As I previewed in our Aug. 18th piece, the Federal Reserve had two major opportunities to discuss and vote on monetary policy in late August and late September.

On Aug. 25th, Federal Reserve Chairman Jerome Powell delivered his annual speech at the Kansas City Fed’s symposium in Jackson Hole. While not as dramatic as last year's short, eight-minute speech, he still managed to deliver some noteworthy comments.

One of Powell’s most important statements – "Two percent is and will remain our inflation target" – was a firm pushback against dovish pressure to declare victory on inflation and move to a 3% inflation target (i.e., where year-over-year inflation ran in June and July), as exemplified by a WSJ op-ed authored by Jason Furman, the Obama administration’s Chairman of the Council of Economic Advisors from 2013-2017.

Chairman Powell concluded his speech with the interesting phrase, "We are navigating by the stars under cloudy skies" – which is obviously a challenge. He reiterated that the Federal Reserve would proceed carefully, based on economic data, before deciding whether to further tighten monetary policy or hold rates steady.

The Federal Reserve left interest rates unchanged following its Sept. 20th meeting, as had been expected. The Federal Reserve’s Summary of Economic Projections (SEP) indicated that 12 of 19 Fed officials expected one more Federal Funds rate increase this year. Regardless of whether that increase takes place, Chairman Powell noted in his press conference: "We remain committed to bringing inflation back down to our 2 percent goal and to keeping longer-term inflation expectations well anchored. Reducing inflation is likely to require a period of below-trend growth and some softening of labor market conditions."

In other words, the Fed will keep short-term rates "higher for longer" to fight inflation. The decline in the inflation rate from 9% to 3% over the past year was the relatively easier part for the economy and labor market (although not for the financial markets and certain banks). The amount of economic damage that might be caused by keeping rates "higher for longer" to reduce the inflation rate is unknown. Importantly, longer doesn't necessarily mean years: the Fed’s SEP expects lower Federal Funds rates by the end of 2024 and again in 2025.

Financial Market Response

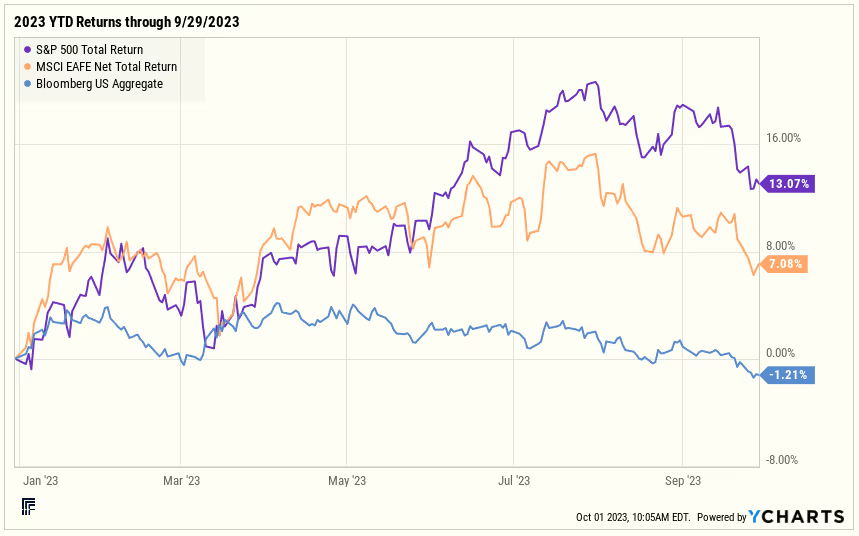

Stock markets hit their peaks for the year at the end of July. Since then, both the stock and bond markets have sold off. From Jul. 31st through Sept. 29th, the S&P 500 Index was down -6.3%, the MSCI EAFE Index was down -7.1%, and the Bloomberg US Aggregate Index was down -3.2%. The S&P 500 remains up +13.1% for the year, and the MSCI EAFE is up +7.1%. The Bloomberg US Aggregate is down -1.2%. Even though interest rates have risen this year, the higher starting points for interest rates in January have mostly offset the principal losses on bonds in 2023 thus far.

Portfolio Construction Thoughts

Sharing a few observations on the current markets:

- U.S. stocks have gotten slightly cheaper in the past two months. The S&P 500 trades at 17.9x expected earnings, down from 19x, but still at a premium to its long-term average of 16.7x.

- International stocks trade at 12.4x expected earnings – one of the largest relative discounts to U.S. stocks in the last 20 years, according to JP Morgan research. International indices include more value stocks, whereas the S&P 500 contains more growth stocks.

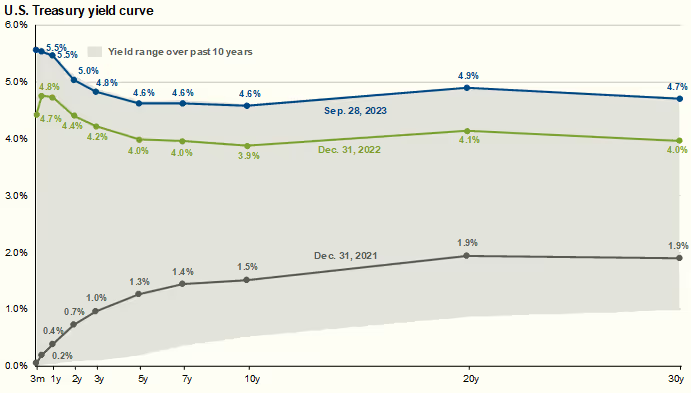

- Interest rates in the U.S. have continued to rise since August. Across the yield curve, U.S. Treasury securities are trading at their highest yields of the last decade, as can be seen in the below chart. As previously discussed, when interest rates fall, they are likely to fall quickly. The comfort of the 5.5% T-bill is likely to be ephemeral at some point next year. For investors who are overweight cash in their portfolios, extending the maturity of your portfolio and locking in yields in short-term U.S. T-Notes remains an attractive proposition.

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management Guide to the Markets – U.S. Data are as of September 28, 2023.

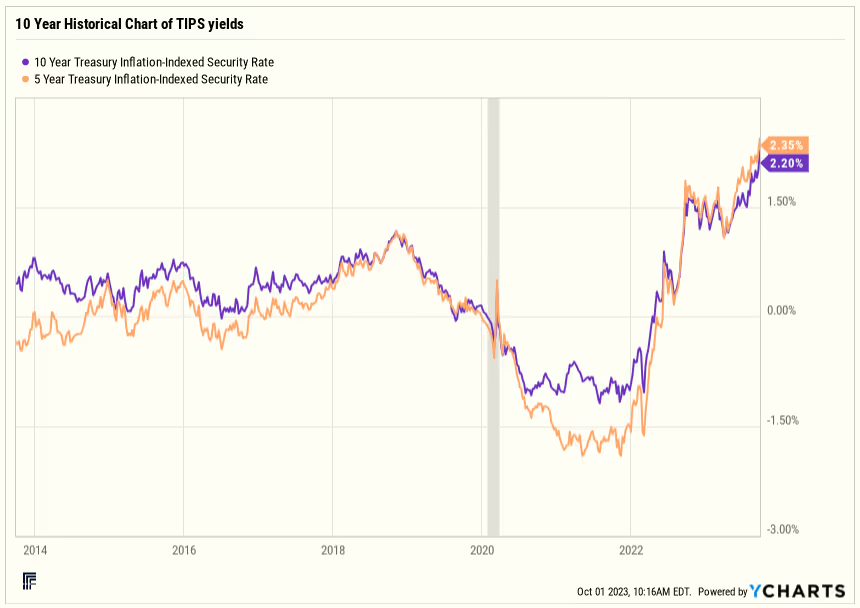

- For investors looking to avoid inflation risk in their bond portfolios, real yields on U.S. TIPS have recently risen above 2% for both 5- and 10-year TIPS: the highest levels in the past decade. These rates are in marked contrast to 2020-22, when real yields were negative on TIPS (as shown in the below chart).

Please connect with your advisor, if you would like to discuss any of the topics raised in this piece or receive help with a portfolio that is significantly weighted to cash and short-term investments.

Lauren Moone, CFA, contributed to this piece.