The first half of 2023 saw both positive developments – such as the strong returns in financial markets – and negative events, including the failures of three large banks in the U.S. and the near failure of Credit Suisse in Switzerland.

This piece attempts to summarize the key economic and financial market events that took place over the past 6 months. While there are no crystal balls in investing, I will try to highlight some areas of opportunity and potential risks to the markets. Most importantly, the more that one can focus on investing for the long-term, the higher the likelihood of reaping the rewards from the past 40 years (which are likely to continue in the coming decades).

Economic Review

Our January piece highlighted several themes that would drive the U.S. economy this year: inflation, the Federal Reserve’s response to combat inflation, and concerns over a possible U.S. recession or soft-landing. The U.S. economy has proved resilient and continued to grow modestly during the first half of 2023. First quarter real GDP grew at 2.0%, and second quarter real GDP is expected to grow at a similar rate. Corporate earnings have also remained strong and are expected to grow this year, which has supported the recovery in stock prices through June.

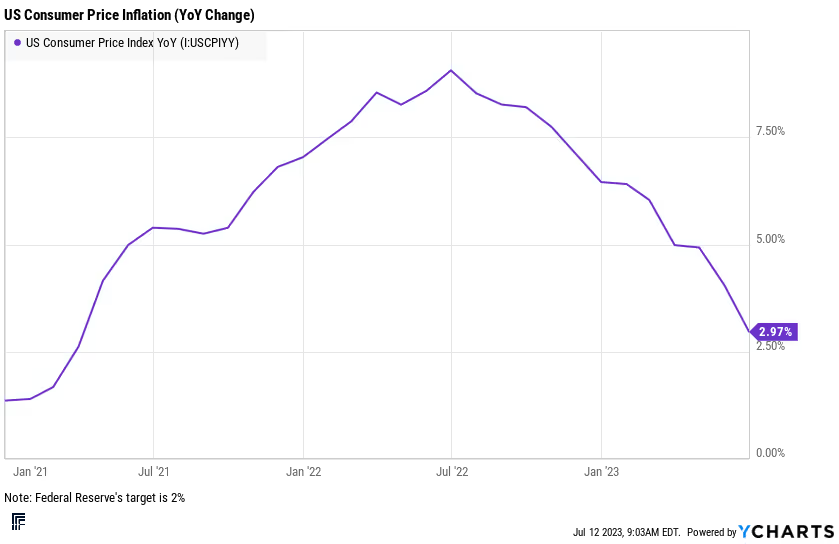

As shown in the above chart, the U.S. Consumer Price Inflation (CPI) rate has fallen since its mid-2022 peak – with the Federal Reserve targeting a 2% annualized CPI rate.

It is important to note a few elements about this data set. Most importantly, the CPI data reports the year-over-year change in prices: a positive number still indicates that prices are higher today than a year ago. While energy prices have fallen meaningfully in the past year, other areas like shelter, hotels, and transportation have increased. Since the beginning of 2021, the cumulative inflation was approximately 16.5% through June 2023. By comparison, the cumulative inflation over the prior decade was approximately 18%, according to the Bureau of Labor Statistics (BLS). The consequences of this accelerated, compressed inflationary episode are still playing out, with the Federal Reserve’s aggressive interest rate response to fight inflation by slowing the economy.

The Federal Reserve raised the Federal Funds rates 0.75% in the first half of the year to a target of 5.25%, as it continues to focus on its battle to lower inflation. We saw 0.25% increases in February, March, and May – while skipping an increase in June. Federal Reserve officials in public statements since the June meeting have indicated that the Fed is likely to raise interest rates 0.50% more this year, with an expected increase of 0.25% at the July 26th meeting. Federal Reserve officials have stated that the Fed’s price stability mandate is more important than its employment mandate until inflation returns to its target, even if high interest rates lead to a recession.

In March, the U.S. suffered two major bank failures: Silicon Valley Bank and Signature Bank fell in swift succession, resulting from the combination of securities losses, due to higher interest rates and high levels of uninsured deposits, which led to rapid deposit runs on both banks as their problems became apparent. In May, First Republic Bank failed for similar reasons: long-term loans whose values had fallen, coupled with funding costs that had increased dramatically, as low-cost uninsured depositors pulled money from the bank. I have written previously that these failures were 8.0 financial earthquakes, and it remains to be seen how many aftershocks (i.e. further bank failures) we may see during the second half of the year.

Market Review

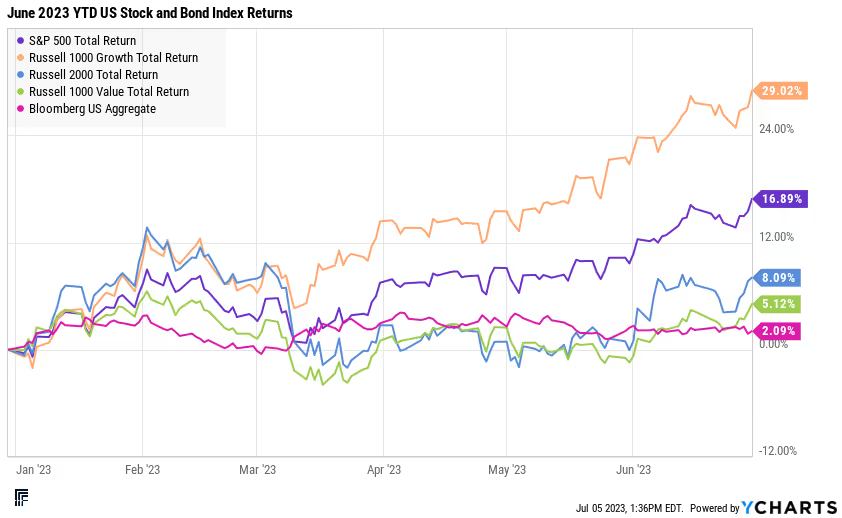

U.S. stocks have had a very strong first half of 2023, rebounding from a challenging 2022. As I wrote in January, we entered this year at significantly more attractive starting valuations for stocks and bonds than we saw at the beginning of 2022. Despite concerns about a possible recession, continued interest rate increases from the Federal Reserve, and a banking crisis that began in March with the collapse of Silicon Valley Bank, the U.S. markets have proved resilient.

- Large-cap stocks outperformed small-cap stocks, and growth stocks outperformed value stocks in the first half of 2023.

- Bonds had a small positive return, in-line with collecting a higher coupon for half a year.

- The S&P 500 Index returned +16.9%, while the small-cap Russell 2000 Index returned +8.1%.

- The Russell 1000 Growth Index returned +29.0%, while the Russell 1000 Value Index returned +5.1%.

- The Bloomberg US Aggregate Bond Index returned +2.1% for the first half of the year.

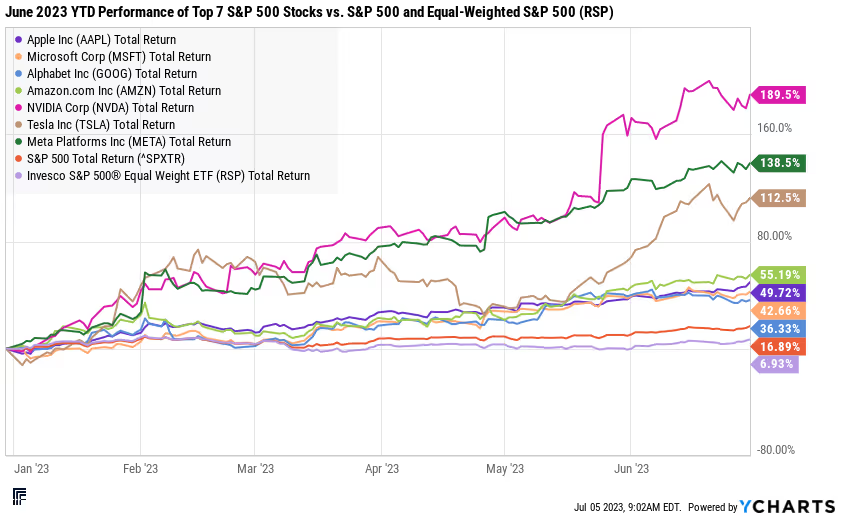

The first chart of broad index returns does not fully communicate how narrow the returns have been in the U.S. stock market. The top seven stocks have contributed virtually all of the performance of the S&P 500 through June. Triple-digit returns from NVIDIA, Meta Platforms, and Tesla, and returns of 36% to 55% from Alphabet, Microsoft, Apple, and Amazon have fueled the S&P 500’s return. Technology stocks, particularly ones with exposure to generative AI, have captured much of the market’s attention. In contrast, the Equal-Weighted S&P 500 Index had a return of only 6.9% for the first half of the year, versus the S&P 500 Index return of 16.9%. The above chart illustrates how dramatic the returns have been for these seven stocks this year.

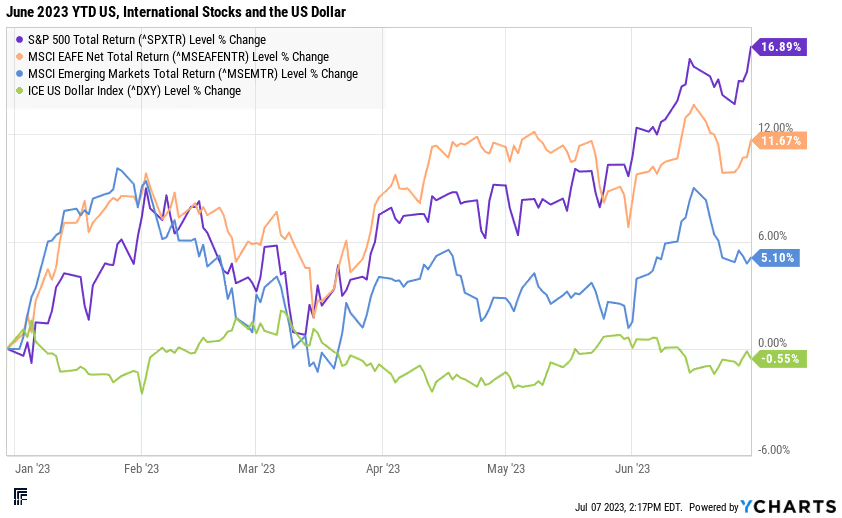

The U.S. stock market also outperformed both developed and emerging market international stocks. The MSCI EAFE Index returned +11.7%, and the MSCI Emerging Market Index returned +5.1% through June. The U.S. Dollar Index was down a modest -0.55%, following 2022’s roller coaster year, which provided a strong headwind to international returns for the first nine months, and a tailwind during the final three months of 2022.

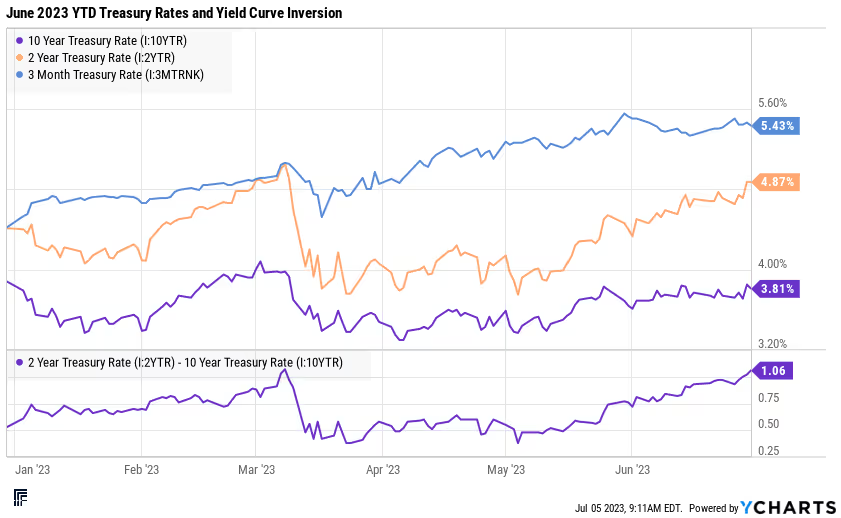

The above chart shows the path of interest rates on Treasury securities for the first half of the year. If you only looked at the beginning and end points of the charts, their changes would be consistent with the Federal Reserve raising short term rates, as reflected in the rise in 3-month T-Bill yields; the market believing that the Fed would succeed in its goal of lowering inflation in the next year or two, as reflected by the 10-year T-Note yield being roughly flat; and the 2-year T-Note yield being slightly higher for the year, but noticeably lower than the 3-month T-Bill yield.

It is important to note the shifts in rates during the middle of March – when the 2-year T-note’s yield fell over 1% in a matter of days, following the failures of Silicon Valley Bank and Signature Bank. The 2-year T-note was used as a safe haven during that crisis and could behave similarly in a future crisis.

H2 Outlook

We do not claim to have a crystal ball on the markets, particularly in the near term. It is impossible to know whether the narrowly focused U.S. market will remain focused on generative AI, or whether market participation will broaden beyond the largest 7 stocks. Our firm recommends diversified core investments, particularly in the U.S. equity market. By owning the S&P 500, investors will have exposure to whichever theme drives the S&P 500’s returns.

There are, however, areas of the markets that are attractively priced now:

- International equities traded at a Price-to-Earnings (P/E) ratio of 13.1, compared to 19.1 for the S&P 500 at the end of June.

- U.S. equities beyond the largest 10 stocks in the S&P 500 are relatively inexpensive. The average P/E ratio of the largest 10 stocks was 29.3 on June 30th. The remaining 490 stocks had an average P/E of 17.8.

- Investment grade bonds remain attractive after the recent rise in yields. Yields on investment grade bonds remain near the 10-year highs reached during the fall of 2022. The income is back in fixed income. For clients who are overweight cash and underweight duration in their bond portfolio, locking in yields and extending duration in the intermediate part of the yield curve looks attractive at present.

It is difficult to predict when this value may be recognized; however, over 5-year periods, the starting valuation on an asset is a very good determinant of its return, according to JPMorgan Asset Management research. Purchasing stocks when they have lower P/E ratios (i.e. when they are cheaper) leads to higher returns over time. Similarly, purchasing bonds when yields are higher leads to better investment returns over time. However, the correlation between starting valuation and 1-year returns is much less strong. Expensive assets can perform well, and cheap assets can perform poorly over short time periods.

There continue to be risks to the economy and financial markets during the second half of the year. The most likely risk would be the potential for additional regional bank failures. The shape of the yield curve, which has lowered the value of banks’ assets (loans and securities) and raised the cost of deposits, as well as a looming commercial real estate crisis, are likely to continue to hurt the balance sheets and income statements of banks. Do not be surprised to hear more about this topic in the news this year. Because of the risk to bank depositors, it is important to safeguard your cash and acquire yield versus banks’ deposits, through the use of Treasury MMFs, ETFs, or T-Bills.

Longer Term Perspective

I wanted to conclude this piece by offering some longer-term perspective on investing. The financial press, media, and Wall Street research analysts tend to focus on and amplify the most recent events and make predictions regarding what will happen in the near future. Wall Street analysts place 1-year targets on individual stocks or the S&P 500 as if they possess crystal balls. The analysts who get that short-term prediction correct tend to receive the most airtime on TV, particularly when they are bearish.

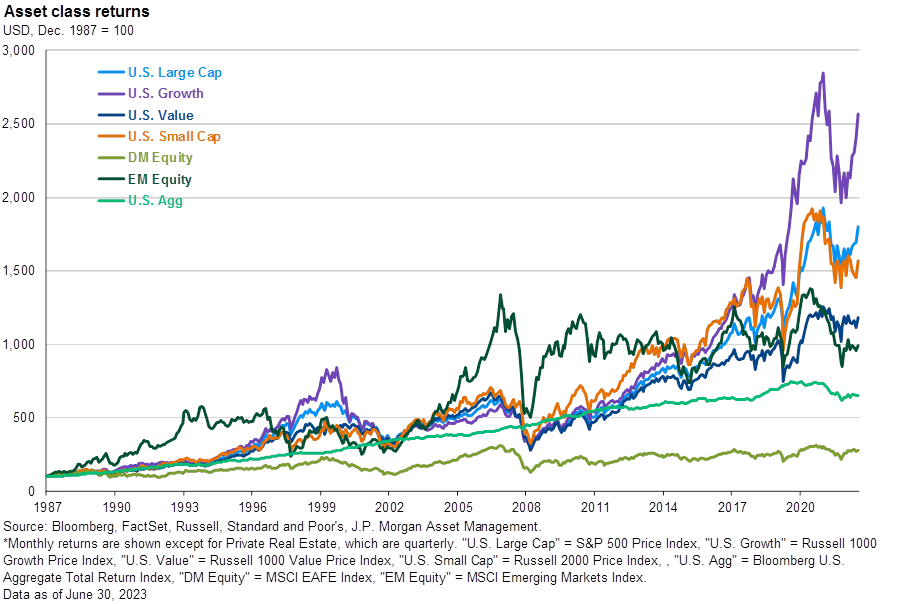

It is quite easy to focus on the things to worry about in the near-term, such as bank failures or a recession, and find reasons to not invest (or stay invested). Being uninvested can be one of the worst mistakes for an investor with a long-term horizon. As the above chart shows, the U.S. Equity market increased approximately 40 times from 1980 through mid-2023 – despite numerous serious events for the United States: six recessions, a terrorist attack, three wars, several stock market crashes, a global financial crisis, and a global pandemic.

When investing, avoiding a myopic fixation on the near-term pays off over decades; and the power of compounding returns over a long period of time should never be ignored.

Lauren Moone, CFA, contributed to this piece.