The stock market experienced robust Q1 returns, fueled by optimism for a soft landing in the U.S. economy – marked by falling inflation, continued GDP growth, and Federal Reserve rate cuts. This rosy narrative changed in April, however, with major stock and bond markets selling off – resulting in a 5.6% decline in the stock market. This correction then proved to be short-lived, with markets rebounding and reaching new highs in May.

Year-to-Date performance highlights:

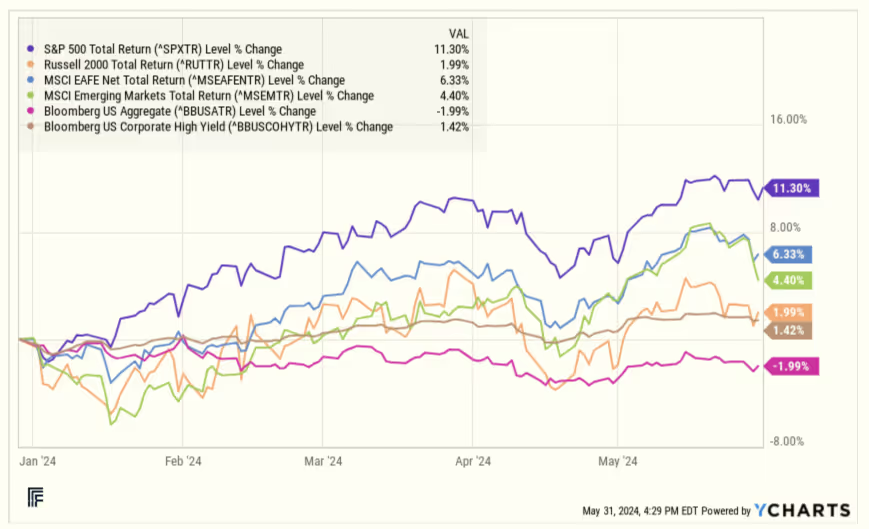

- The large-cap S&P 500 index rose by 11.3% through May, significantly outperforming the small-cap Russell 2000, which increased by 1.99%.

- Growth stocks continued to outperform value stocks, with the Russell 1000 Growth index up 12.84% while the Russell 1000 Value index was up 6.09% through May.

- International stocks were up 6.33% YTD, underperforming their U.S. counterparts.

- The Bloomberg Aggregate bond index was down -1.99% through May, driven by rising interest rates.

What has changed in the last few months?

Inflation: The year began with most economic analysts expecting that inflation would fall below 3%, toward the Federal Reserve’s 2% target. Contrary to expectations, the March CPI inflation report showed a third consecutive month of higher-than-anticipated inflation, with CPI rising to 3.5% year-over-year. Subsequently, the April CPI inflation report released in mid-May came in softer than expected, with CPI ticking down to 3.4% year-over-year.

Economic Growth: First Quarter GDP growth was an annualized +1.6%, well below the consensus expectations of 2.4%. The core PCE inflation index grew at 3.4% annualized, aligning with the latest CPI index, confirming fears of inflation exceeding the Federal Reserve’s 2% goal. This combination of slower growth and higher inflation spurred fears of stagflation returning – a scenario of stagnant growth and high inflation – rather than a soft landing.

The Federal Reserve: At the start of the year, the Federal Reserve expected three rate cuts for 2024, while markets anticipated up to six. However, persistently high inflation has tempered these expectations to one or two cuts.

At the May 1 Federal Open Market Committee (FOMC) meeting, the Federal Reserve maintained short-term rates, but reduced its monthly Treasury bond sales from $60 billion to $25 billion, effectively easing longer-term interest rates. In Chairman Jerome Powell’s post-meeting press conference, he stated that “it’s likely to take longer for us to gain confidence that we are on a sustainable path to 2% inflation” and allayed concerns that the Fed was considering rate hikes. When asked about stagflation he said: “I don’t see the stag or the ‘flation.” Still, despite Powell’s confidence and economic influence, he is not omniscient – and has made mistakes in forecasting the future before, e.g. his predictions of “transitory inflation” in 2021.

Interest Rates: In response to higher inflation and a belief that short-term rates would remain higher for longer, Treasury yields have risen across the yield curve since the start of the year. The 2-year Treasury yield rose 0.7% to over 4.9%, and the 10-year Treasury yield rose 0.6% to over 4.5%.

Earnings: First quarter corporate earnings were strong, with 98% of S&P 500 companies reporting and 78% surpassing analyst estimates, compared to a long-term average of 66%. According to JPMorgan Asset Management, S&P 500 earnings are projected to grow by 10% this year and 14% next year, following flat earnings in 2023.

Banking Stress: Regional banks continue to grapple with high interest rates, which reduce the value of their assets and increase funding costs. Commercial real estate loans have become problematic, as more borrowers have defaulted on their loans. New York Community Bank, which was in a precarious financial situation in February, received a $1 billion capital infusion in March. Republic First Bank, a $6 billion bank not to be confused with First Republic Bank, failed on April 26th. Expect more problems in the regional banking sector and keep your cash safe in Treasuries.

What does this all mean?

Consensus economic forecasts are much more of a weathervane than a crystal ball. It is natural human behavior to rely on recency bias in our thinking and predictions – valuing our recent experiences more than historical ones.

Think of how many times the consensus has changed quickly in the last 18 months. The economic consensus called for a recession in 2023 (GDP growth had nearly flatlined the first half of 2022). After growth picked up in 2023 and inflation fell from its peak of 9.2% towards 3%, the consensus shifted to a soft-landing for the economy. After three inflation reports higher than expected and one quarter of weaker than expected GDP growth, talk of few or no interest rate cuts and fears of stagflation returned to the discussion. Following the downtick in inflation reported in May, markets returned to rally back to new highs. How these changing views will play out is impossible to know, but predicting future economic trends based solely on recent events is unreliable.

How are the financial markets valued today?

Predicting future returns is notoriously difficult, as we have written. The frustrating fact is that current valuation (whether an asset is cheap or expensive) is a poor indicator of returns over a 1-year period. In the U.S. equity market, 1-year returns have been as good or bad when the stock market trades at 20x earnings as when the stock market trades at 14x earnings according to research by JPMorgan Asset Management. However over 5-year periods, higher returns tend to be driven by how cheap the market is at the start of the period.

With the understanding that our thoughts aren’t predictive of near-term returns, we thought it would be useful to summarize a few valuation indicators.

- The U.S. stock market, trading at 21x earnings as of May 31, is above its long-term average of 16.7. If earnings grow by 10% this year as expected, the P/E ratio would fall to ~19x, even if the market remains flat. This suggests returns of 5-7% over the next 5 years.

- International stocks remain cheaper than U.S. stock, with P/E ratios of 15.5x, 33% lower than U.S. stocks. Despite positive returns over the past 16 months, international stocks have lagged behind U.S. stocks, widening the valuation gap.

- Treasury yields as of May 31 are more attractive than at the beginning of the year, as seen below. In contrast to buying stocks, if you hold Treasuries to maturity, you know your return in advance.

- Given the CBO’s outlook for budget deficits starting at $1.5 trillion annually and rising for the next 10 years, it’s likely that interest rates will remain higher than they were during the 15 years of near zero rates, prior to rates rising in 2022.

- High yield corporate bonds remain at tighter than average spreads over Treasuries, +3.3% versus a long-term average spread of 5.6%. These spreads can be justified if the economy remains strong but could widen considerably if the economy weakens.

- Middle market private credit strategies appear attractively priced. These funds make senior loans to private companies and are currently yielding approximately 10%. Manager selection in this area is particularly important; not all funds are created equally in this space. Investors should seek managers who invest in non-cyclical businesses with low leverage that can service their debt even at today’s high rates. For investors who can tolerate the illiquidity, a small allocation to this sector is warranted.

What if you’re worried about stagflation?

According to Google Trends, recent searches for stagflation have spiked to their highest level since June 2022. At that time, the economy was slightly contracting due to the Omicron wave, supply chain disruptions, rising interest rates, and peak inflation of 9.0%. It's important to note that Q1 2024 saw GDP growth of 1.6%, and April’s inflation report came in at 3.4% annually – both better than mid-2022. It is challenging to predict whether stagflation will occur or whether it will be something that the market has forgotten a few months from now.

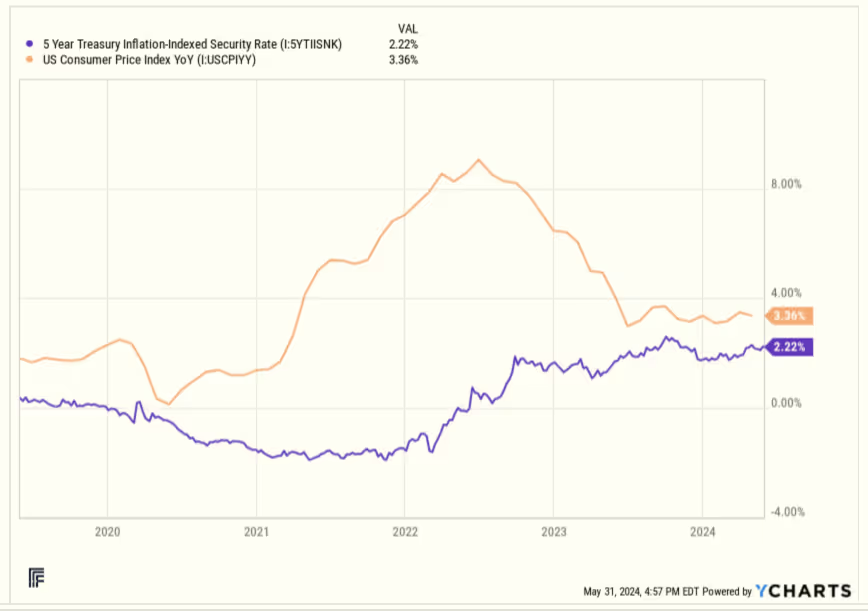

However, certain securities are more attractively priced today to benefit from higher inflation. Treasury Inflation-Protected Securities (TIPS) now offer positive real returns. As of May 30, 5-year TIPS yield 2.22% over CPI, ensuring a positive real return for investors. For taxable investors, both the CPI appreciation and the coupon are taxed annually, making TIPS particularly advantageous in tax-deferred or tax-free accounts.

Near-Term Portfolio Positioning Thoughts

Try not to miss the forest for the trees and get overly focused on current worries about the economy, inflation, or politics.

- We recommend staying at your strategic weight in stocks. Consider adding international stocks, especially if you don’t own any.

- We like high-quality short term (2-5 year) fixed income, funded from cash.

- If you are concerned about stagflation or want to lock in a real return over inflation, consider adding 5-year TIPS securities into your fixed income portfolio.

- Maximize the security and yield of your cash by investing in Treasuries, either via money market funds, ETFs or purchasing T-Bills directly.

Long-Term Portfolio Positioning Thoughts

With Treasury bonds nearing 5% and stocks trading at 21x earnings (a 5% earnings yield), diversified portfolios seem well positioned to return 5% or more annually over the next 5 years. Since stocks are expected to grow their earnings, a return of 5-7% on stocks seems quite reasonable in the next 5 years, although this growth will almost certainly not occur in a straight line. Investors willing to consider alternative investments such as private credit or private equity may achieve higher returns, though these asset classes come with increased risks associated with illiquid investments.

We encourage you to call or write, if you have any questions about the topics raised in this piece.

Lauren Moone, CFA, contributed to this piece.