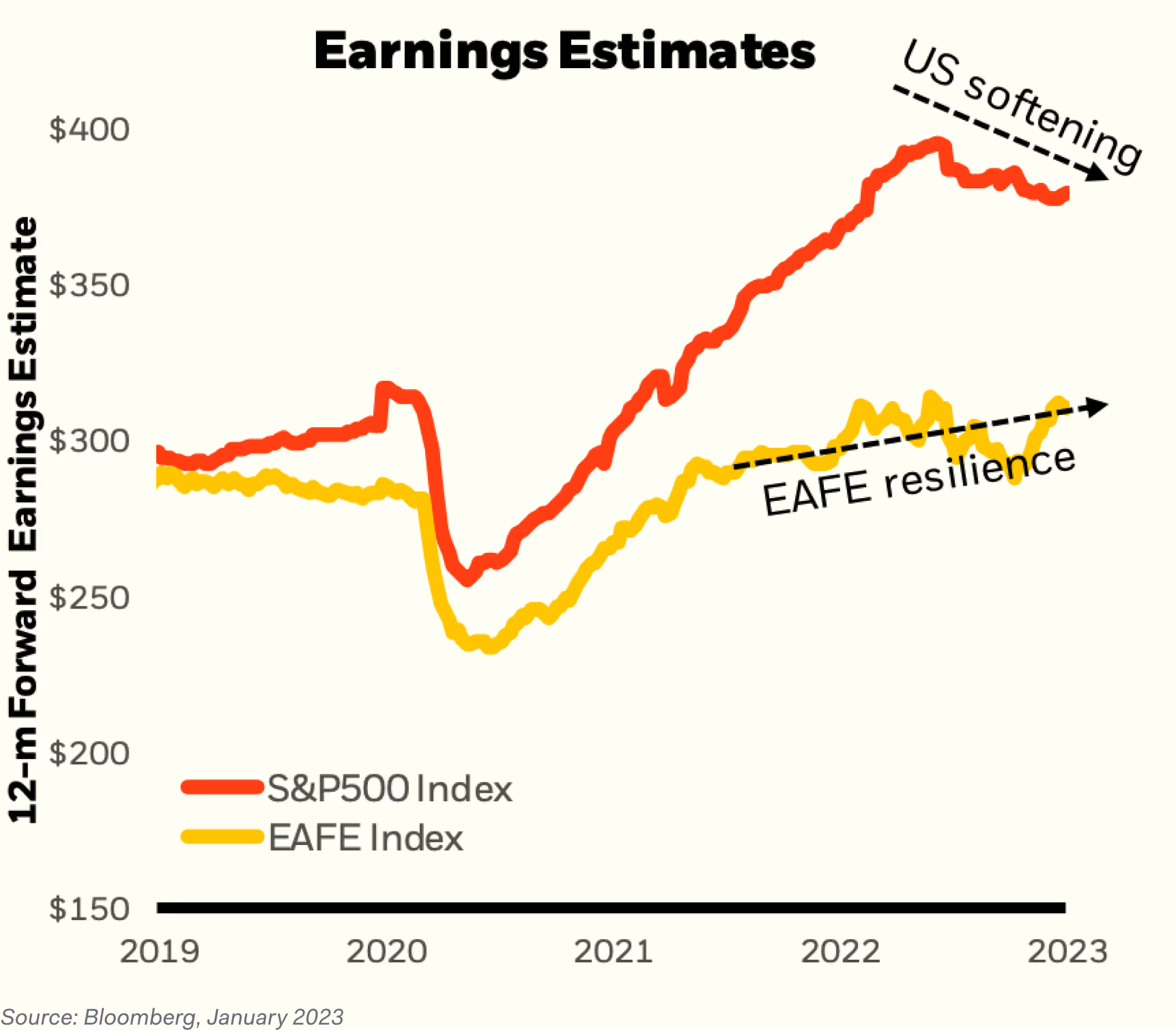

We also see opportunities in international markets, due to the resiliency in international earnings estimates (vs softer U.S. estimates). As a result, we are increasing our weighting in both mature international and emerging markets.

In order to make room for these increased allocations, we are closing out our positions in energy and commodities, having leveraged them for the past 18 months as an inflation hedge.

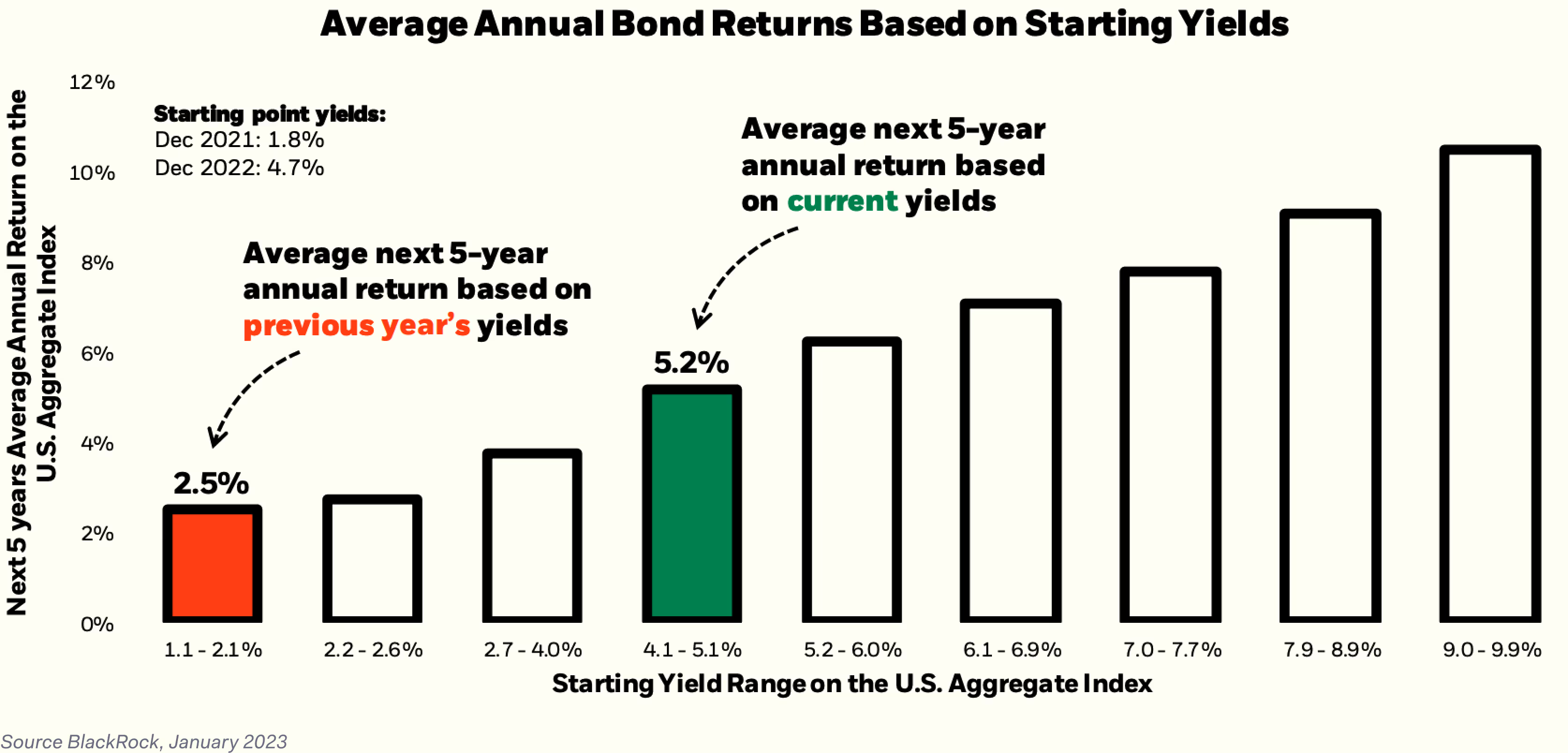

With respect to bonds: after a challenging year in 2022, we believe that fixed-income assets may once again play their traditional role as a portfolio diversifier and volatility dampener. With bond yields now at higher levels, we see total returns in 2023 as being much more favorable.

We are increasing our duration (i.e., time to bond maturity), in order to obtain higher yields; and we are exiting treasury inflation protected (TIPs) positions, as interest rates are expected to decline.

We are also slightly increasing our exposure to credit spreads: allocating more to mortgage-backed securities and emerging market debt, and reducing our weighting of U.S. Treasuries.

Q1 Portfolio Reallocation Recommendations