The first four months of 2025 have tested investors’ resolve, as markets navigated their most turbulent stretch since the pandemic. Equity volatility surged amid conflicting macroeconomic signals, while bond yields fluctuated in response to evolving inflation expectations and trade policy uncertainty. The imposition of broad-based tariffs has introduced a new layer of complexity – pressuring growth while reawakening inflation concerns – and leaving the Federal Reserve straddling the line between benign past data and a forward-looking outlook shaped by the risk of stagflation.

In this month’s commentary, we share how we have adjusted portfolios in response to this dynamic environment, offer our updated capital market assumptions, and provide a forward-looking view across asset classes and the global economy. We remain steadfast in our belief that maintaining discipline – especially in the face of uncertainty – remains one of the most powerful tools available to long-term investors.

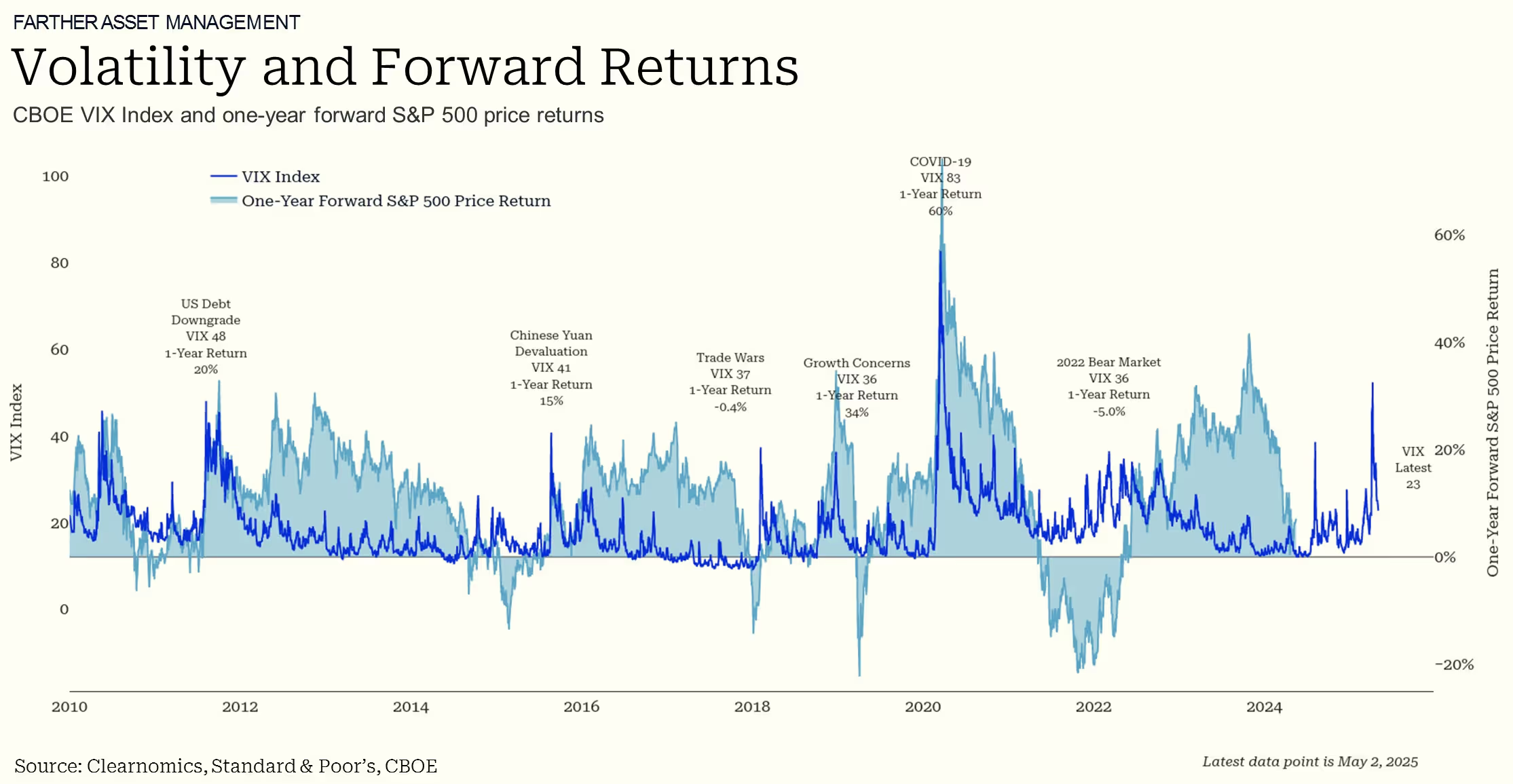

- April marked a particularly volatile chapter, with the VIX briefly exceeding 50 – the highest reading since the pandemic era (as shown in the above chart). Still, sharp selloffs were often followed by swift recoveries, underscoring the inherent difficulty of timing markets. The swings served as a reminder that volatility works in both directions, and that overreacting to short-term movements can derail long-term progress.

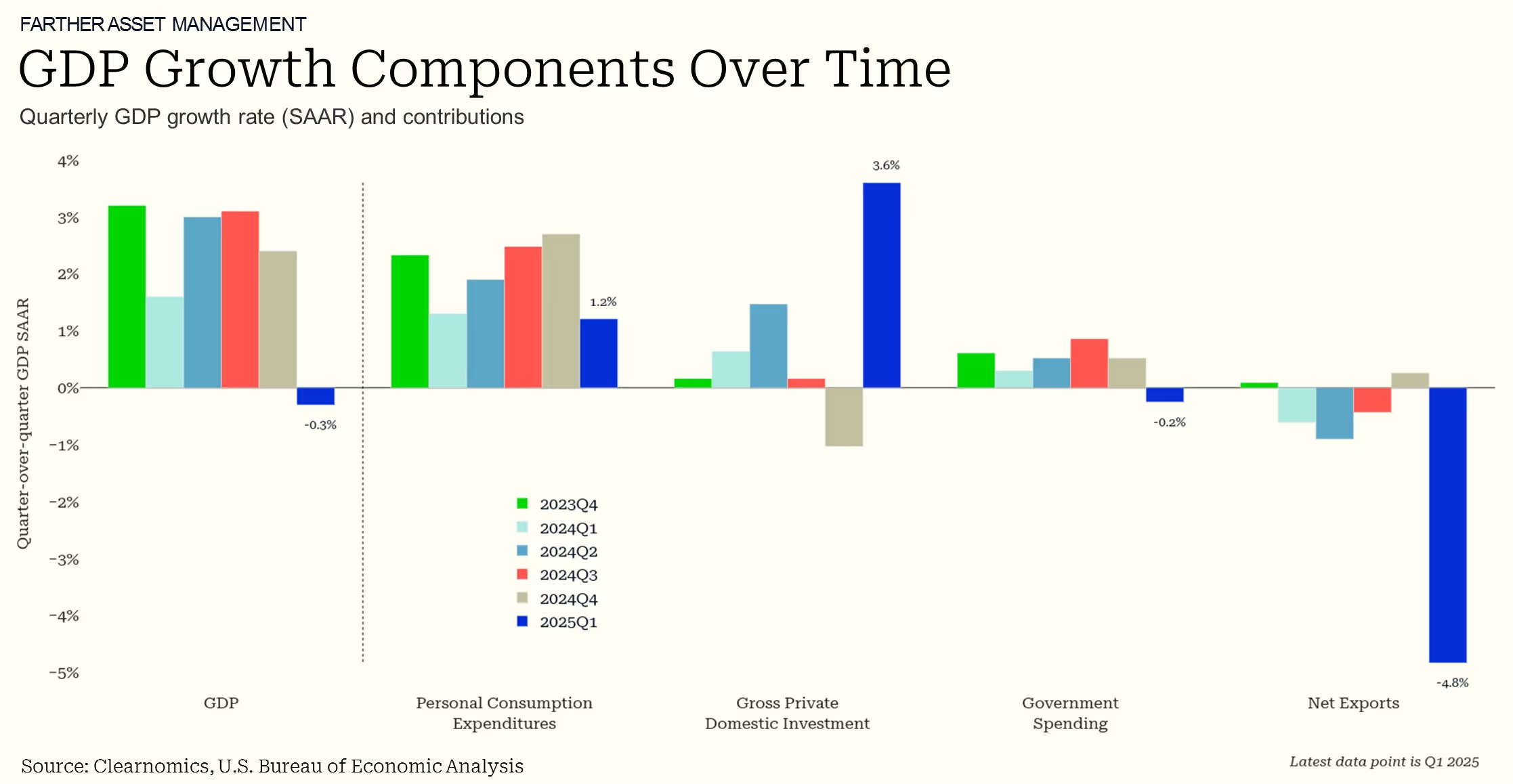

- Investors remain particularly concerned about whether tariffs will simultaneously boost inflation and hamper growth. Recent economic data confirmed a slight contraction in the first quarter economy, with GDP declining by 0.3%, marking the first reduction since early 2022. This downturn stems almost exclusively from trade factors as businesses accelerated imports to build inventory reserves. Consumer spending slowed but maintained positive growth. It's worth noting that these GDP figures represent initial estimates and may undergo revision.

- While markets have recently shown signs of stabilization, uncertainty persists; and several factors driving April's volatility remain in focus. Trade policy developments continue to evolve, though the 90-day pause suggests reduced likelihood of worst-case outcomes. Investors should anticipate continued volatility from tariff-related headlines in the near term, even as markets gradually adapt to the changing trade environment.

Q1 Showed Economic Contraction

Consumer spending has remained the primary engine of U.S. economic growth in recent years, as illustrated in the above chart.

- However, recent surveys suggest that consumers now expect prices to rise more rapidly, both in the near term and over longer horizons. These shifting expectations have weighed on sentiment, driving consumer confidence to some of its lowest levels in over a decade.

- While this change in outlook has yet to meaningfully impact spending behavior or inflation data, it may begin to exert greater influence as the year progresses.

Investors remain particularly concerned about whether tariffs will simultaneously boost inflation and hamper growth.

- Recent economic data confirmed that the U.S. economy contracted by 0.3% in the first quarter, marking the first decline in GDP since early 2022. The contraction appears largely attributable to trade dynamics, as businesses accelerated imports in anticipation of new tariffs.

- While consumer spending decelerated, it remained in positive territory – offering a measure of resilience. These initial figures may be revised in the coming months, but they underscore the economic sensitivity to trade policy shifts.

The complex interplay between economic growth and inflation compounds challenges facing the Federal Reserve. Beyond difficult interest rate decisions in upcoming months, the central bank's independence faced brief questioning from the White House, generating additional market uncertainty. Currently, markets anticipate approximately four rate cuts this year, potentially beginning in July.

April 2025 Market Dynamics and Macroeconomic Context

Equity Markets: Resilience Amid Volatility

Despite a sharp drawdown early in the month, equity markets demonstrated notable resilience in April. The S&P 500 rebounded from an intra-month decline of 12% to finish just 0.8% lower, buoyed by a shift in risk sentiment following delays in tariff enforcement and a string of stronger-than-expected corporate earnings, particularly within cyclical sectors. Nevertheless, year-to-date performance remains in negative territory, with the S&P 500 down 5.3% and the Nasdaq Composite lower by 9.7%.[1][2]

Importantly, April’s rebound was distinguished by broader market participation, diverging from the narrow leadership of megacap technology stocks that dominated 2024. Mid- and small-cap equities outperformed, supported by more attractive valuations – trading at discounts of 15% to 30% relative to their large-cap counterparts – hinting at a potential shift toward a more inclusive market regime.[3][2] International equities also gained ground, aided by a 4.5% year-to-date decline in the U.S. dollar, which enhanced relative performance in developed markets[4][5].

Equity Markets: Valuation Reset

Valuations across equity markets have begun to recalibrate in response to evolving macro conditions. The forward price-to-earnings (P/E) ratio for the S&P 500 has contracted meaningfully, declining to 20.2x from 26.7x at the end of 2024.[8][9] This correction reflects both heightened volatility and more grounded expectations for earnings growth.

Outside the U.S., relative valuations remain compelling. On a sector-neutral basis, international equities now trade at a 35% discount to U.S. peers, with Japanese and European value stocks benefiting from monetary policy normalization and a rebound in capital expenditures.[10][3] Within the U.S., small-cap equities appear increasingly attractive on a relative basis, now trading at a 30% forward P/E discount to large caps – the widest spread observed since 2010.[6][7] For long-term investors, this dislocation offers a potential entry point into overlooked areas of the market.

Fixed Income: A Source of Stability Amid Uncertainty

In a landscape marked by equity market turbulence and policy ambiguity, fixed income provided a steadying force. The Bloomberg U.S. Aggregate Bond Index rose 2.9% year-to-date through April, offering stability to diversified portfolios. The 10-year Treasury yield ended the month at 4.17%, having oscillated between 3.99% and 4.49% as markets recalibrated their expectations for Federal Reserve policy. A notable steepening of the yield curve – reflected in a 14 basis point widening of the 2s10s spread – suggests growing investor skepticism that rate cuts will materialize before the fourth quarter.

Credit markets offered a mixed picture. Investment-grade corporate spreads widened modestly by 35 bps, indicating a cautious tone. Yet high-yield bonds delivered positive performance, supported by firming commodity prices and continued strength in the energy sector – a divergence from typical late-cycle behavior that reflects sector-specific tailwinds.[4][5]

Macroeconomic Crosscurrents: A Mixed but Resilient Picture

While headline growth contracted modestly in the first quarter – GDP declined by 0.3%, marking the first quarterly pullback since 2022 – the underlying economic foundation remains relatively solid. The contraction was largely attributed to a surge in imports as businesses moved to front-load inventory ahead of expected tariffs.[6]

Several key indicators point to resilience beneath the surface:

- Inflation Moderation: Headline CPI for March cooled to 2.4% year-over-year, though core services inflation remains elevated at 3.1%.[7]

- Labor Market Strength: The unemployment rate held steady at 3.8%, and while wage growth has cooled to 4.1%.[6]

- Consumer Sentiment: Retail sales declined by 0.9% in March, yet the low personal savings rate remains depressed at 4.6%, suggesting pent-up demand.[4]

These dynamics create a complex backdrop for portfolio construction, where traditional 60/40 allocations require recalibration for higher macroeconomic volatility.[8][9]

Dynamic Asset Allocation Revisions

Fixed Income Positioning: Enhancing Stability and Flexibility

Our fixed income strategy remains anchored in high-quality, shorter-duration instruments – reducing overall portfolio duration by 0.15 to 0.19 years. This aligns with capital market assumptions favoring short-term Treasuries over long-dated bonds amid persistent term premium pressures.[9]

Key refinements include:

- Floating-Rate Instruments: We increased exposure to floating-rate securities as a hedge against continued rate volatility.

- Municipal Bonds: In taxable portfolios, we shifted from intermediate to short-duration municipals to enhance interest rate sensitivity and preserve tax efficiency.

- Inflation Protection: We expanded our allocation to Treasury Inflation-Protected Securities (TIPS), focusing on maturities within the 0–5 year range. This positioning aims to safeguard purchasing power in an environment shaped by structural inflationary forces – most notably from AI-driven capital expenditures and supply chain realignments.[10][9]

Equity Rebalancing: Valuation Discipline and Global Opportunity

On the equity side, we have taken deliberate steps to improve valuation exposure and increase portfolio efficiency:

- Mid-Cap Emphasis: We increased exposure to mid-cap equities, which are trading at a 22% discount to their 10-year average valuations – a level that presents compelling upside potential.[3]

- Global Diversification: Developed international markets saw a modest allocation increase, supported by favorable relative valuations and improved return expectations. For context, J.P. Morgan forecasts 8.84% annualized returns for EAFE equities, compared to 7.64% for global equities broadly.[5]

- Quality Tilt: We strengthened the portfolio’s quality profile by prioritizing companies with return on invested capital (ROIC) above 15% and debt-to-EBITDA ratios below 2x. As a result, the portfolio’s dividend yield improved from 1.93% to 2.19%, reinforcing both income and stability characteristics.

May 2025 Capital Market Assumptions

Fixed Income Expectations

Equity Return Projections

- U.S. Large Caps: 6.3% annualized (down from 6.9% in 2024) due to rich valuations.[11]

- International Developed: 8.8% expected returns, driven by weaker USD and AI productivity gains.[5]

- Emerging Markets: 9.1% potential returns, though China exposure remains limited to 2% of allocations.[10]

- US Small Caps: Small-cap equities trade at a 30% P/E discount to large caps – their widest gap since 2010 – creating potential for mean reversion as rates stabilize.[3]

Alternatives and Real Assets

Overweight Infrastructure, Underweight REITs

Infrastructure equities now comprise a larger portion of portfolios, offering 6.2% dividend yields and inflation-linked cash flows.[6][7] Gold remains a core component of the strategic allocation as a geopolitical hedge, with significantly higher expected annual returns in stagflation scenarios.[10][9]

Asset Class Outlook and Implementation

Equity Allocation Recommendations

- Cyclical Value Rotation: Increase exposure to sectors benefiting from capex growth, particularly industrials and materials.

- Small-Cap exposure increases: Exploit valuations 22% below historical averages.

- Selective Internationalization: Overweight Japanese and European equities, leveraging BOJ policy normalization and AI-driven productivity gains.[11][5]

Fixed Income Positioning

- Credit Quality Over Yield: Reduce high-yield exposure, reallocating to floating-rate corporates and short-duration municipals.

- Laddered Maturities: Concentrate 75% of bond holdings in 2–5 year maturities to balance yield and rate risk.

- Inflation Hedge Anchor: Increase allocation to inflation-linked securities, primarily in short- to intermediate maturities

- Currency Management: Reduce FX-hedged international exposure to capitalize on USD weakness.[8][9]

Macro Risks and Opportunities

Three forces will dominate the rest of 2025:

- Tariff Implementation: The 90-day tariff pause creates a window for portfolio rebalancing before potential October volatility[18].

- Fed Policy Path: Market-implied 65% probability of July rate cut creates opportunities via convexity in rate-sensitive assets[5].

- Earnings Revisions: S&P 500 EPS estimates were revised down 4.2% for Q2. A stabilization in tech guidance is critical to future earnings estimates[19]

Conclusion: Navigating the New Macro Regime

The April 2025 market “stress test” validated Farther’s dynamic asset allocation framework. By reducing duration risk, enhancing inflation protection, and rebalancing equity exposures toward undervalued market segments, portfolios are positioned to navigate the uncertainty that sits in front of us.

Six critical imperatives emerge for H2 2025:

- Maintain Quality Bias: Prioritize companies with strong balance sheets and pricing power.

- Ladder Bond Maturities: Mitigate reinvestment risk in a higher-for-longer rate environment.

- Monitor Tariff Impacts: Prepare tactical rotations to domestic industrials if trade tensions escalate.

- Duration Discipline: Short-term bonds now provide 85% of long-dated yield with 40% less volatility.[14][15]

- Global Value Rotation: International cyclicals trade at 12x earnings vs. 18x for U.S. defensives.[16][13]

- Inflation Resilience: Real assets are priced for 2% inflation but hedge against 4%+ scenarios.[10][17]

While AI-driven growth narratives dominate headlines, we emphasize cash flow durability in equity selections and quality convexity in fixed income. As J.P. Morgan notes, "The 2025 market regime favors investors who position for reflation without overpaying for growth."[13] By maintaining barbelled exposures to both defensive yield and cyclical value, portfolios are positioned to navigate the transition from monetary to fiscal dominance.

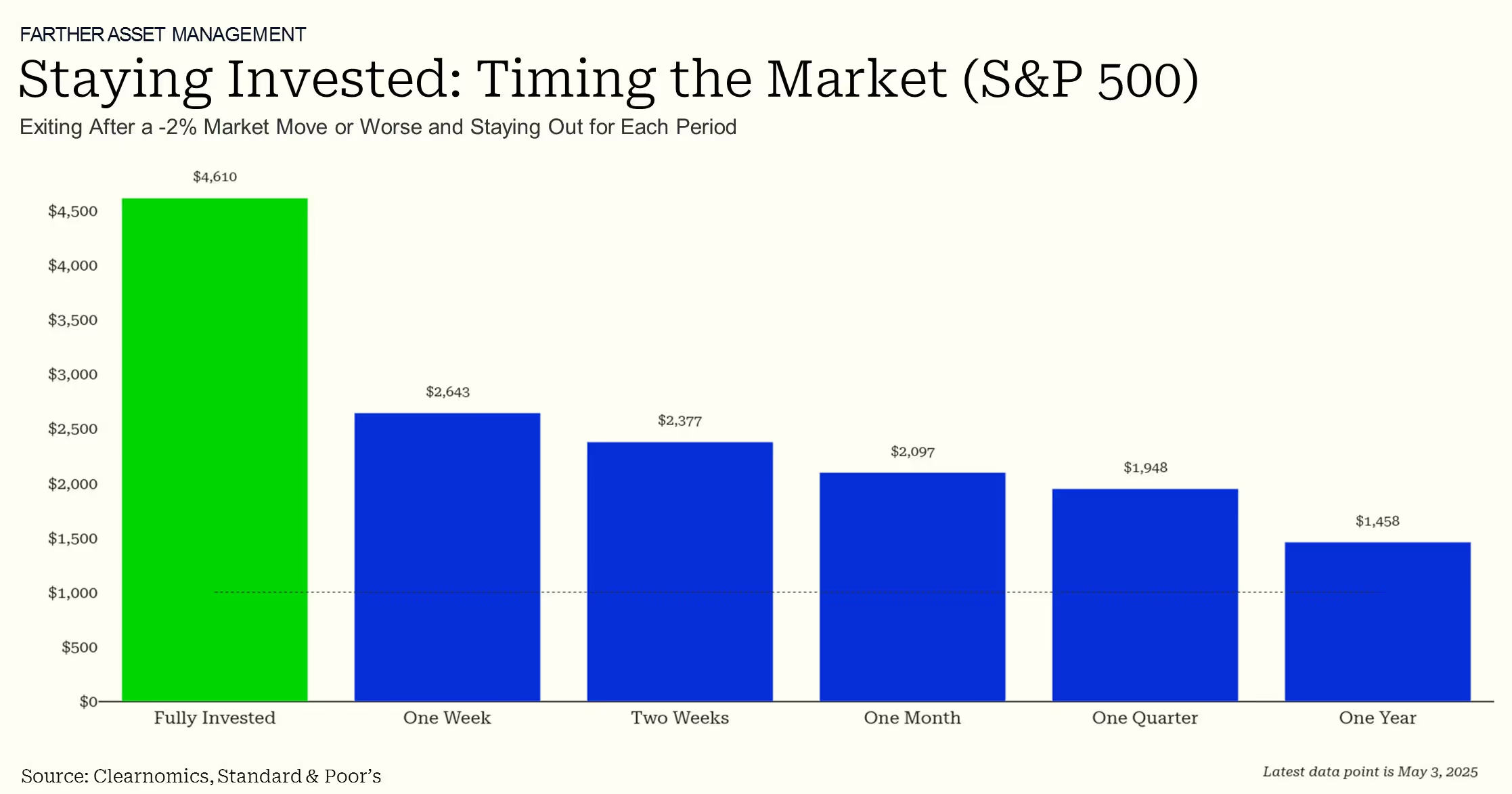

Staying the Course Through Volatility: Historical Rewards of Patient Investing

Despite recent market headwinds, one enduring investment principle remains clear: patience and discipline through volatile periods have historically rewarded long-term investors. As illustrated in the above chart, attempting to sidestep short-term declines – such as reacting to drops of 2% or more – can lead to costly missteps. Positive and negative market days often arrive without warning, and stepping out of the market, even briefly, risks missing the sharp rebounds that frequently follow downturns.

In the face of heightened uncertainty, it can be tempting to shift course. Yet these very periods serve as a valuable reminder of the importance of thoughtful financial planning, intentional portfolio construction, and a long-term mindset. Market dislocations often give rise to compelling valuations and opportunities across asset classes, offering entry points for investors seeking to enhance diversification and positioning.

The takeaway? April’s market volatility serves as a powerful reminder that significant market movements can occur unexpectedly. Historical evidence consistently shows that disciplined investors who maintain focus on long-term financial objectives position themselves more effectively to achieve their goals.

---

- https://www.wsj.com/finance/stocks/global-stocks-markets-dow-news-04-30-2025-bf889725

- https://www.fidelity.com/learning-center/trading-investing/stock-market-outlook

- https://akwealthadvisors.com/market-update-april-2025/

- https://www.parkavenuesecurities.com/monthly-market-commentary-april-2025

- https://am.jpmorgan.com/pt/pt/asset-management/adv/insights/market-insights/monthly-market-review/

- https://www.cbsnews.com/news/gdp-report-today-trump-tariffs-economy-first-quarter-2025/

- https://tradingeconomics.com/united-states/inflation-cpi

- https://www.poems.com.sg/glossary/financial-terms/dynamic-asset-allocation/

- https://www.blackrock.com/ca/institutional/en/insights/charts/capital-market-assumptions

- https://research-center.amundi.com/article/capital-market-assumptions-2025

- https://www.capitalgroup.com/about-us/news-room/capital-group-issues-2025-capital-market-assumptions.html

- https://pro.thestreet.com/market-commentary/will-april-deliver-a-record-intra-month-swing-even-as-danger-lurks

- https://am.jpmorgan.com/us/en/asset-management/institutional/insights/portfolio-insights/ltcma/

- https://www.fr.vanguard/professionnel/analyses/what-do-higher-starting-yields-mean-for-the-bond-outlook

- https://corporate.vanguard.com/content/corporatesite/us/en/corp/who-we-are/pressroom/press-release-vanguard-releases-2025-economic-and-market-outlook-121124.html

- https://www.invesco.com/content/dam/invesco/apac/en/pdf/insights/2024/december/2025-invesco-capital-market-assumptions-USD.pdf

- https://research-center.amundi.com/article/capital-market-assumptions-2025

- https://www.optimacapitalmgt.com/insights/market-volatility-90-day-reciprocal-tariff-pause-investor-dip-buying

- https://advantage.factset.com/hubfs/Website/Resources Section/Research Desk/Earnings Insight/EarningsInsight_041125.pdf