Editor’s Note: This special edition blog post extends beyond recent market events to encompass our perspective on the core security of your cash. The location of your money is a decision that is equally as important as the person who is managing it.

Many of our clients hold significant cash balances outside of their long-term investment portfolios to fund near-term expenses, major purchases, or investments. The safety of our clients' cash is as important today as it was seven months ago, when Silicon Valley Bank (SVB) collapsed. Not all cash at financial institutions is treated equally. It is important to understand how we work to maximize both the safety and yield on our clients' cash.

I am writing to update and synthesize a few of the topics I have written on over the past several months – with the goal of helping our clients safely invest both their personal and corporate cash.

Summarizing a few key points here:

- The financial pressures that contributed to the failures of SVB and Signature Bank in March and First Republic in May are as severe today as they were earlier this year, raising the possibility of further regional bank failures.

- Bank deposits are insured up to $250,000 per depositor, per bank, per ownership category. Anything over that is at risk of loss if the FDIC closes a bank.

- SIPC covers uninvested cash at brokerage firms for the same $250,000 amount per ownership category.

- Not all cash at a financial institution is treated equally. Cash at a bank or uninvested cash at a brokerage firm is at greater risk in a bankruptcy than securities such as U.S. Treasury Bills, ETFs, and Money Market Funds that own T-Bills.

- Bank deposits are liabilities on banks’ balance sheets, backed by the banks’ assets and equity.

- Client securities on the other hand are required by law in the US to be held separately from a brokerage firm’s assets. This segregation of assets passed the test of the 2008 financial crisis.

- We recommend investing cash into securities: U.S. Treasury Money Market Funds, U.S. Treasury Bills or ETFs that own U.S. Treasury Bills. Short-term U.S. T-Bills yield as much as 5.5% today.

- Recent interest rate increases in 1-4-year Treasuries offer an attractive opportunity to extend maturities a bit and lock in yields for several years. Somewhat counterintuitively, despite short-term rates being so high, they are likely to fall in 2024 and 2025.

- If you have cash held away from our firm that you need help managing, please contact your advisor.

- Bottom line: In a financial crisis, your cash over $250,000 is safer invested in U.S. Treasuries than held at a bank. Why? Cash at a bank is backed by the bank's assets and equity. If the bank goes bankrupt, your deposit over the insured $250,000 amount could be lost. Securities held at brokerage firms (like Schwab, Fidelity, and Pershing) are held separately from the firm's assets, i.e., they are held in your name and not owned by the brokerage firm.

A Quick Recap on the Spring 2023 Banking Crisis

Between March 10 and May 1, we saw the failures of Silicon Valley Bank, Signature Bank, and First Republic Bank: the three largest bank failures since Washington Mutual's failure in 2008. I wrote a detailed piece on these events in May, including the factors that caused the downfall of these banks and the reasons there could be further stress in the banking system.

Several factors caused these banks to fail, including:

- The rapid increase in both short-term and long-term rates in 2022 was a double blow for banks: the mismatch between lending long-term at lower rates and borrowing short-term at high rates hurt both the balance sheets and income statements of banks.

- The banks that failed had high percentages of uninsured deposits, leading to rapid bank runs that forced the banks to be taken over by the FDIC.

While the FDIC ultimately guaranteed the uninsured deposits of these failed banks, assuming that they will guarantee the deposits of all future bank failures is an assumption that you should not test for balances over $250,000.

Pressure on Regional Banks Persists

As I wrote in May, regional banks were likely to be the most susceptible to further rate increases and possible weakness in the commercial real estate market, impacting the assets on their balance sheet. While all banks' loans and securities are negatively affected by increases in long-term interest rates, regional banks are much more likely to need to fund their balance sheet with deposits or borrowing from the FHLB or Federal Reserve at higher interest rates than the large money-center banks.

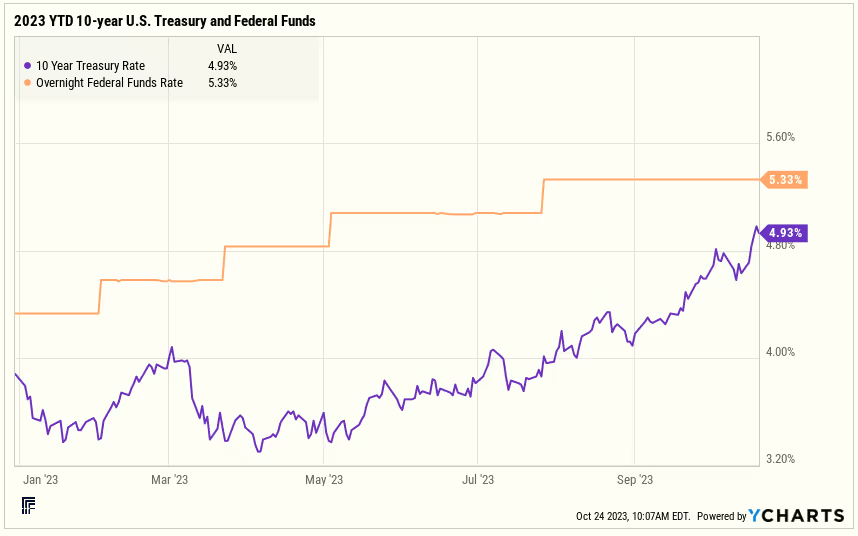

Since March, both long-term and short-term rates have increased. The 10-year US Treasury is yielding near 4.9% in late October, after touching 5% on October 23. The target Federal Funds rate has increased 0.75% since March, to a range of 5.25% - 5.50%, as can be seen in the chart below. The higher 10-year Treasury line is a good proxy for the increased pressure on the mark-to-market losses in the securities and loan portfolios of banks. The Federal Funds rate is a good proxy for the increased cost of financing in a regional bank's income statement. Even the largest banks are not immune to the impact of rising interest rates. Bank of America’s recently reported Q3 earnings included a disclosure that its unrealized securities losses had increased from $106 billion in Q2 to $131 billion.

It is important to understand that while the Federal Reserve is responsible for both monetary policy and bank supervision, monetary policy is viewed far more importantly. Federal Reserve Governor Christopher Waller spoke in Norway in June and delivered these very revealing comments:

“Let me end by noting that some have argued that the Fed's tightening of monetary policy was significantly responsible for the failures and stress in the banking system. They argue we should have taken this into account when setting policy. Let me state unequivocally: The Fed's job is to use monetary policy to achieve its dual mandate, and right now that means raising rates to fight inflation. It is the job of bank leaders to deal with interest rate risk, and nearly all bank leaders have done exactly that. I do not support altering the stance of monetary policy over worries of ineffectual management at a few banks. We will continue to pursue our monetary policy goals, which ultimately support a healthy financial system. At the same time, we will continue to use our financial stability tools to prevent the buildup of risks in the financial system and, when needed, to address strains that may emerge.”

Governor Waller said a lot in one paragraph of a speech. He confirmed that the Federal Reserve is focused on using monetary policy primarily to combat inflation, and that bank soundness is primarily the responsibility of banks themselves. However, it's hard to state that the rapid rise in interest rates in 2022 had nothing to do with the failures of banks in early 2023, as Waller implied. The Federal Reserve in mid-2021 was predicting year-end 2023 Federal Funds rates of 0.5-0.75%, 3.75% less than what occurred. Waller seems to be conveying that banks should have been smart enough to disbelieve what the Fed was saying about interest rates in 2021.

The rapid increase in long-term rates directly led to the fall in value of SVB's securities portfolio, which led to the sale of some of its securities at a loss and a failed capital raise that triggered the rapid bank run in March 2023. SVB's equity had effectively been wiped out by the effect of rising rates on its balance sheet assets. The rapid bank run on its deposits caused its failure, effectively realizing those losses. Waller's comment that the Fed will "when needed ... address strains that may emerge," while not taking any responsibility for the past impact that the Fed's policies caused on banks, suggests that there will be more bank issues to clean up after the fact.

Because of this continued pressure on the banking system, it is important to continue to manage your cash balances very closely to ensure they are safe for both your personal and corporate accounts. Even major corporations got caught in the SVB failure. For example, Roku reported in a public filing that it held over $487 million in uninsured cash at Silicon Valley Bank on March 10, 2023.

A Brief Overview of the Difference Between Bank Deposits and Securities Custody

Following the failures of Silicon Valley Bank, Signature Bank, and First Republic, people have asked why we have heard so much about banks and FDIC limits, but not about brokerage firms and the safety of their clients' assets.

The short answer is that the way in which banks hold their clients' deposits is different from the way that brokerage firms custody their clients' assets. In the United States, the securities (stocks, bonds, mutual funds) of brokerage firms' clients are required by law to be kept separately from a firm's assets. This separation of assets has served clients very well in past crises to keep their assets safe. A bank deposit, on the other hand, is a liability on the balance sheet of the bank that a client is doing business with.

In a bankruptcy, brokerage firm client assets are segregated from the firm's assets and are not available to creditors' claims. This segregation of assets contrasts with a bank failure, in which deposits at a bank are senior creditors of that bank's failure, and uninsured deposits could be at risk of receiving a haircut when that bank failure is resolved. In 2008, the brokerage firm system had a worst-case, real-world test when Lehman Brothers went bankrupt. Fortunately, brokerage clients with fully paid-for securities were able to transfer their accounts to other firms very quickly, following that bankruptcy.

Many large U.S. brokerage firms are either owned by a large bank or own an affiliated bank. That bank is often the default cash sweep option for the brokerage firm's client cash. It's in these cases where it's important to understand precisely what a client's cash is: is it swept into a bank deposit of the affiliated bank (and subject to FDIC protection rules on bank cash), or is it held as cash at the brokerage firm (and subject to the SIPC protection rules on cash)?

Brokers at wirehouse brokerage firms are often paid more to keep their clients' cash in their firm's affiliated bank deposit (thereby funding the brokerage firm's bank). In contrast, as fiduciaries for our clients, our firm is paid solely by our clients; our goal is to maximize the safety and yield of our clients' cash.

We have very high confidence in the safety of clients' securities at brokerage firms, as a result of the SEC Customer Protection Rule. However, there's no reason to keep over $250,000 in cash in a brokerage account, unless you need it for an immediate purchase. Fortunately, regardless of how the cash is held in a client's brokerage account, the protection limits are similar; and the solution to enhance the safety of, and almost certainly the yield on, client cash is similar, as detailed below.

Protecting Our Clients’ Cash

The banking crisis this year was a serious situation and an echo (not necessarily a repeat) of the 2008 financial crisis. I have used the analogy of a major financial earthquake hitting the San Francisco Bay Area in March. We saw another major aftershock in May (First Republic), but do not know how many or how severe future ones may be. With the pressure building on banks from recent interest rate increases, we believe that it is prudent to prepare, in advance, for any potential banking problems.

It is important to separate your long-term holdings from your near-term cash needs. And it is always better to keep slightly more cash than you might think – so that you can live your life, handle an unexpected expense, or make an attractive investment, if it should arise.

We have a playbook for managing clients’ cash – which I learned as an advisor at Goldman Sachs during the 2008 financial crisis – to keep your cash as safe as possible.

Here are a few basic steps to understand and take:

- Bank deposits are insured up to $250,000 per depositor, per bank, per ownership category. Anything over that is at risk of loss if the FDIC closes a bank.

- SIPC covers uninvested cash at brokerage firms for the same $250,000 amount per ownership category.

- Invest your excess cash into securities: U.S. Treasury Money Market Funds, U.S. Treasury Bills, or ETFs that own U.S. Treasury Bills.

- U.S. Treasury securities have the double benefit of being both the safest financial instrument and their interest is exempt from state taxes. Don’t stretch for small amounts of yield in other types of MMFs in your cash portfolio.

- In 2008, yields on U.S. T-bills went negative during the post-Lehman Brothers panic. Today they yield approximately 5.5%. Most banks are paying considerably less than the Treasury is right now.

In the current environment, being safe with your excess cash generally improves your return, as opposed to keeping it in a bank account!

Locking in Safe Yields for Longer

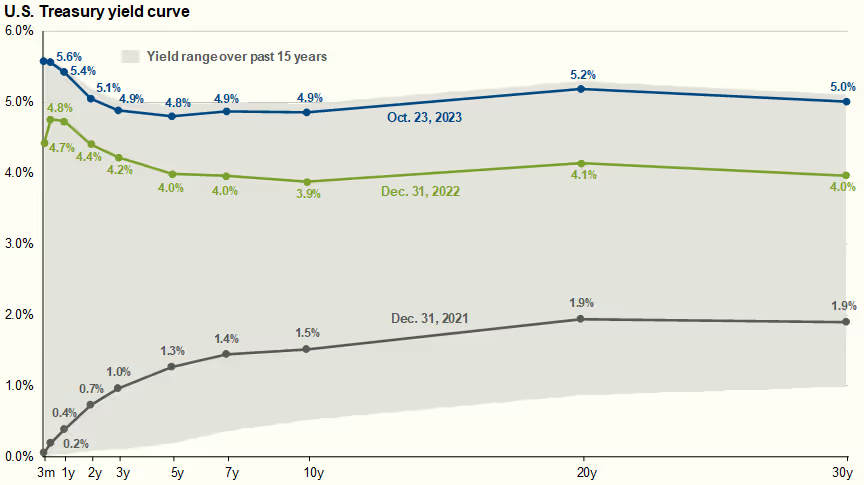

As I wrote about in our recent market commentary, U.S. Treasury yields are at or near their highest levels of the decade across the entire yield curve, as can be seen in the chart below.

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of October 6, 2023

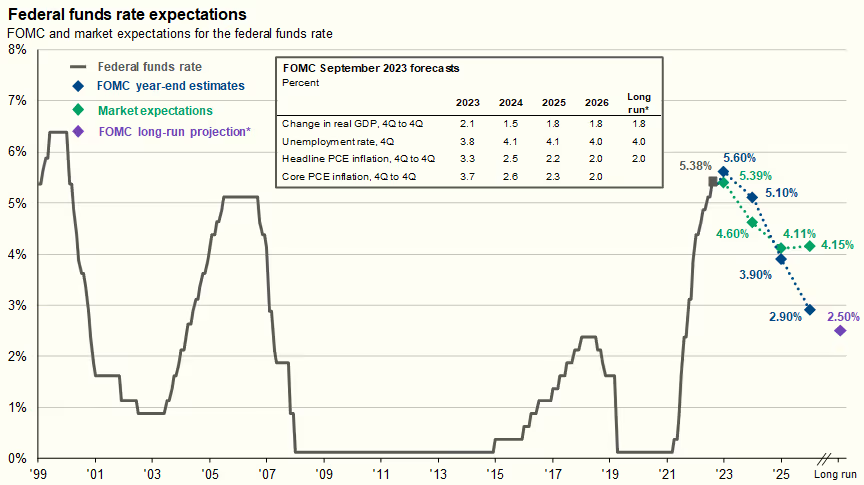

While short-term T-Bills are the highest yielding securities on the yield curve at present, both the Federal Reserve and the fixed income markets expect short-term rates to fall in 2024 and 2025. The Federal Reserve’s talk of “higher for longer” interest rates does not mean “higher forever.”

Source: Bloomberg, FactSet, Federal Reserve, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of October 6, 2023. Market expectations are based off of USD Overnight Index Swaps. *Long-run projections are the rates of growth, unemployment and inflation to which a policymaker expects the economy to converge over the next five to six years in absence of further shocks and under appropriate monetary policy. Forecasts are not a reliable indicator of future performance. Forecasts, projections and other forward-looking statements are based upon current beliefs and expectations. They are for illustrative purposes only and serve as an indication of what may occur. Given the inherent uncertainties and risks associated with forecasts, projections or other forward-looking statements, actual events, results or performance may differ materially from those reflected or contemplated.

For clients whose cash balances are larger than their near-term needs, we recommend investing the excess into short-term U.S. Treasuries to lock in yields, rather than risk reinvesting at lower rates. Even extending maturities from 3 months to 1 or 2 years offers clients safe yields over 5%, if held to maturity.

If you have questions about what to do with cash you hold away for your personal or corporate account, we encourage you to connect with your Farther advisor to discuss your options.

Lauren Moone, CFA, contributed to this piece.