Private credit has outperformed most public credit over the last decade – and is now approximately the same size as the real estate investment trusts (REIT) market. Given increased regulations on banks, this investment category is expected to grow even faster. And yet, its investors are predominantly institutions, not individuals.

Does private credit deserve your investment dollars?

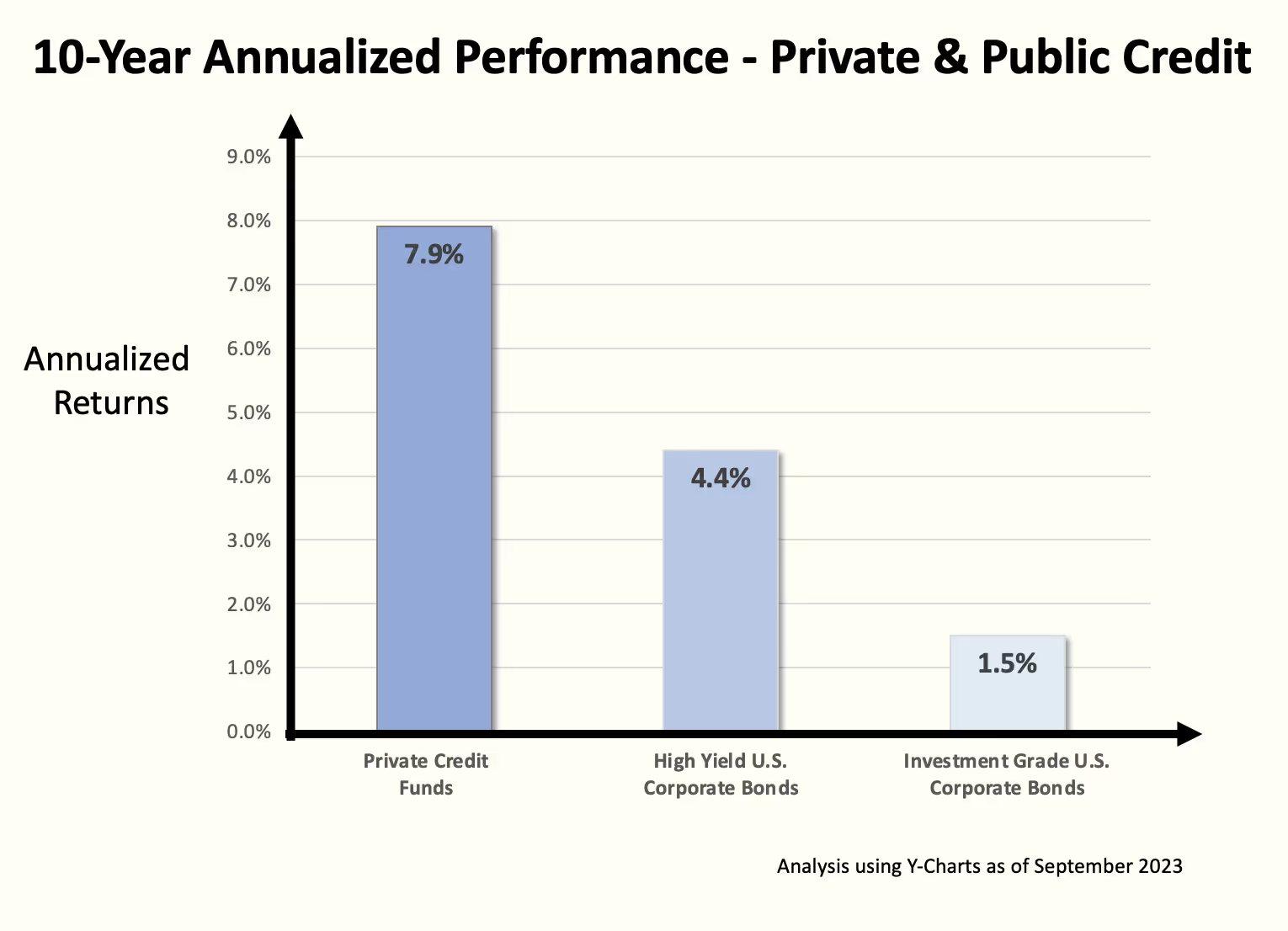

The above chart is an analysis of the prior 10-year returns, showing annualized returns of each aggregate asset class using the following indexes:

- Investment Grade bonds (as measured by the Bloomberg Aggregate U.S. Bond Index)

- High Yield Bond (as measured by the Bloomberg Aggregate U.S. High Yield Bond Index)

- Private Credit (as measured by the Cliffwater Middle Market Direct Lending Index)

What is Private Credit?

To understand this asset class, it is useful to first review the public credit markets: fixed-income investments that are publicly listed on major exchanges such as the NYSE – including large corporation bonds (e.g., the Fortune 500), U.S. government Treasury securities, mortgage-backed securities (MBS), and asset-backed securities (ABS). Each of these asset classes can be invested in directly or through mutual funds and fixed-income ETFs. While government debt is backed at the federal, state, and local level, corporate bonds are typically offered through investment banks or large commercial banks and are backed by the corporations that issue them. Publicly available fixed-income investments are liquid (i.e., traded daily, based on the market price) and exist on a fixed rate basis (e.g., the bond has a stated rate of interest).

Conversely, private credit investments are not typically available through the major exchanges and are not as liquid as their public market counterparts. These investments are made available when private fund managers raise capital from their investors. Unlike public credit, these fixed-income investments are comprised of debt obligations from small-to-medium-sized businesses (companies smaller than the Fortune 500). The fund managers then earn a small percentage of fees based on the assets under their management, and their investors then earn their proportional share of returns when interest payments are made by the businesses that borrow money.

Due to its lack of liquidity and unique set of risks, the investors in private credit funds have traditionally been institutions (such as pension funds, family offices, foundations, asset managers, and university endowments) seeking to diversify from publicly traded fixed-income instruments and to obtain higher than public fixed-income returns. After all, these investors have had the resources and third-party assistance to evaluate these funds and are equipped to mitigate the risk when investing in this asset class. Furthermore, these funds have traditionally had multi-million-dollar, minimum entry-level investment thresholds. Over the last few years, however, fund managers have increasingly structured their funds to be accessible to individual retail investors (see ‘40 Act funds). These newer structures allow for more liquidity options along with lower investment thresholds, with some as low as $10,000.

The Private Credit Boom

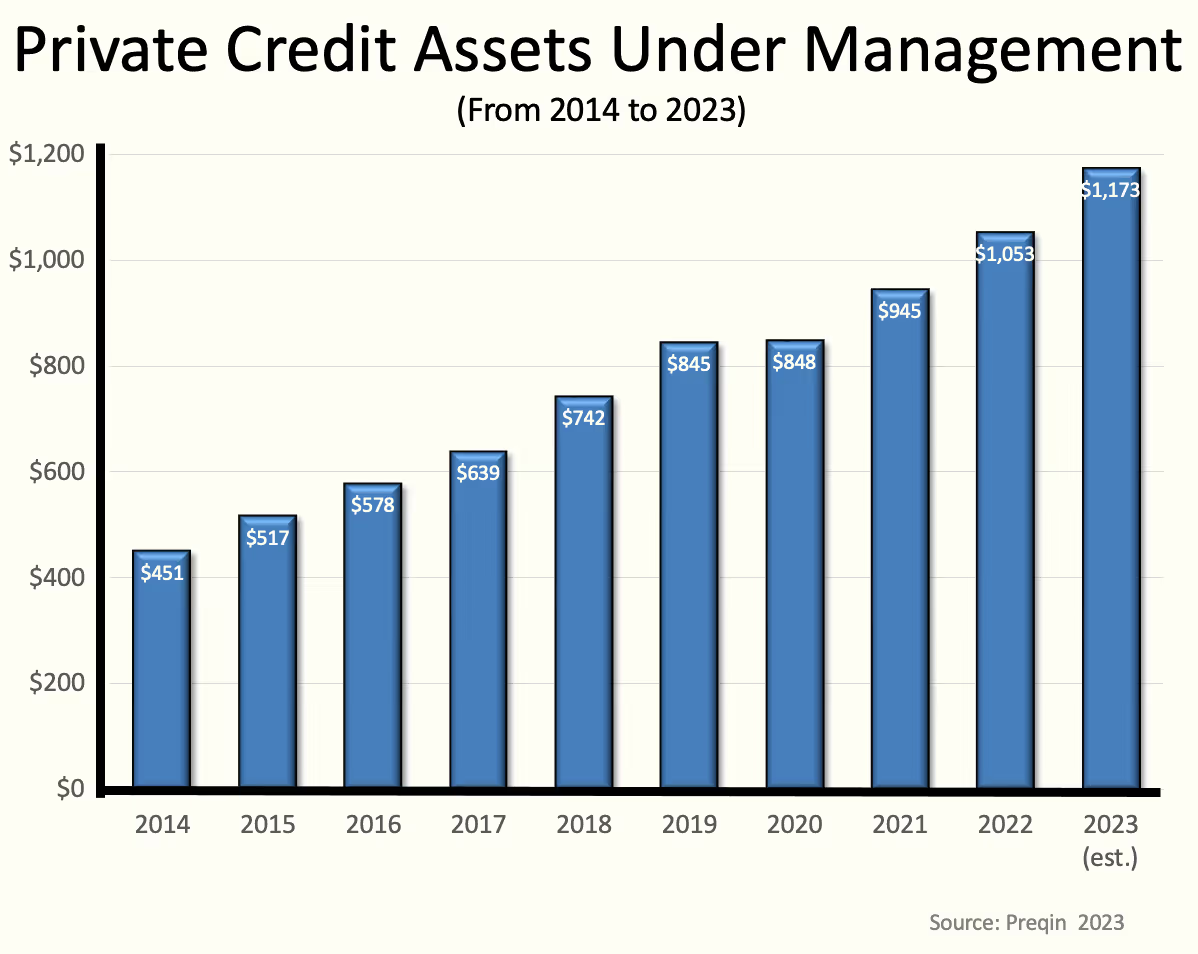

Once a niche investment segment, this category started to expand rapidly as regulatory requirements on banks increased after the 2008 global financial crisis (GFC). These post-GFC regulations made it more difficult for banks to loan money. Smaller regional banks did not want to take on more risk, and larger money-center banks focused more on debt to larger corporations. Over the last decade, private credit fund managers have steadily increased their share of credit to businesses – and now represent more than a trillion dollars under management.

An institutional investor survey conducted by BlackRock in early 2023 showed that the majority of institutional investors plan to place more money in private credit. More recently, BlackRock stated that, given recent banks’ distress and failures in early 2023 (with additional governmental regulations expected), they now favor private credit over public credit.

Private Credit’s Risk & Challenges

At the same time, this asset class has its own unique risks and challenges; and we encourage prospective individual investors to tread with caution.

- Small business sector risk: Since private credit is based on debt instruments for smaller corporations (not the Fortune 500), its default rate could be more sensitive to economic downturns that impact the broader small business economy.

- Lack of liquidity: Depending on the policy and structure of the fund, there are usually restrictions on when one can pull money out or exit the fund (usually on a quarterly basis). Thus, an investor may not be able to sell their position and receive their capital at the precise desired time.

- Non-bank underwriting standards: Because private credit funds are not subject to the same compliance and regulatory standards as banks, one must rely on the underwriting skills of the fund manager.

- Valuation risk: Since private credit is a level 3 (private) asset, the underlying valuations of the indebted companies are often not as accurate as widely traded public companies. Also, their ongoing solvency is not tracked by third-party credit rating agencies. Therefore, the ability of the fund manager to appraise the company and its solvency is especially important in private credit.

- Sub-strategy risk: Most private credit funds are based on general-purpose loans referred to as “direct lending”. However, some fund managers may employ niche debt strategies. For example, some managers exclusively work with riskier venture debt, litigation finance, or distressed lending. As a result, research needs to be conducted on the underlying strategies of each potential fund manager.

- Fees: While management fees are warranted, some managers have a labyrinth of fees, including multi-faceted performance fees. Common direct lending fee structures are greater than a 1% management fee (but some are much higher), along with incentive fees on income over a stated hurdle rate (annualized) and an incentive fee on capital gains. An investor will need to understand all fees, as well as the reported historical performance, and whether the reported returns are stated on a net-of-fees basis.

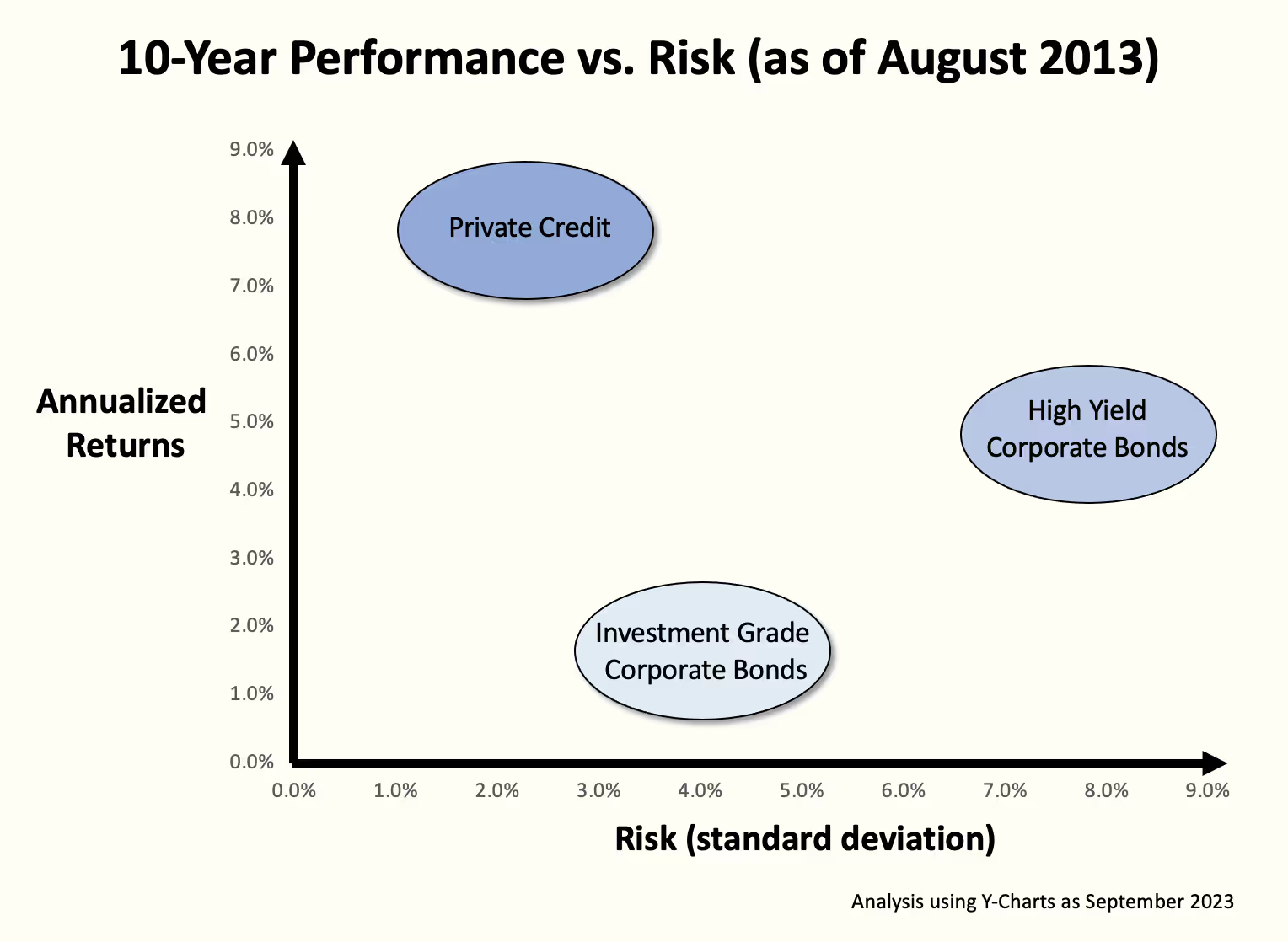

Volatility is Similar to Public Credit

While private credit, as a category, has its own set of unique challenges, its market volatility is similar to publicly traded fixed-income investments.

The above chart illustrates the last 10 years of combined annualized returns, versus the volatility of each asset class (as measured by the standard deviation).

Fund Manager Selection Is Critical

Unlike the publicly traded fixed-income market, in which information on any given bond is widely accessible (including ratings from third-party rating services), private credit investing requires substantial research.

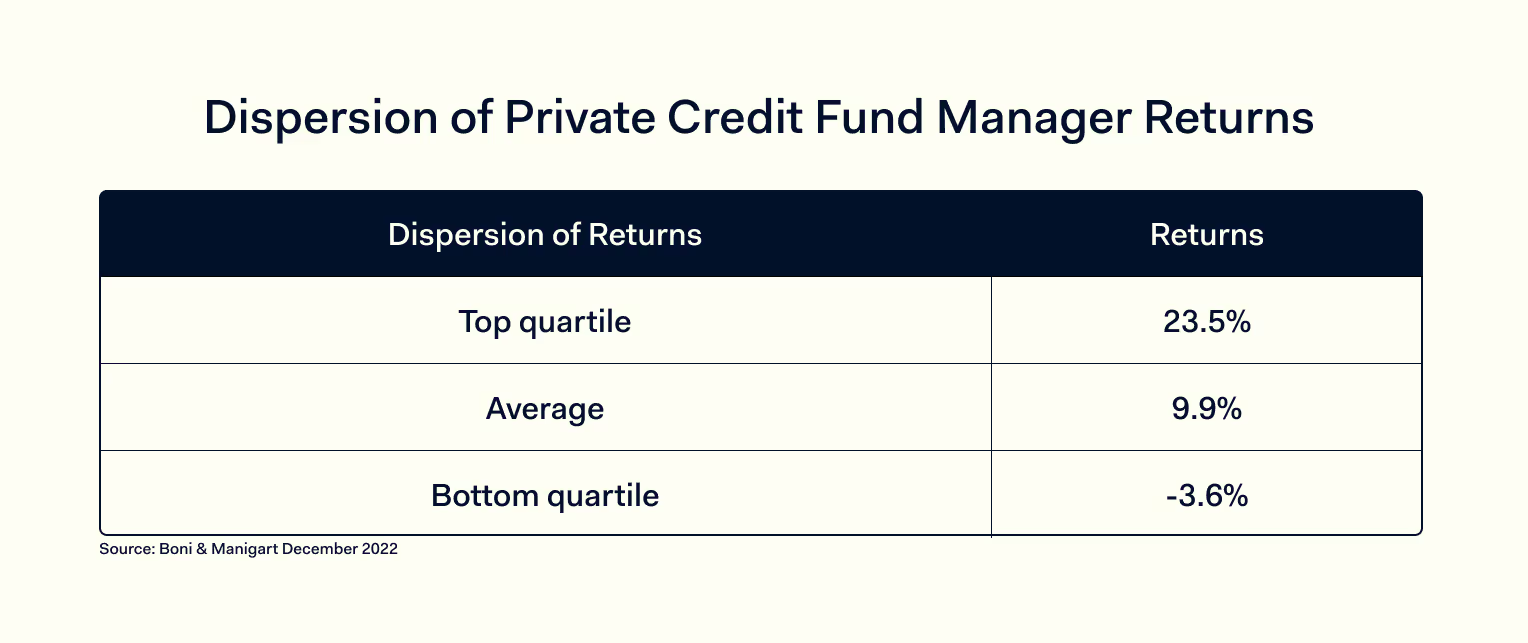

Professors Boni and Manigart recently conducted an in-depth study on over 400 private credit funds. They concluded that while private credit outperformed public credit (even when accounting for fund fees), there was a wide dispersion of returns across all fund managers.

Boni and Manigart concluded that when it comes to private credit, past performance by any given investment manager is a very strong predictor of future success – one only has to research and determine the winners (while steering clear of the losers).

Risk Mitigation

If private credit may make sense for you, there are several ways to manage your risk.

- Diversify managers: with private credit, the underwriter is not a bank with an extensive set of governmental regulations to guide their underwriting process. Instead, investors have to rely on an individual firm’s risk management skill set. Therefore, it is wise to spread your investment across multiple fund managers who have a proven track record of success. This will also reduce liquidity risk since you can have multiple funds with different redemption policies to help ensure you can get access to your money if you need it.

- Diversify strategies: since either deploy several debt strategies in a single private credit fund or only a specific niche strategy (venture debt, distressed credit, etc.) for each fund, you should be aware of any given manager’s strategy and how it will impact the risk and reward of your overall portfolio.

- Allocate appropriately: since private credit isn’t meant to replace all your public credit, you should use it to diversify only a portion of your existing fixed income portfolio.

Consider a Private Credit Sherpa

Investing in this asset class is not as easy as selecting the top publicly listed ETF or mutual fund. It requires careful and extensive research to identify the fund types, their underlying strategy, the specific fund itself, and how it fits into your overall portfolio strategy for your risk profile.

Even seasoned institutional professionals seek assistance in making allocations to this intricate asset class and culling through densely worded prospectuses to zero in on the most appropriate and best-performing funds to invest in.

Farther specializes in private capital, including private credit, and is adept at customizing allocations to meet your individual requirements. Let us guide you through the intricacies of private credit investing.

__________________________________________________________________________________

This material is for informational purposes only and should not be construed as investment advice. Please consult with your advisor for specifics. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy or investment product. Investing in securities involves risks, including the potential loss of money; and past performance does not guarantee future results. Farther suggests that you consult with your tax professional, as we do not provide legal or tax advice.