With the S&P 500 closing over 5000 for the first time on February 9th, we thought it would be constructive to revisit several of the points highlighted in our 2024 Market Outlook.

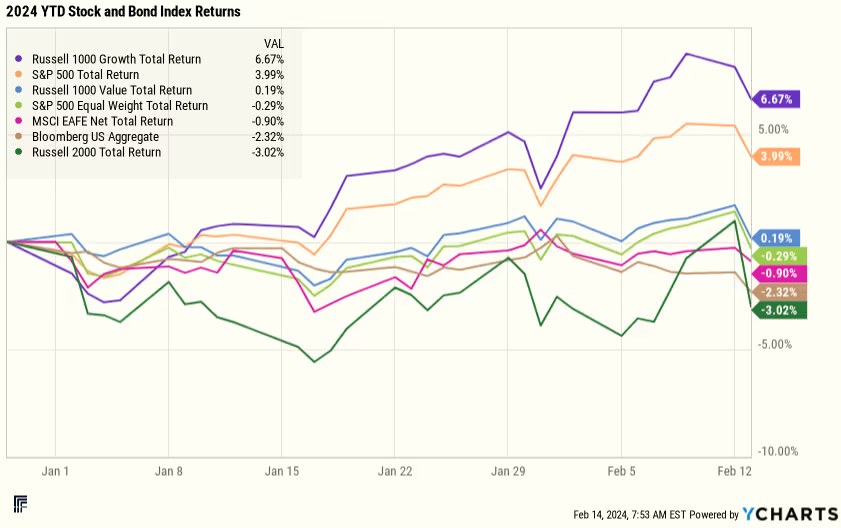

U.S. stocks have had a strong start to the year, led by large-cap growth stocks. While many forecasted a fall of the Magnificent 7 and a rise of “the S&P 493”, early 2024 has been an extension of 2023. The S&P 500 was up +3.99%, while the equal-weighted S&P 500 was down -0.29% through February 13th. Earnings have been particularly strong in the technology sector.

As we noted in our 2024 Market Outlook, stocks usually go up in election years. According to data from First Trust: since the 1928 election, 20 of 24 presidential election years have had positive returns, averaging 11.6%. The high valuations that started the year have historically led to both good and bad stock market returns. International stocks continue to remain cheap, relative to U.S. stocks. We recommend staying invested in your strategic equity allocation.

Economic data remains strong. The January employment report added a stronger than expected 353,000 jobs. Federal Reserve officials’ comments since the January 31st FOMC meeting have indicated that the Federal Reserve intends to hold rates steady past its March 20th meeting, but still indicated an intention to cut rates later in the year. The bond market had expected rate cuts as early as March.

Inflation Uptick Surprises Markets

The January CPI data, reported on February 13th, came in above consensus expectations at +0.3% month-over-month and +3.1% year-over-year. Core inflation (which excludes food and energy price changes) rose +0.4% in the month and 3.9% annually. Both the stock and bond markets sold off in response to this data. The S&P fell -1.36%, while 10-year U.S. Treasury yields rose 0.14% to 4.31%. The Federal Reserve is even more likely to keep interest rates steady at its March meeting after this report.

Bonds Post Negative Returns as Yields Rise

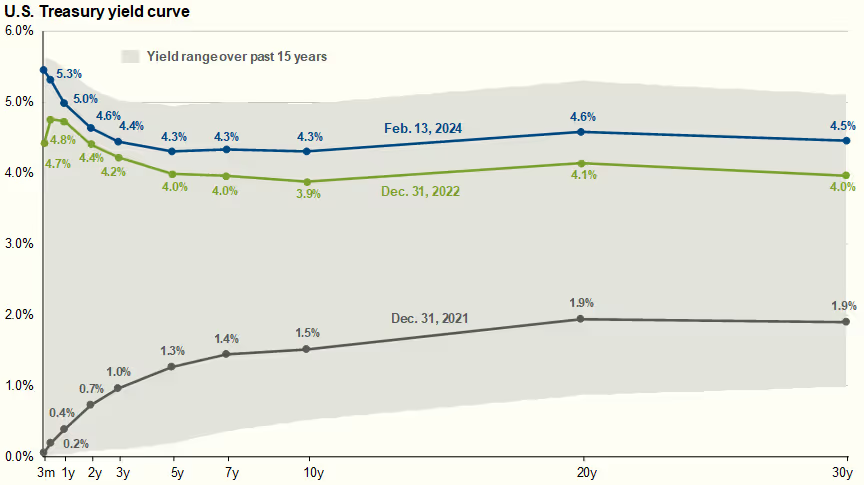

Bond yields have risen since the start of the year, particularly since the January jobs report on February 1st. As can be seen in the chart below, U.S. Treasury yields are higher than at the end of 2022, while the annual inflation rate has fallen from 6.5% in December 2022 to 3.1% in January 2024. We believe that bonds are more attractive today for investors than at the beginning of 2024, following this year’s rise in yields (e.g., over 0.4% higher on the 10-year U.S. Treasury).

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of February 13, 2024.

Regional Bank Risks Persist

Regional banks continue to present a risk to the economy and to depositors. New York Community Bank (NYCB, which also operates as Flagstar Bank) is a prime example of the risks we had flagged in our 2024 Market Outlook: that commercial real estate (CRE) losses could compound the effects of interest rate pressure on banks’ balance sheets and income statements. NYCB reported its earnings on January 31st, with an unexpected CRE write-down and a dividend cut. NYCB did not disclose that its chief risk officer had left the firm in the fourth quarter. Moody’s downgraded the bank’s long-term debt to Ba2, a non-investment grade rating on February 6th. Notably, NYCB acquired some of the assets of Signature Bank, which failed in March of last year. NYCB’s stock is down over 50% since it reported earnings.

Regional banks are more exposed to CRE loans than large banks, and we expect further write-downs by individual banks. While we do not think this represents a systemic risk to the financial system and broader markets, it can be highly risky to hold concentrated bank assets – whether owning the equity, debt, or being a depositor of a bank. If the FDIC closes a bank, equity and bond holders are likely to take significant losses. Depositors over $250,000 can also take partial losses on their uninsured deposits. There is an easy solution to safeguard your cash and improve your yield: move any cash over $250,000 from a bank and purchase U.S. Treasury securities via Money Market Funds, ETFs, or T-Bills. For more information, see our October piece that discussed this topic in depth.

Keep Your Cash Safe and Working for You

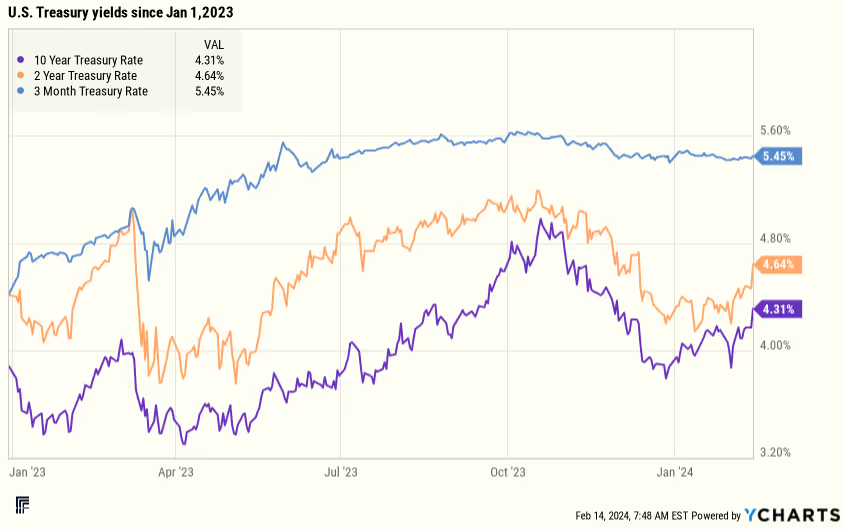

Finally, for clients who are overweight cash: do not be afraid to extend the maturity of your portfolio and invest in high-quality fixed income. As we discussed above, yields are more attractive today than at the beginning of the year. If individual banks experience significant problems this year, we could see a similar “flight-to-safety” rally in bond yields that we saw in March 2023, when Silicon Valley Bank and Signature Bank failed. The 2-year U.S. Treasury yield fell dramatically after those banks failed, as can be seen by the middle line in the chart below.

In conclusion, we believe that the risk of further bank stress is real, and that there are actions we can take for our clients to protect their cash holdings and to take advantage of the recent rise in interest rates. Please reach out to your advisor for guidance on your specific situation.

Lauren Moone, CFA, contributed to this piece.